/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Dell (DELL) has emerged as one of the top-performing stocks in the S&P 500 ($SPX) in 2026, with shares surging more than 225% year-to-date (YTD). The rally in DELL stock reflects booming demand for the company’s artificial intelligence (AI) servers as enterprises and hyperscalers accelerate investments in AI infrastructure.

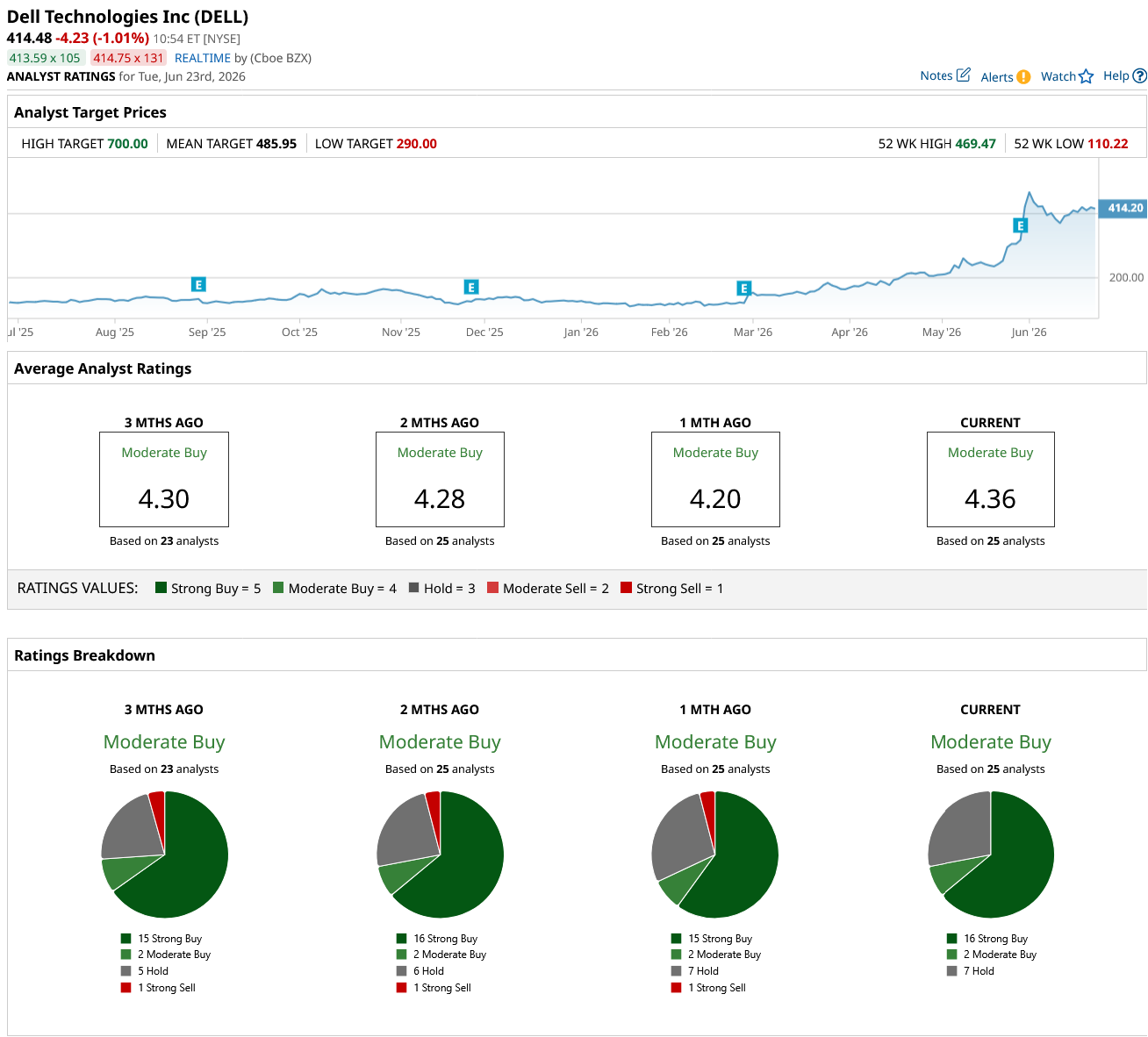

Despite the stock's remarkable run, at least one analyst believes DELL could hit $700 per share, the Street’s highest price target, implying about 69% upside from current levels.

At first glance, that price target may seem overly optimistic. However, when viewed against the backdrop of soaring AI infrastructure spending, strong server demand, and its growing position in the AI ecosystem, DELL stock hitting $700 becomes much easier to justify.

Dell Is Firing on All Cylinders

Dell is witnessing strong demand across all lines of business and geographies. The company recently delivered one of its strongest quarters in history, underscoring that demand for AI infrastructure remains exceptionally robust.

First-quarter revenue surged to $43.8 billion, while profitability expanded even faster. Gross margin dollars increased 57% to $7.8 billion, operating income jumped 154% to $4.2 billion, and net income nearly tripled to $3.2 billion.

Dell’s adjusted EPS came in at $4.86, crushing both management's guidance of $2.90 and Wall Street's consensus estimate of $2.79.

Supporting Dell’s growth is the solid momentum in its Infrastructure Solutions Group (ISG). ISG revenue climbed 181% year-over-year (YoY) to $29 billion. AI-related demand remained exceptionally strong, generating $24.4 billion in orders and $16.1 billion in AI server revenue during the quarter.

Perhaps more important than the quarter’s revenue growth is the visibility provided by Dell’s AI backlog, which expanded to a record $51.3 billion. Dell’s leadership said demand continues to outpace supply. The company also noted that its AI opportunity pipeline continues to grow and remains several times larger than the current backlog, suggesting sustained solid growth potential.

Demand is broad-based rather than concentrated in a single customer group. Hyperscalers, cloud providers, sovereign entities, and enterprise customers are all investing heavily in AI infrastructure, positioning Dell to gain share as organizations build next-generation computing capabilities.

Beyond AI, Dell’s traditional server business is also performing well. Revenue from conventional servers increased 92% YoY, supported by enterprise infrastructure refresh cycles and rising compute requirements. Management highlighted that a large portion of the installed base still relies on older-generation systems, creating a sizable long-term upgrade opportunity.

Additionally, AI inference workloads are driving incremental demand for traditional compute infrastructure, providing another growth catalyst.

Management’s outlook reflects confidence that current momentum will continue. For the second quarter, Dell expects revenue of $44 billion to $45 billion and adjusted EPS of approximately $4.80, with ISG projected to grow about 75%. The company also sharply increased its full-year forecast, now expecting fiscal 2027 revenue of $165 billion to $169 billion, compared with its previous outlook of $138 billion to $142 billion.

AI server revenue is projected to reach roughly $60 billion, while operating income is expected to rise more than 55%, and adjusted EPS is forecasted to jump about 74% to $17.90. The upgraded guidance suggests Dell is firing on all cylinders and is poised to expand earnings at a solid pace, which will support its share price rally.

Could DELL Stock Hit $700?

At first glance, a $700 price target for DELL stock may seem far-fetched, but there is a credible case for it. Demand for the company's AI servers continues to outpace supply, and Dell is benefiting from a record backlog, strong order growth, and a significantly improved financial outlook from management. These factors position the company to deliver robust earnings growth, which could provide further support for its stock price.

As enterprises, cloud providers, and governments continue to invest heavily in AI, Dell is well-positioned to capture a meaningful share of that spending. Given its rapid earnings growth, expanding AI business, and still-reasonable valuation relative to its earnings growth prospects, a $700 share price looks less like an ambitious forecast and more like a realistic possibility if current trends persist.

Wall Street analysts remain cautiously optimistic on DELL, with the stock currently carrying a "Moderate Buy" consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)