IREN Limited (IREN) has come a long way from its Bitcoin (BTCUSD) mining roots. Over the past few years, the company has made a big shift, turning itself into a full-fledged AI infrastructure player. With a massive long-term powered land bank of around 6 gigawatts and a business that stretches from data centers to GPU cloud services, IREN has carved out a sweet spot in the booming AI market. As demand for AI computing keeps exploding, the company is looking more like an AI cloud provider.

That is starting to catch Wall Street’s eye. Jefferies recently initiated coverage on the Australian company with a “Buy” rating and a $79 price target, with analyst Jonathan Petersen and his team believing IREN’s major partnerships with giants like Microsoft (MSFT) and Nvidia (NVDA) have put it in a strong position to generate billions in recurring revenue and compete with some prominent AI infrastructure names.

So, why is Jefferies turning bullish on IREN now? Let’s dive into the details.

About IREN Stock

IREN has grown into a leading AI infrastructure company, providing the computing power that fuels today’s AI boom. The company, with a market capitalization of $21.4 billion, operates a vertically integrated platform, owning both the hardware and the data centers that support AI training and inference workloads.

Backed by a vast portfolio of grid-connected land and power assets in renewable-rich regions across North America, Europe, and Asia-Pacific, IREN offers everything from GPU cloud services to custom AI-ready facilities. As demand for computing capacity continues to outstrip supply, IREN has positioned itself as a key player in the high-performance computing market, helping customers accelerate their AI ambitions with flexible infrastructure and large-scale GPU clusters.

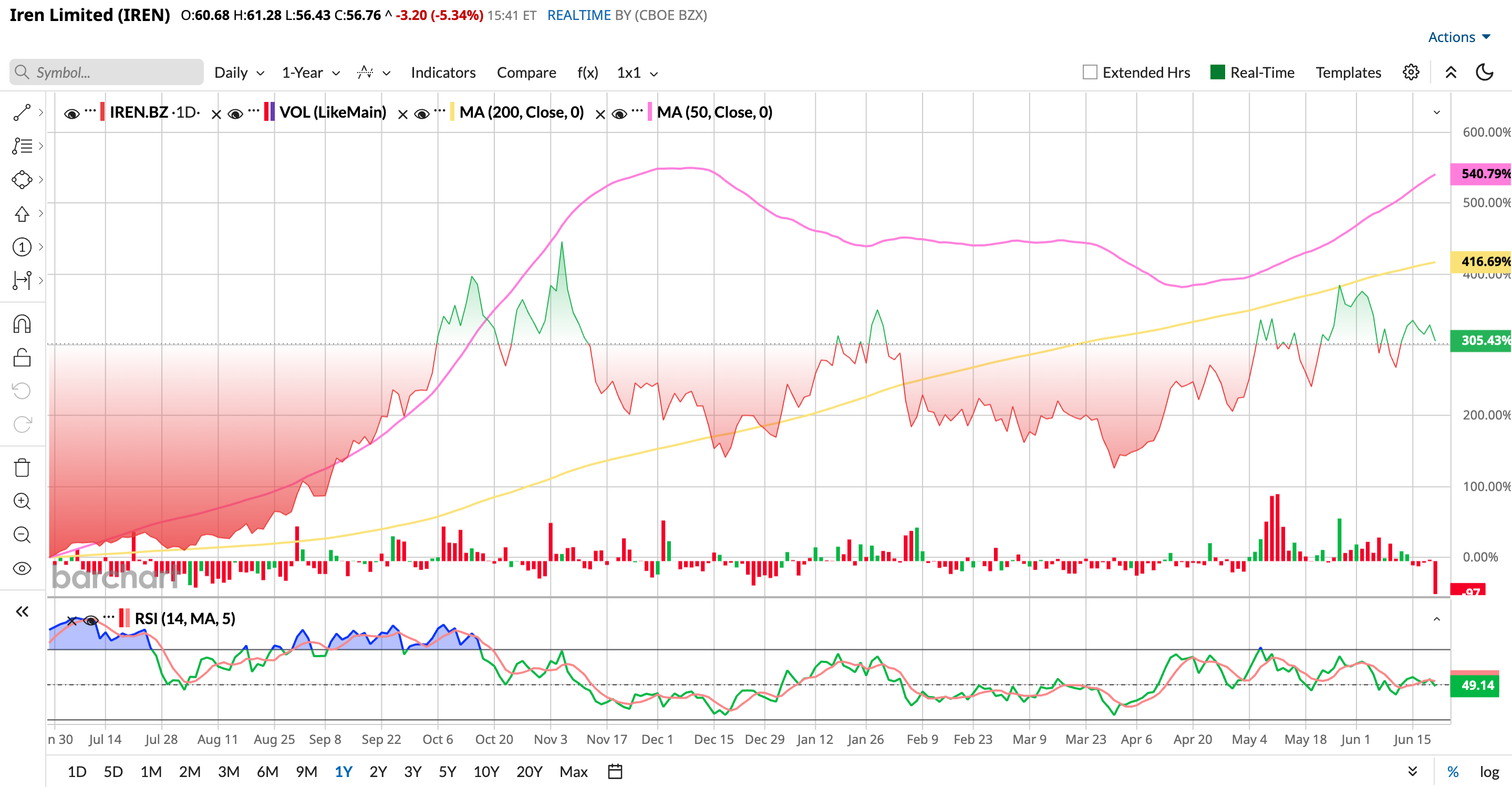

IREN stock has had its ups and downs. Sure, shares are still 26% below their 52-week high of $76.87 reached last November, but zoom out, and the picture looks pretty impressive. Over the past 52 weeks, the stock has soared 445%, leaving the broader market’s gains behind. The rally really hit another gear when shares crossed the $70 level on June 3, but since then, the stock has taken a step back and is now 19.4% below that level.

Even so, IREN is still sitting on gains of 51% in 2026. The latest boost came after Jefferies jumped into the ring with an upbeat rating, giving bulls another tailwind.

Currently, IREN seems to be at a crossroads. According to the trader’s cheat sheet, support sits around $58.95 and $58.53, while resistance stands near $60.97 and $61.39. In other words, the stock looks like it is catching its breath after a strong sprint. If shares can push above $61, bulls could get back in the driver’s seat. A break below support may invite some profit-taking.

Technically, things still look steady. The 14-day RSI is 49.51, which means the stock is not running too hot or too cold. Plus, shares remain above both their 50-day and 200-day moving averages. So, while IREN may be taking a breather, it does not look like the AI story has run out of gas just yet.

A Snapshot of IREN’s Q3 Numbers

IREN reported its fiscal third-quarter 2026 results on May 7, generating total revenue of $144.8 million, down 21.6% sequentially and below Wall Street’s expectations. Net loss widened to $247.8 million from $155.4 million in the prior quarter, while adjusted EBITDA slipped to $59.5 million from $75.3 million in Q2 fiscal 2026. Still, the adjusted EBITDA margin held steady at 41%.

The changing mix of the business tells the bigger story. As IREN shifts its focus almost entirely toward AI, Bitcoin revenue fell 33.6% sequentially to $111.2 million. Management said the decline was largely due to lower Bitcoin prices and the ongoing retirement of mining hardware to make room for GPU deployments. Meanwhile, AI Cloud Services revenue nearly doubled from the previous quarter, jumping 94.2% to $33.6 million, showing where the puck is headed.

The company also has plenty of liquidity. IREN ended Q3 with $2.6 billion in cash and equivalents and expects operating cash flows, GPU financing, and other funding initiatives to support near-term capital spending. In fact, roughly 95% of Microsoft-related GPU capex is expected to be covered through prepayments and financing.

On the strategic front, IREN landed a five-year, $3.4 billion AI Cloud contract with Nvidia for air-cooled Blackwell GPUs, with deployment planned within 60 megawatts of existing capacity at Childress and ramp-up expected in early 2027. The two companies also formed a broader 5-gigawatt partnership to develop Nvidia-aligned infrastructure across IREN’s global data center pipeline. As part of the deal, Nvidia received rights to purchase up to 30 million shares at $70 each, representing potential investment capacity of as much as $2.1 billion.

Meanwhile, IREN said its 2026 build program remains on track for 480 megawatts of AI Cloud capacity by year-end, with even bigger expansion plans targeting 1,210 megawatts in 2027.

IREN recently expanded its footprint with the acquisition of Spain-based Ingenostrum, or Nostrum Group, a developer of grid-connected AI data centers. The deal gives IREN a foothold in Europe, one of the fastest-growing markets for AI infrastructure. More importantly, it adds roughly 490 megawatts of secured power in Spain, along with a broader development pipeline.

Nostrum brings a team of more than 50 specialists spanning engineering, development, construction, and operations. With Spain offering abundant renewable energy and strong fiber connectivity, the acquisition gives IREN both the local talent and the infrastructure needed to hit the ground running as demand for AI cloud services continues to heat up across Europe.

Wall Street thinks IREN still has plenty left in the tank. Analysts expect fiscal 2026 revenue to reach about $742.8 million, even as the company posts a loss of roughly $1.25 per share. But the tide could turn quickly. Losses are expected to shrink sharply by 188% YOY, and by next fiscal year, IREN could finally turn the corner, with earnings projected at around $1.10 per share.

What's Wall Street Saying About IREN Stock?

Jefferies is making a pretty strong bet on IREN. The brokerage firm recently initiated coverage on the Australian AI infrastructure company with a “Buy” rating and a $79 price target. That represents an upside potential of 31.8% from current levels.

Analyst Jonathan Petersen and his team believe IREN has carved out a unique spot in the AI infrastructure game. The company controls an enormous powered land bank of roughly 6 gigawatts and runs a vertically integrated GPU cloud business. Thanks to major contracts with Microsoft and Nvidia, Jefferies estimates IREN could generate about $3.1 billion in annual recurring revenue.

The crown jewel is a five-year, $9.7 billion deal with Microsoft for 200 megawatts of Nvidia GB300 capacity at Childress, followed by a separate $3.4 billion AI cloud contract with Nvidia. Put together, Jefferies says these deals give IREN a seat at the big table alongside players like CoreWeave (CRWV) and Nebius (NBIS).

The Microsoft agreement also includes a $1.9 billion upfront payment and $3.65 billion in GPU financing at roughly 6%, a setup Jefferies says could help IREN earn back its $8.8 billion investment while generating returns north of 20%.

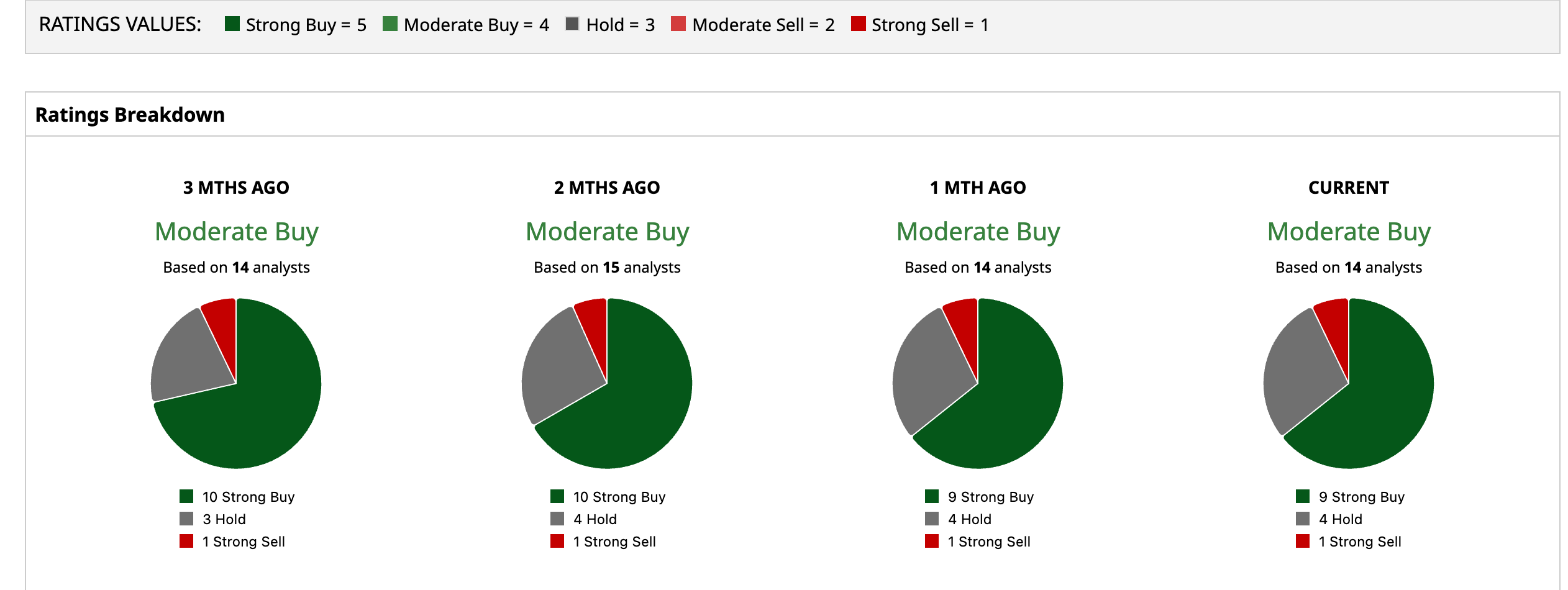

Wall Street analysts overall are upbeat on IREN. The stock has a consensus “Moderate Buy” rating. Among the 14 analysts covering the stock, nine suggest a “Strong Buy,” four recommend a “Hold,” and one has a “Strong Sell” rating.

The average price target of $80.33 implies potential gains of 42.13% from current levels, while the Street-high target of $105 suggests shares could soar as much as 85.8% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)