/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Micron Technology (MU) will report fiscal third-quarter 2026 earnings on June 24. Surging revenue for high-bandwidth memory (HBM), DRAM, and NAND, coupled with increased pricing, has led Micron to deliver massive earnings growth over the past several quarters. This, in turn, has driven a significant rally in MU stock.

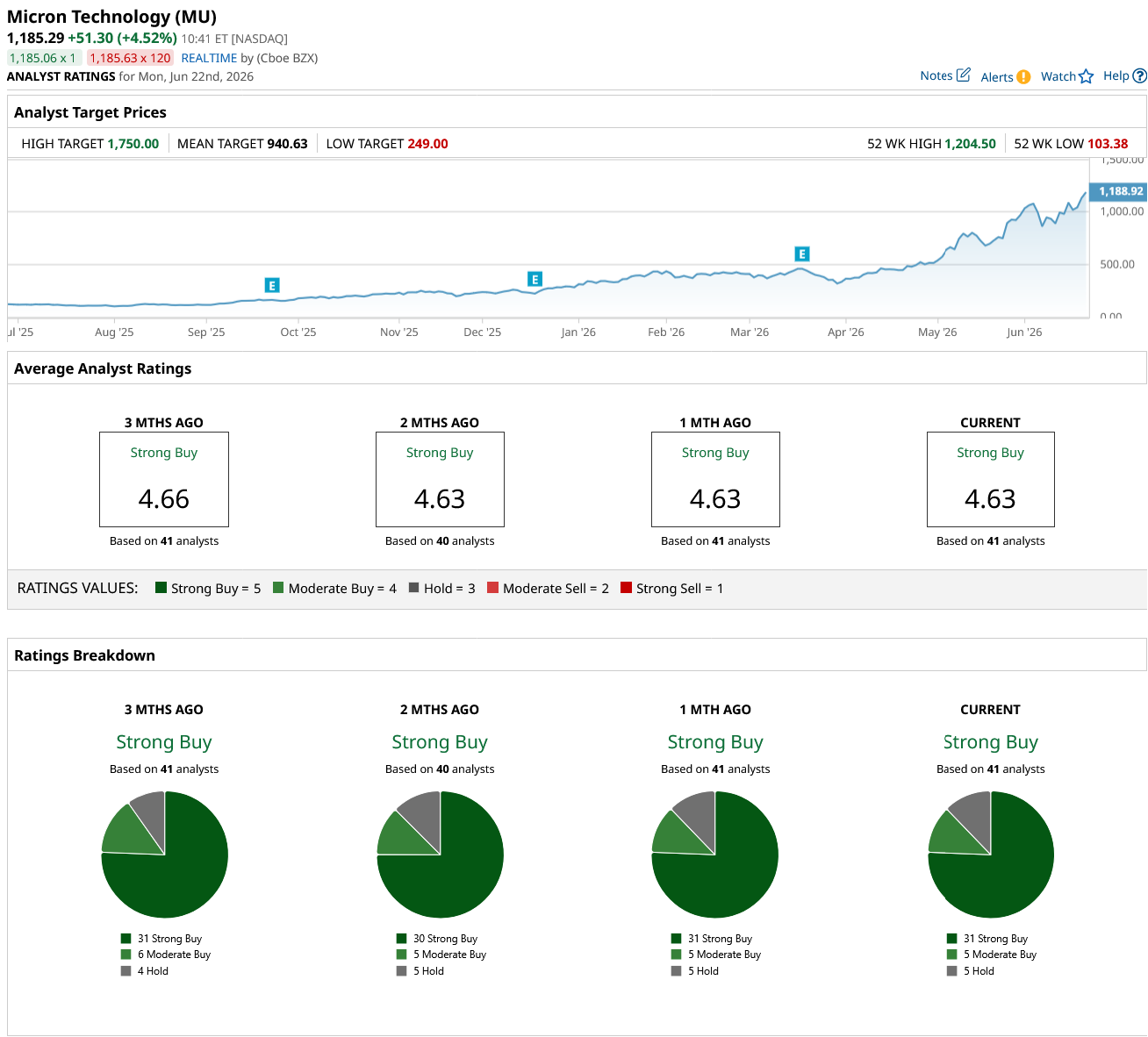

Micron has delivered eye-popping returns, with its shares climbing 858% over the past year and 315% year-to-date (YTD).

With increasing demand and a strong pricing environment, Micron is likely to deliver another blowout quarter.

Micron's Q3 Earnings: Here’s What to Expect

For Micron, the tailwinds behind the AI memory boom remain intact, setting the stage for another potentially strong quarter. As hyperscalers and enterprises continue investing aggressively in AI infrastructure, demand for high-performance memory is accelerating, supporting Micron’s growth.

The demand backdrop is being amplified by tight industry supply. Memory production remains constrained across the sector, allowing pricing to stay elevated and supporting substantial margin expansion for Micron.

DRAM remains Micron's largest growth engine. In fiscal Q2, DRAM revenue reached $18.8 billion, up 207% year-over-year (YoY) and accounting for 79% of total company revenue. Sequentially, DRAM revenue rose 74%, supported by mid-single-digit growth in bit shipments and mid-60% pricing increases.

AI workloads are emerging as the primary catalyst. Training and inference applications require significantly more memory than traditional computing workloads, while next-generation AI servers continue to push memory requirements higher. At the same time, conventional server demand remains healthy as enterprises refresh aging infrastructure and deploy systems capable of supporting AI-driven workloads.

Micron's NAND business is also benefiting from solid AI adoption. Fiscal Q2 NAND revenue climbed to a record $5.0 billion, up 169% YoY.

The company is seeing increasing demand from data center customers deploying AI applications that rely heavily on storage-intensive technologies. At the same time, solid-state drives (SSDs) continue to gain share in capacity storage deployments.

Micron's competitive position appears to be strengthening. The company increased its market share in the data center SSD market. Management noted that NAND demand is now running well ahead of available supply and expects further growth in the quarter ahead.

Overall, Micron’s management expects third-quarter revenue of $33.5 billion, implying sequential growth of about 40% and YoY growth of about 260% from $9.3 billion.

Micron’s profitability is expected to expand significantly. Management forecasts gross margins of roughly 81%, up sharply from 39% a year ago and above the already impressive 75% reported in the second quarter. This expansion is being driven by stronger memory pricing, improved manufacturing efficiency, and a more favorable product mix.

Earnings growth is expected to outpace revenue growth. Micron projects earnings of approximately $19.15 per share, compared with $1.91 per share in the year-ago quarter. The substantial increase reflects both higher pricing and stronger shipment volumes in a supply-constrained market.

Wall Street is even more optimistic, with analysts forecasting earnings of $20.81 per share. Micron has consistently exceeded consensus expectations in recent quarters, benefiting from stronger-than-anticipated pricing trends and resilient AI-driven demand. If those conditions persist, the company may once again deliver results above market expectations.

Bottom Line on MU Stock

Micron’s fiscal third-quarter results are once again expected to highlight the strong tailwinds driving the memory market, including surging AI-related demand, constrained supply, and a favorable pricing environment. These factors should support another quarter of strong revenue and earnings growth.

Despite its impressive rally over the past year, Micron's valuation remains relatively attractive. MU trades at 19 times forward earnings, a reasonable multiple considering analysts expect MU’s earnings to soar more than 701% in fiscal 2026, followed by an additional 91.3% increase in fiscal 2027.

However, with expectations already elevated, Micron’s outlook for memory pricing, AI demand, and future profitability will have a greater impact on the stock’s next move than the quarter's reported results alone.

Wall Street remains optimistic on Micron, with analysts maintaining a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)