/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)

Accenture Plc (ACN) stock is down 5% today after falling 18% last Thursday, spurring huge, unusual put and call activity today. Management guided for lower revenue in its June 18 fiscal Q3 earnings release. However, it guided for higher earnings per share for the FY 2026 ending August 31, according to Benzinga.

ACN is at $121.22, down from a $196.59 peak on June 1 (-38.3%) and off 22% from June 17 ($156.01) right before its earnings release.

Investors seem to think the market's reaction to its revenue guidance. The unusually high volume of out-of-the-money (OTM) puts and calls today seems to imply this.

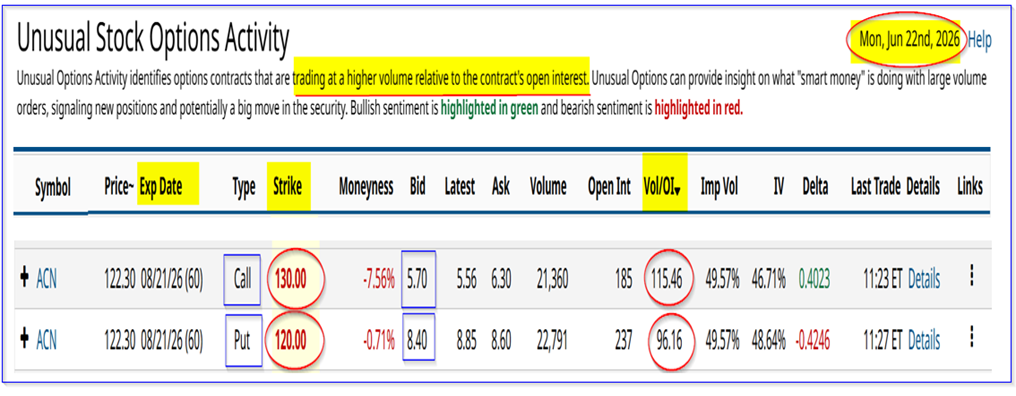

This high options volume can be seen in today's Barchart Unusual Stock Options Activity Report.

It shows that the call option volume at the $130.00 strike price expiring in 60 days (Aug. 21, 2026) is over 115 times the prior number of call options outstanding. That strike price is over 7.2% higher than today's price, so it is considered “out-of-the-money.”

Moreover, $120.00 strike price put options for the same Aug. 21, 2026, expiry date (also “out-of-the-money” since it is 1.0% below today's price) have over 96 times the prior outstanding contracts.

It's likely, therefore, that some investors are either shorting the puts to fund call options buying, or vice versa, or possibly shorting both. Let's look at this.

Shorting OTM ACN Puts and Calls

Shorting OTM ACN Puts. The table above shows that the put and call premiums are relatively high. That makes them attractive to short-sellers.

For example, the midpoint for the puts is $8.50, implying that a short seller of the $120.00 put earns a 2-month yield of 7.0833%. Here's why:

$850 income earned per put / $12,000 collateral required per put (i.e., cash-secured short-sale) = 0.070833 = 7.0833%

That works out to a per-month yield of 3.54%, which is quite attractive to short-sellers.

However, given that the delta ratio is over 42%, there is a very good chance that ACN could fall to $120 or lower. That means the short-sellers' accounts will be assigned to buy shares.

Not to worry. The breakeven point is much lower:

$120.00 - $8.50 = $111.50 breakeven point

$111.50 / $121.22 = -0.08 = 8% below today's price

In other words, this is a way for short-sellers to potentially set a lower buy-in point.

Shorting OTM Calls. Similarly, the out-of-the-money (OTM) call options at $130.00 have a high $6.00 midpoint premium. That implies a short-seller, especially a covered call seller, can make an attractive yield:

$600 / $12,122 (market price x 100 shares per call contract) = 0.0495 = 4.95% for 2 months

That works out to 2.475% per month for the next 2 months.

Moreover, covered call investors could make more money from capital gains if ACN rises from its present price to $130 or higher (i.e., maxed out at 7.24% if it moves from $121.22 to $130.00). So, the total potential return is 4.95% +7.24%, or 12.19%.

Spreads and Combinations. Some investors could short the calls to pay for buying puts, if they think ACN will keep falling. Others could short the puts to pay for the calls if they think ACN is bottoming out and ACN stock will rise.

Moreover, some could short both the puts and calls if they think ACN will stay within a range between today's price and $130.00.

The bottom line is that ACN's extreme move has brought out huge buyers and sellers of ACN options.

So, is ACN cheap here? It certainly looks so.

Fair Market Value for ACN Stock

Analysts surveyed by Yahoo! Finance (28 analysts) have an average price target of $197.95, or 63% over today's price. Similarly, Barchart's mean analyst survey price target is $228.92, or 89% highers.

Moreover, AnaChart's survey of 22 analysts, which tends to include more recent write-ups, shows an average price target of $256.00, or 111% higher than today's price.

This shows that analysts have strong recommendations that the sell-off in ACN stock looks well overdone.

Moreover, its average price/earnings (P/E) metric shows a similar result. For example, Morningstar shows that the stock's five-year average P/E has been 23.67x, and Seeking Alpha's forward P/E average is over 25x.

But management estimates this year it's earnings per share (EPS) will be between $13.38 and $13.50, or $13.44 at the midpoint. That puts its forward P/E at just 9x:

$121.22 / $13.44 = 9.02x

In other words, ACN stock is trading at less than 40% of its average forward P/E of 24x over the last 5 years.

That makes the stock look incredibly cheap, at least from an historical standpoint.

Summary and Conclusion

This could also be why investors are buying OTM calls or shorting OTM puts today, as seen in today's Barchart Unusual Stock Options Activity Report. By shorting OTM puts, they get a potentially lower buy-in, and they can use that income to buy these OTM calls.

Similarly, some investors may be buying puts and also buying calls. The puts will act as downside insurance for their long call purchases.

Or, as shown above, they could also be shorting both the OTM puts and calls, believing ACN will stay in a trading range.

But there are risks with that as well. For example, ACN could fall well below the short-put breakeven point over the next 60 days. But, at least, in that event, the investor has a lower potential buy-in price, given the huge potential upside in the stock over the long-term.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)