Valued at a market cap of $29.9 billion, Casey's General Stores, Inc. (CASY) is a leading convenience store chain and fuel retailer that operates primarily in small towns and rural communities across the Midwest and Southern United States. Headquartered in Ankeny, Iowa, the company is one of the largest convenience store operators in the country, with more than 2,800 locations across over 15 states.

Shares of CASY have outperformed the broader market over the past 52 weeks. CASY has soared 81.6% over this time frame, while the broader S&P 500 Index ($SPX) has gained 29.6%. In 2026, shares of CASY are up 46.4%, compared to SPX’s 9.8% increase on a YTD basis.

Narrowing the focus, CASY has also outpaced the State Street Consumer Discretionary Select Sector SPDR Fund’s (XLY) 13.4% rise over the past 52 weeks and marginal return on a YTD basis.

Casey's General Stores has outperformed the broader market over the past year due to strong execution across its prepared food business, resilient inside-store sales growth, and continued expansion through acquisitions and new store openings. Investors have been encouraged by the company’s ability to generate steady earnings growth despite a challenging consumer environment and volatile fuel margins. Additionally, Casey’s defensive business model has appealed to investors during periods of economic uncertainty.

On May 10, Casey's announced that it had been added to the S&P 500, reflecting the company’s strong financial performance, consistent growth, and resilient operating model.

For the year that ended in April 2026, analysts expect CASY’s EPS to improve 24.3% year over year to $18.19. The company’s earnings surprise history is stellar. It beat the consensus estimates in each of the last four quarters.

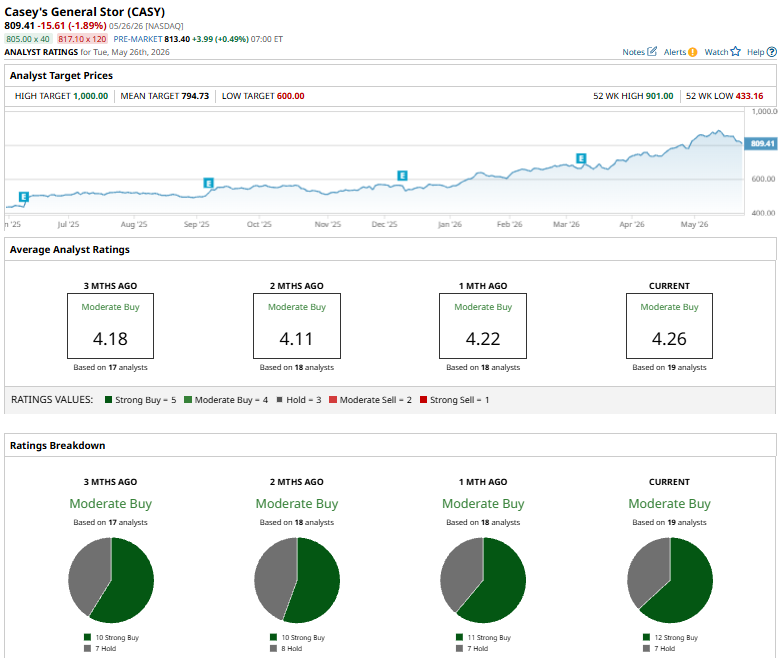

Among the 19 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 12 “Strong Buy” ratings and seven “Holds.”

This configuration is bullish than a month ago, when the stock had 11 “Strong Buy” suggestions.

On May 26, Wells Fargo raised its price target on Casey's to $910 from $745 while maintaining an “Overweight” rating on the shares. The firm noted that Casey’s fourth-quarter results could include a modest EPS miss due to weaker fuel margins, but added that the company’s initial fiscal 2027 guidance will likely be viewed as conservative given its strong history of outperforming expectations and its continued appetite for M&A following the integration of Fikes Wholesale.

While CASY currently trades above its mean price target of $794.73, the Street-high price target of $1000 implies a potential upside of 23.5% from the current price.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)