/Fair%20Isaac%20Corp_%20Logo%20and%20website%20on%20phone-by%20T_Schneider%20via%20Shutterstock.jpg)

Bozeman, Montana-based Fair Isaac Corporation (FICO) provides analytics software in the Americas and internationally. The company has a market capitalization of $28.8 billion and offers B2B scoring solutions and services for access to predictive credit scores and other scores, as well as B2C scoring solutions through its myFICO.com subscription offerings.

FICO shares have lagged behind the broader market over the past year and declined 25.6% compared to the S&P 500 Index ($SPX) 29.6% surge. Moreover, in 2026, the stock has fallen nearly 25.5%, underperforming the SPX’s 9.8% rise.

Focusing on its industry benchmark, the State Street Technology Select Sector SPDR ETF (XLK) has risen 63.3% over the past year, outperforming the stock. In 2026, as well, XLK surged 28.6% and has rallied the stock.

On Apr. 29, FICO stock rose 3.3% following the release of its Q2 2026 earnings. The company’s revenue for the quarter rose 38.7% from the prior year’s quarter to $691.7 million, surpassing Wall Street’s estimates. Moreover, its adjusted EPS came in at $12.50, also surpassing the Street’s forecasts. Fair Isaac expects full-year earnings to be $40.45 per share, with revenue expected to be $2.45 billion.

For the current year ending in September, analysts expect FICO’s EPS to rise 51.5% year over year to $37.99. Moreover, the company has surpassed analysts’ consensus estimates in three of the past four quarters, while missing it once.

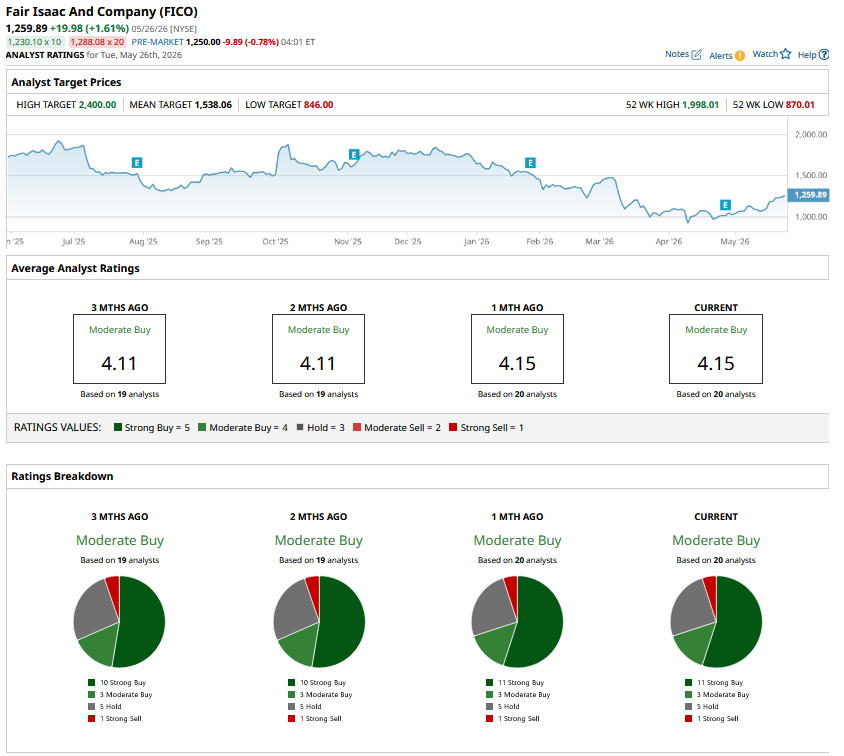

Among the 20 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 11 “Strong Buy” ratings, three “Moderate Buys,” five “Holds,” and one “Strong Sell.”

The configuration has remained unchanged over the past month.

On May 23, Deutsche Bank analyst Faiza Alwy maintained a “Buy” rating on Fair Isaac and set a price target of $1,658.

FICO’s mean price target of $1,538.06 indicates a premium of 22.1% from the current market prices. Its Street-high target of $2,400 suggests a robust 90.5% upside potential from current price levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Close-%20up%20of%20computer%20chip%20with%20AI%20sign%20by%20YAKOBCHUK%20V%20via%20Shutterstock.jpg)

/SpaceX%20rocket%20launch%20liftoff%20by%20Ryan%20Chylinski%20via%20Adobe%20Stock.jpeg)