Introducing The Spread Trader — A New Dimension of Market Analysis

At the Klarenbach Grain Report, our mission has always been to bring you the same calibre of analysis used by institutional traders, grain companies, and hedge funds operating in Chicago, London, New York, and Geneva.

Today, we are expanding that mission with the launch of a new content series: The Spread Trader.

To lead this series, we are proud to welcome Brent Futz as a guest contributor.

Brent brings a rare depth of experience to the Klarenbach Grain Report. His career spans the era of the open-outcry trading floor at the Winnipeg Commodity Exchange through to the modern electronic marketplace — a journey that has taken him through the roles of institutional trader, floor trader, broker, senior economist, and consultant.

Across those years, Brent has refined a disciplined approach to calendar spread trading that integrates seamlessly with both technical and fundamental analysis.

Brent holds a Master of Science in Agricultural Economics from the University of Manitoba, and it is that combination of academic grounding and real-world market experience that makes his

Commodity Futures Spreads

An Introduction to the Third Dimension

Introduction

Commodity futures trading strategies generally fall into two categories: technical or fundamental analysis. Commodity futures spreads, the difference in price of consecutive contracts, offer another dimension to those strategies.

A basic understanding of futures spreads supports and complements technical and fundamental strategies.

Commodity futures contracts are categorized by underlying product: energies, grains, livestock, softs, metals, currencies, indices, and financials. Within each category, futures contracts are settled by either physical delivery or cash settlement.

The introduction to futures spreads will focus on contracts settled by physical delivery and will use the canola futures contract and the WTI crude oil contract to present a trading strategy that transcends categories.

Effects of Contango and Backwardation on Open Interest

The spread between successive contracts is measured in dollars and cents. Spreads exhibit one of three relationships:

contango (the nearby contract is at a discount to the deferred contract),

even money (contracts are at the same price), and

backwardation (the nearby contract is at a premium to the deferred).

Table 1 lists the closing prices and open interest for canola and WTI crude oil futures for May 5, 2026.

The canola futures prices provide an example of successive spreads displaying a contango relationship, while the crude oil spreads are inverted and display a backwardation relationship.

Table 1: Canola Futures vs. WTI Crude Oil Futures

Closing prices and open interest, May 5,2026

Canola Futures WTI Futures

Contract | Close | O/I |

| Contract | Close | O/I |

|

July’26 | 757.30 | 178,171 |

| June’26 | 102.27 | 263,506 |

|

Nov’26 | 762.10 | 122,341 |

| July’26 | 98.07 | 186,910 |

|

Jan’27 | 768.80 | 23,659 |

| Aug’26 | 93.86 | 109,591 |

|

Mar’27 | 773.80 | 5,345 |

| Sept’26 | 89.92 | 133,951 |

|

The orientation of a spread can have significant implications for participants with open positions.

The open positions of a contract are collectively referred to as the open interest (OI) and are published weekly by the Commodity Futures Trading Commission (CFTC) in the Commitment of Traders Report (COT).

The CFTC records OI as either commercial or speculative, and as long or short. It is important to understand that within these categories, participants manage positions that may be considered perpetual.

Given that a very small percentage of contracts follow through the delivery process, it follows that the spread between contracts represents a cost to perpetual participants that “roll” their positions from nearby contracts to deferred contracts.

The spread or cost often determines the effectiveness of a trading strategy, whether its objective is to serve as a hedging strategy or a speculative position.

The July/Nov canola spread provides an empirical example of contango.

The July/Nov spread is currently trading at approximately $5 under.

For any perpetual long rolling a position forward, they are selling their long position and replacing it at a price $5 higher, thereby increasing the price of its average purchase price by $5.

Conversely, a perpetual short buying the July and selling the Nov at $5 is increasing the price of its average short position.

This example demonstrates how a spread trading at a contango works to the advantage of the short and disadvantage of the long, that is, there is a transfer of wealth from the long to the short.

The transfer of wealth is calculated by the tonnage represented by the open interest multiplied by the value of the spread (3.7 M tonnes x $2/tonne = $18.5M).

If the spread moves to $20 under, the transfer of wealth increases to $74M.

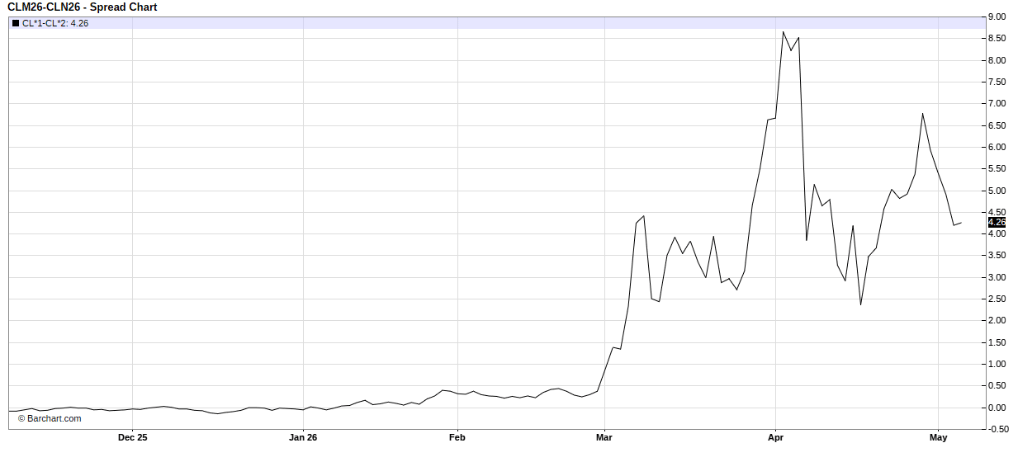

Chart 1 presents a depiction of the July/Nov canola spread trading at both backwardation and contango orientations over the past 6-month period.

Chart 1: July ‘26/Nov ‘26 Canola Futures Contract Spread

Chart 1: July ‘26/Nov ‘26 Canola Futures Contract Spread

Chart 2 depicts the June/July crude oil spread over the past 6-month period. Note the change in orientation from even money to backwardation at the beginning of the US-Iran war.

The current backwardation orientation allows the perpetual long to decrease the price of its average long position while the short decreases the average price of its short position.

There is a transfer of wealth from the short to the long.

Chart 2: June ‘26/July ‘26 WTI Crude Oil Futures Contract Spread

Chart 2: June ‘26/July ‘26 WTI Crude Oil Futures Contract Spread

Contango and Backwardation Parameters

The spread between successive futures contracts is not random, and contracts should not be considered as being independent of one another.

A contango orientation displays an intrinsic property of commodities, that is, there is a cost associated with the ownership of a commodity over time.

For commodity futures contracts, the maximum or full carrying charges between successive contracts are the sum of storage and interest costs.

Storage costs are usually fixed, while interest costs vary between participants.

The concept of full carrying charges is crucial to contract orientation because it allows traders to arbitrage between nearby and successive contracts when the spread exceeds full carry.

For example, during the liquidation of the May ‘26 canola contract, the May/July spread traded to $14 under; that is, the May contract traded at a $14 discount to the July.

Given that full carry charges were $15 for the May/July spread, traders could have guaranteed a profit by buying May and selling July at levels above $15.

Arbitraging two successive contracts at levels greater than full carry requires traders to take delivery of the underlying contract and redeliver during the delivery period of the successive contract.

In theory, traders' ability to arbitrage successive contracts is the underlying factor that prevents the nearby from becoming disconnected from the deferred and losing its intrinsic value.

The arbitrage trade at full carry underscores the importance of a properly functioning delivery system and sets a limit on the value of contango; the arbitrage opportunity prevents a spread from moving beyond full carry.

A difference between contango and backwardation orientation is that there are no parameters that limit backwardation; that is, there is no limit to an inverted spread.

An inverted spread implies that the market perceives a shortage in the near term, and participants are willing to forego storage costs to secure supplies.

The magnitude of the inversion is a measure of the perceived shortage.

The analysis of futures spreads has demonstrated the mechanics behind a transfer of wealth between long and short participants.

A complete analysis recognizes that hedgers can offset losses attributed to their futures position by a corresponding change in the value of their physical commodity.

For example, in an inverted spread, the short can offset their loss in their futures position by an equal appreciation in their physical commodity.

Nonetheless, the transfer of wealth resulting from the orientation of futures spreads underscores the importance of a strategic approach to commodity futures spreads.

Strategic vs. Passive Strategies

An orderly liquidation of the nearby contract typically occurs in the month preceding the first delivery day.

This characteristic of futures contracts suggests that a significant percentage of the participants use "time” to roll their positions into deferred contracts.

Futures contracts have been described as a zero-sum game in the context of game theory.

In that context, participants who use a passive approach, such as time to roll their positions forward, are at a disadvantage compared to those who take a more strategic approach.

Likewise, for those participants who base their strategy on technical or fundamental analysis, it is important to understand that spreads offer another dimension to their strategy.

Canola Corn Wheat CBOT Wheat HRW Soybeans Soybean Meal Soybean Oil Oil Gold Feeder Cattle Live Cattle

I cover this technical setup and specific price targets in depth in the Klarenbach Grain Report.

Join 3,500+ farmers getting sell signals and technical roadmaps here:

Trent Klarenbach, BSA AgEc, PAg, publishes the Klarenbach Grain Report and the Klarenbach Special Crops Report.

Klarenbach Research

Sign up below for a FREE trial of our newsletters

/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/A%20concept%20image%20of%20a%20flying%20car_%20Image%20by%20Phonlamai%20Photo%20via%20Shutterstock_.jpg)

/Palantir%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)