/Applied%20Materials%20Inc_%20mobile%20and%20computer%20logo-by%20vieimage%20via%20Shutterstock.jpg)

The semiconductor story has turned back into a spending story. Semiconductor stocks now account for 14% of the S&P 500 ($SPX), getting a boost from higher memory prices, automotive chips recovering, and new factory construction that still needs more clean rooms and equipment.

Taiwan Semiconductor (TSM) expects around $54 billion in 2026 capital expenditures, Micron (MU) sees capex rising to $25 billion, and several new plants won't open until 2027 or 2028. That's why chip-equipment companies remain central to the artificial intelligence (AI) trade right now.

Applied Materials (AMAT) is right in the middle of that buildout. The company is benefiting from AI-driven demand, advanced packaging growth, and customer spending on foundry, logic, and memory. The company's latest systems are built to handle atomic-scale manufacturing problems for next-generation AI chips. That's why Seaport recently turned bullish on AMAT stock and lifted its price target to $500, putting fresh attention on a company already near the center of the semiconductor equipment chain.

If AI infrastructure spending is still early and Applied Materials is supplying the tools that make that growth possible, how much further can AMAT stock go? Let's take a closer look.

Breaking Down Applied Materials' Financial Performance

Applied Materials supplies the manufacturing equipment and engineering tools that chipmakers use to build advanced logic and memory chips. Shares of AMAT sotck have surged 164% over the past 52 weeks and are up another 60% year-to-date (YTD) as investors bet on its AI exposure.

That rally has pushed the stock's valuation well above sector averages. AMAT now trades at a forward price-to-earnings (P/E) ratio of 36.8 times compared to the sector average of 24 times.

Still, Applied Materials keeps returning cash to shareholders with a quarterly dividend of $0.46, which works out to annualized dividend of $1.84 and a 0.45% yield. The payout ratio sits at 18.77%, and the company has raised its dividend for nine-straight years.

The business itself remains solid. In the first quarter of 2026, revenue came in at $7.01 billion, down 2% year-over-year (YOY). However, profitability stayed strong with GAAP EPS of $2.54, up 75% YOY, and non-GAAP EPS of $2.38, which remained flat YOY. Gross margins held at about 49%, and operating income hit $1.83 billion.

Some bright spots included record DRAM revenue in Semiconductor Systems and record services and spares revenue in Applied Global Services. The company generated $1.69 billion in operating cash flow and returned $702 million to shareholders through $337 million in buybacks and $365 million in dividends.

What Is Driving Applied Materials' Growth?

Applied Materials recently entered a definitive agreement to acquire NEXX from ASMPT Limited, a top supplier of large-area advanced packaging equipment. The deal expands Applied Materials' panel-level packaging portfolio, which helps chipmakers build larger AI accelerators that use less power. As AI workloads push demand for more complex designs that combine multiple GPUs, high-bandwidth memory stacks, and I/O chips, the industry is moving from 300-millimeter wafers to panel formats as large as 510 by 515 millimeters or more. This shift supports the 2.5D and 3D chiplet stacking needed for larger interposers and advanced substrates, letting designers scale AI chip packages and boost output.

In April, Applied Materials also introduced two deposition systems built for angstrom-era logic chips, controlling materials with atomic-level precision. These systems let chipmakers build Gate-All-Around (GAA) transistors at 2 nanometers and beyond, delivering faster and more power-efficient performance.

Separately, Applied Materials has partnered with Micron to develop next-generation DRAM, high-bandwidth memory, and NAND for AI applications. The partnership brings together R&D from Applied Materials’ EPIC Center in Silicon Valley and Micron's Boise facility, working on advanced materials, process technologies, architectures, and packaging to deliver high-bandwidth, low-power memory for power-hungry AI workloads while strengthening the U.S. semiconductor pipeline.

What Does Wall Street Think of AMAT Stock?

For the current quarter, analysts expect EPS of $2.67, up 12% from last year's $2.39 per share. For the next quarter ending in July, estimates are for $2.94 per share, up almost 19% from $2.48 a year ago. Full fiscal year 2026 estimates point to EPS of $11.14, up 18% from $9.42.

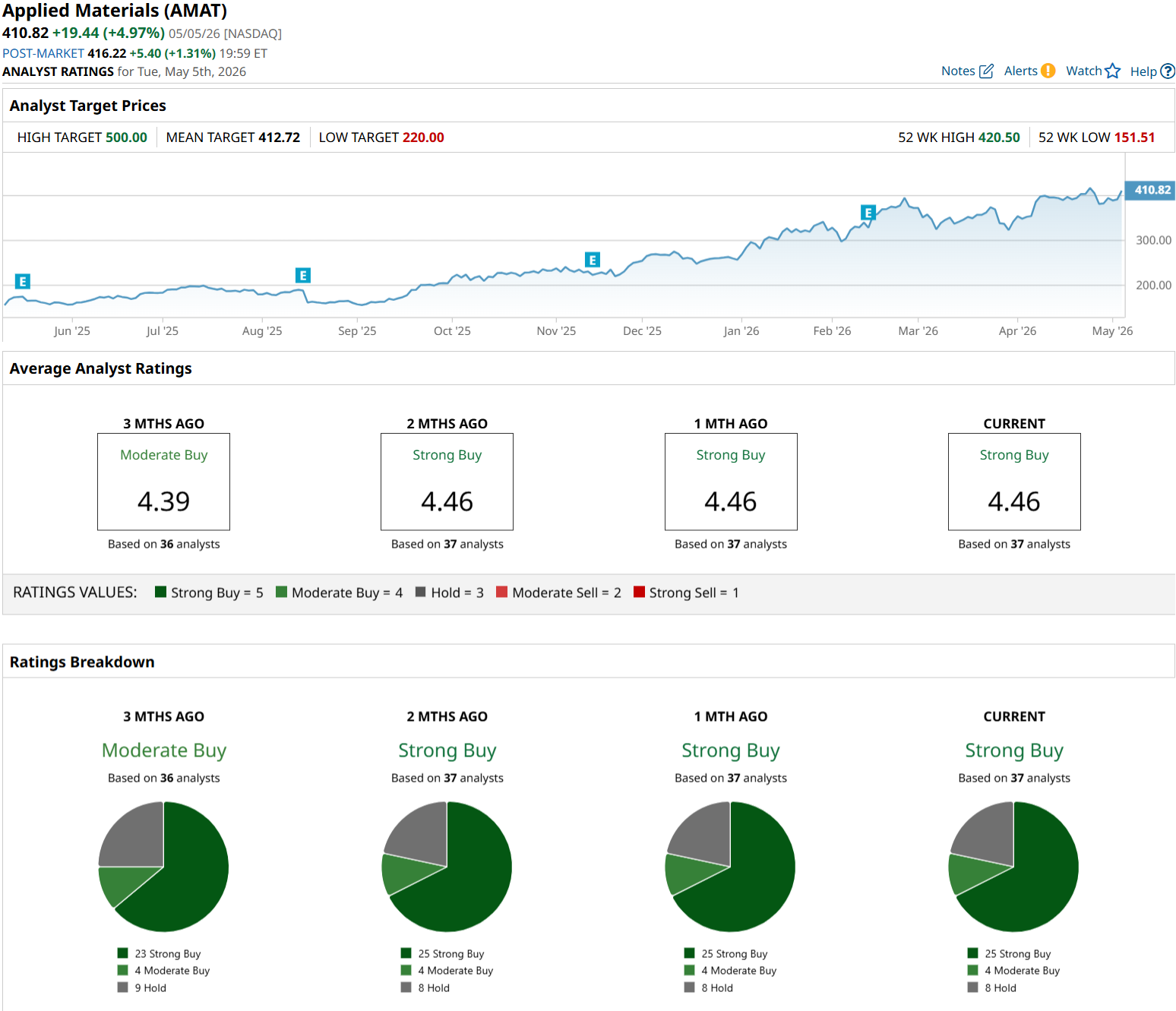

Deutsche Bank analyst Melissa Weathers upgraded AMAT stock to “Buy” from “Hold” with a $390 target in January, saying the outlook for wafer fabrication equipment spending had improved. Wells Fargo's Joe Quatrochi also kept his “Overweight” rating with a $435 target after Applied Materials' latest earnings, noting that the company's expected 20%-plus growth in semiconductor systems revenue was running “well ahead” of analyst expectations.

Based on 38 analysts covering the stock, Applied Materials has consensus “Strong Buy" rating. The average price target is $417.55, which implies about 2% potential upside from current levels. Seaport's high target of $500 implies potential upside of 22% from here.

Conclusion

Applied Materials has built a compelling case for continued relevance in the AI semiconductor buildout, with strategic moves in advanced packaging, angstrom-era deposition, and memory solutions that directly address where chip manufacturing is heading. The new $500 Street-high price target from Seaport underscores that positioning, although the valuation already reflects much of the optimism. Still, with double-digit earnings growth projected through fiscal 2027 and major chipmakers committed to multi-year capex cycles, the fundamentals appear solid enough to support further gains. The current setup looks to favor gradual upside for those willing to pay a premium for what analysts view as an almost irreplaceable role in the AI supply chain.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)