/Computer%20memory%20closeup%20by%20Nor%20Gal%20via%20Shutterstock.jpg)

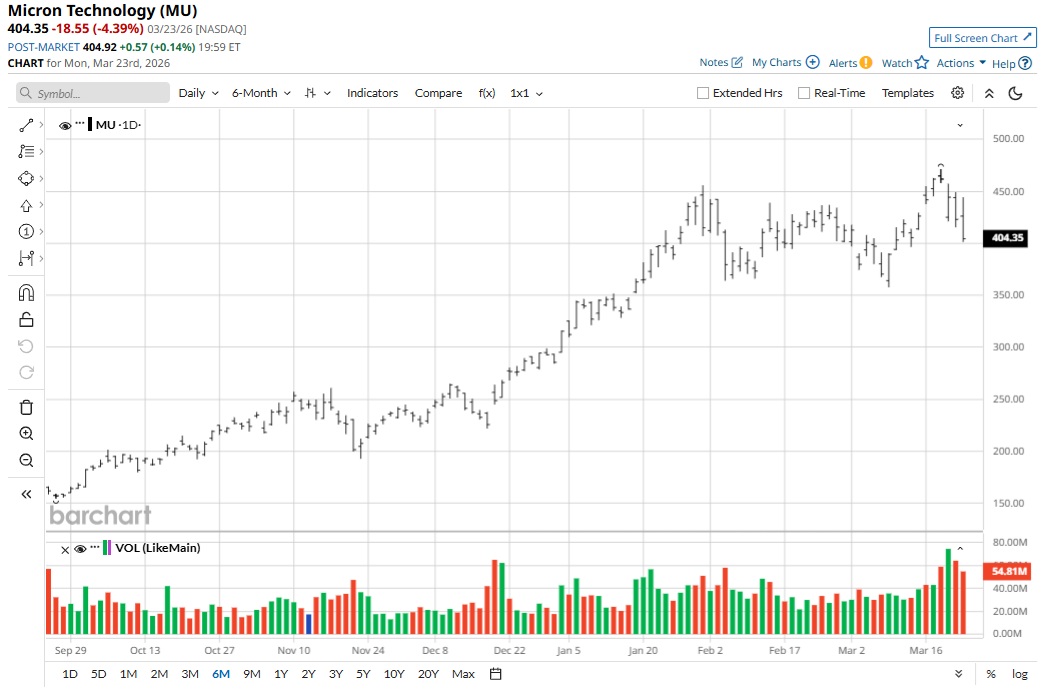

Micron Technology (MU) stock has surged by 306% in the last 52 weeks amid swelling demand for memory for artificial intelligence (AI). This rally has been fundamentally backed by stellar growth and significant cash flow expansion.

However, MU stock seems to have taken a breather after second-quarter results with a correction of 19% from all-time highs. With structural tailwinds for memory and storage products, the correction seems like a good buying opportunity.

Recently, Wedbush opined that, amid the tight demand-supply scenario, some memory prices may surge by more than 100%. This is expected to be positive for the likes of Micron, Seagate Technology (STX), and Western Digital (WDC). Prices trending higher would imply continued positive impact on the top line as well as EBITDA margin expansion.

Following Micron's Q2 earnings, Citi also reiterated a “Buy” rating on MU stock and increased its price target from $430 to $510. With a bullish industry and company-specific view, Micron looks interesting at current levels.

About Micron Stock

Headquartered in Boise, Idaho, Micron is among the leading global players in innovative memory and storage solutions. The company’s current portfolio includes DRAM, NAND, and NOR memory and storage products. The global product portfolio also includes solid-state drives, graphics and high-bandwidth memory, and managed NAND and multichip packages. Product portfolio expansion is likely to sustain considering the company's focus on innovation. Micron has more than 60,000 granted patents globally.

Micron’s core business units include Cloud Memory, Core Data Center, Mobile & Client, and Automotive & Embedded. All of these business segments witnessed year-over-year (YOY) revenue growth in excess of 150% in Q2 fiscal 2026.

For Q2, DRAM represented 79% of total revenue, with 21% coming from NAND. Micron reported robust top-line growth of 197% YOY to $23.9 billion. For the same period, operating cash flow (OCF) was $11.9 billion, implying annualized OCF potential of nearly $50 billion.

With industry tailwinds, robust growth, and a surge in cash flows, MU stock has rallied by 144% in the last six months. Considering the tight demand-supply scenario for memory products, upside will likely sustain.

Significant Investments to Boost Growth

Micron's projected capital investments are an indication of impending demand and growth potential. For fiscal 2026, Micron has guided for capex of $25 billion. For fiscal 2027, capex is likely to support HBM- and DRAM-related investments.

An important point to note is that Micron is building global manufacturing sites to ensure ample opportunities from emerging markets. For example, the company recently inaugurated India’s first semiconductor assembly and test facility with an investment of $2.75 billion. The company will also be investing $24 billion in an advanced wafer fabrication facility in Singapore over the next 10 years.

While these investments are significant, financing growth is unlikely to be a concern. As of Q2, Micron reported a cash buffer of $20.2 billion, while adjusted free cash flow was $6.9 billion. With robust growth and visibility for cash flow upside, Micron is positioned for big investments and continued buybacks to create shareholder value.

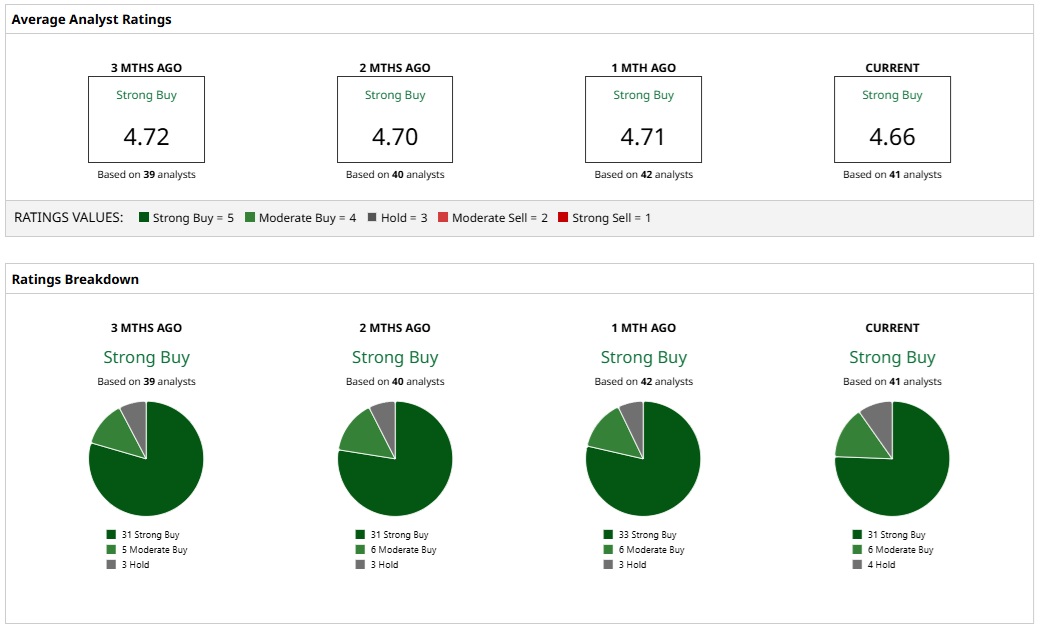

What Do Analysts Say About MU Stock?

Based on 41 analysts with coverage, MU stock has a consensus “Strong Buy" rating. While 31 analysts have a “Strong Buy” rating for Micron, six analysts have a “Moderate Buy” rating, and four analysts have a “Hold.”

The mean price target of $489.29 represents potential upside of about 28% from current levels. Further, the most bullish price target of $750 suggests that MU stock could climb 96% from here.

It’s worth noting that, for fiscal 2026 and fiscal 2027, analyst estimates point to earnings growth of 622% and 64%, respectively. With robust growth likely, a forward price-to-earnings (P/E) ratio of 10.1 times looks attractive and points to further upside for MU stock. The correction from highs therefore seems like a good buying opportunity.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)