Valued at a market cap of $108.2 billion, The Southern Company (SO) is an integrated energy provider, delivering a comprehensive suite of utility and infrastructure solutions. The Atlanta, Georgia-based company generates, transmits, and distributes reliable electricity and natural gas, supported by a massive fleet that includes industry-leading nuclear capacity, modern natural gas facilities, and a rapidly expanding renewable energy portfolio.

This utility company has underperformed the broader market over the past 52 weeks. Shares of SO have gained 5.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 28.5%. However, on a YTD basis, the stock is up 10%, outpacing SPX’s 6% rise.

Narrowing the focus, SO has also lagged the State Street Utilities Select Sector SPDR ETF (XLU), which soared 16.6% over the past 52 weeks. Nonetheless, it has outpaced XLU’s 8.6% YTD rise.

On Apr. 30, shares of SO soared 3.4% after it delivered better-than-expected Q1 earnings results. Due to higher electric and natural gas revenue, the company’s total operating revenue increased 8% year-over-year to $8.4 billion, surpassing consensus estimates by 3.8%. Moreover, its adjusted EPS of $1.32 grew 7.3% from the same period last year, handily topping analyst expectations of $1.21.

For the current fiscal year, ending in December, analysts expect SO’s EPS to grow 6.3% year over year to $4.57. The company’s earnings surprise history is mixed. It topped the consensus estimates in three of the last four quarters, while missing on another occasion.

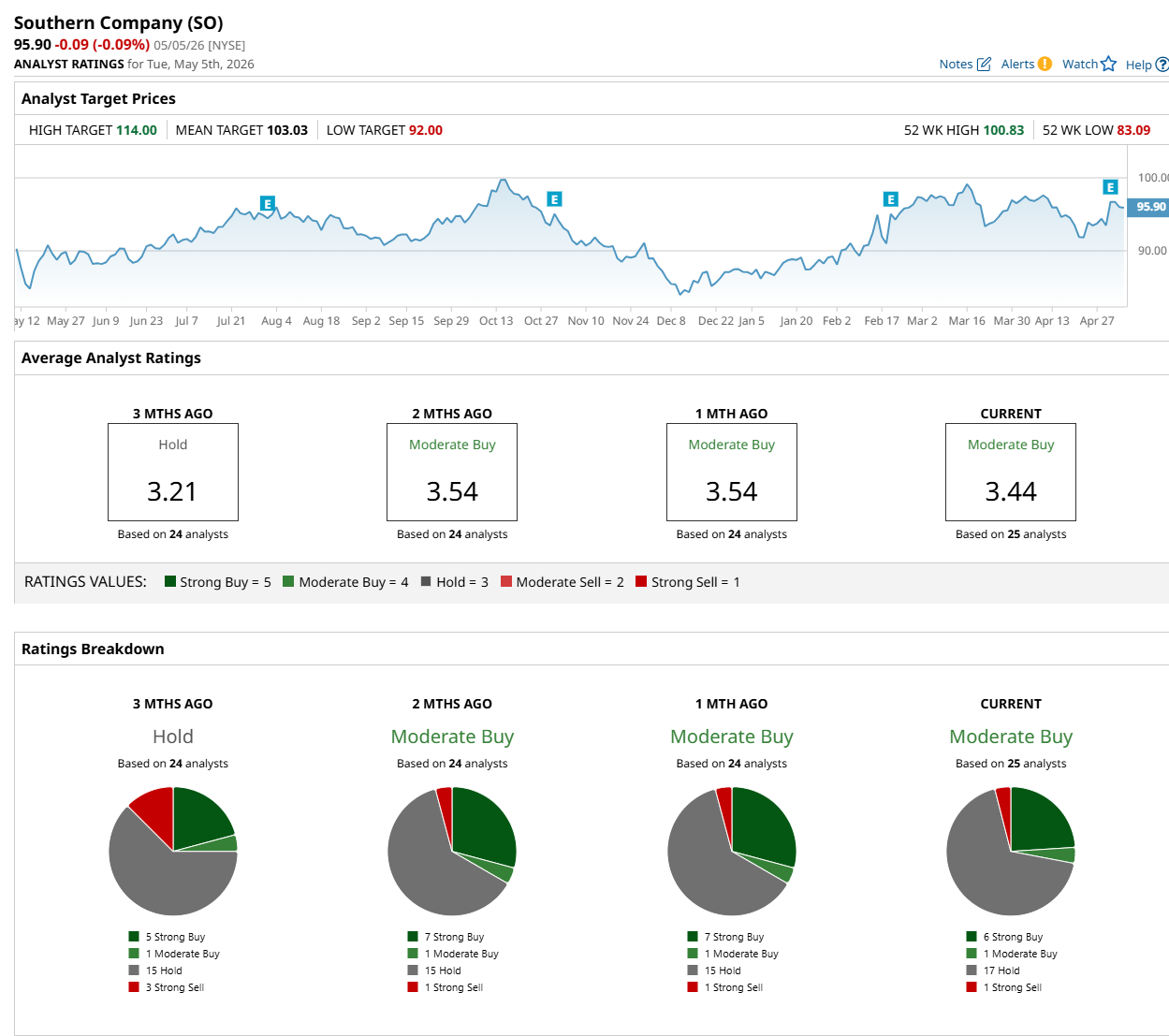

Among the 25 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on six “Strong Buy,” one “Moderate Buy,” 17 "Hold,” and one “Strong Sell” rating.

The configuration is slightly less bullish than a month ago, with seven analysts suggesting a "Strong Buy” rating.

On May 4, Argus Research maintained a “Buy” rating on SO, with a price target of $101, indicating a 5.3% potential upside from the current levels.

The mean price target of $103.03 suggests a 7.4% premium to its current levels, while its Street-high price target of $114 implies an 18.9% potential upside from the current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)