November soybean futures have pushed higher as the market continues to price in strong domestic demand tied to the renewable diesel sector. USDA's May WASDE report projected U.S. soybean crush at a record 2.75 billion bushels for the 2025/26 marketing year, reflecting favorable processor margins and continued expansion in biomass-based diesel demand. Even with U.S. production forecast to rebound to 4.435 billion bushels, rising crush demand is tightening the balance sheet and limiting the potential for burdensome carryout growth. For soybean traders and hedgers, the key point is that domestic demand is now providing a stronger floor underneath the market than in previous years, particularly during seasonal periods when export demand alone would not normally support rallies.

Seasonally, soybean futures often build strength into the summer weather market, and this year's move has been reinforced by improving technical momentum and renewed trade optimism. Expectations for additional U.S.-China agricultural agreements have added a risk premium to the export outlook, despite large South American supplies remaining available on the world market. From a chart perspective, November futures have maintained higher lows and attracted buying on breaks, a sign that commercial and speculative participants are willing to defend support levels. If crush demand remains near current projections and export commitments improve, the market could continue its typical seasonal tendency of holding strength through key growing-season months.

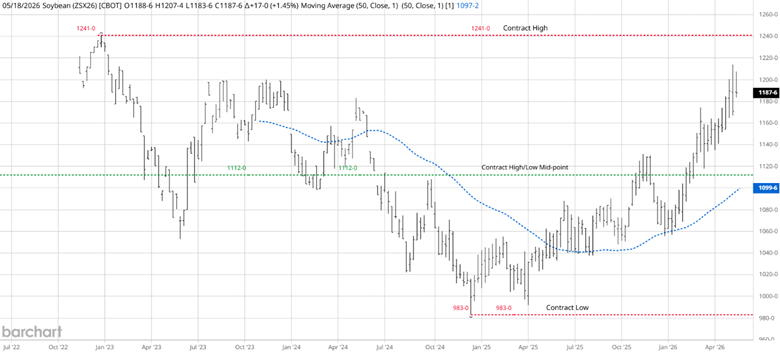

November Soybean Technical Picture

Source: Barchart

The weekly chart of the November Soybean futures shows the contract low, set in January 2025, at $9.83 per bushel. The contract high was set earlier in the contract life at $12.41 per bushel in January 2023. During the recent rally off the contract lows, the market initially found resistance at the mid-point of the contract high/low and retraced back to the rising 50 simple moving average (SMA) before resuming the rally. The next occurrence at the mid-point, the November contract traded higher. Soon after, the market retraced to the mid-point, which had then become support, and rallied off the retest to current levels. Technically, the November futures look strong and poised to challenge the contract's high.

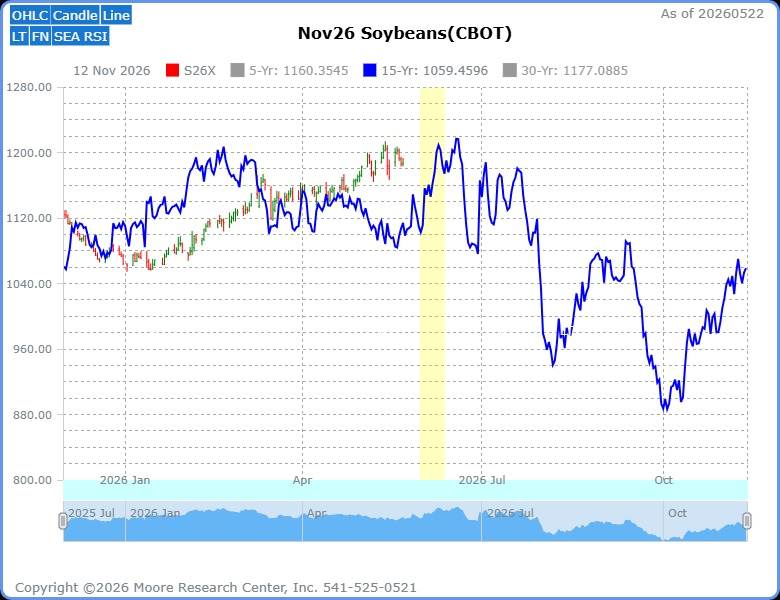

Seasonal Pattern

Source: Moore Research Center, Inc. (MRCI)

With the uptrend in place and price near the contract high, MRCI's research has identified a seasonal buying pattern (yellow box) that may drive the contract to new highs or into a retest. The 15-year average price (blue line) shows that prices peak in mid to late June, then decline into the harvest season. The 15-year average gives us a macro view of price action over the year, but MRCI research goes further, refining the data into optimal seasonal windows. This year, their research reveals that the November soybean futures contract has closed higher on approximately June 12 than on May 31 for 12 of the past 15 years, an 80% occurrence. The optimal window is shorter, only 13 calendar days. Allowing traders to position for this move up into the seasonal highs and then consider reversing their positions as the seasonal highs begin to show signs of weakness.

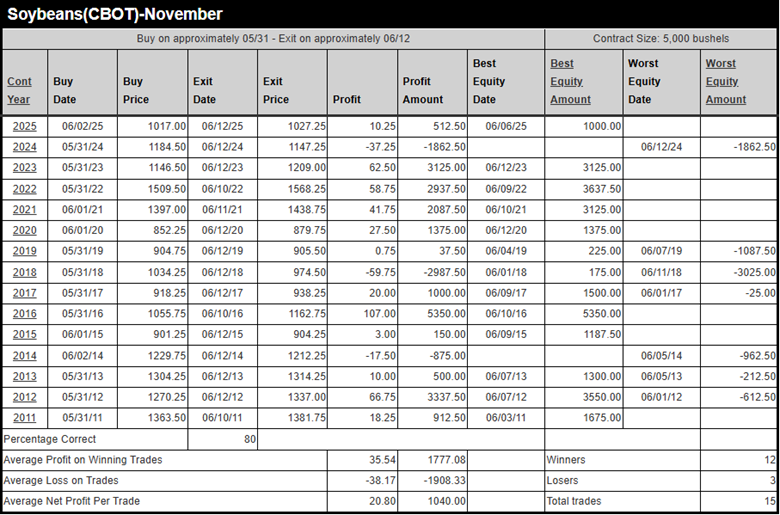

Source: MRCI

During hypothetical testing, this pattern has returned an average net profit of almost .21 or $1,040 per contract. What stands out about this seasonal pattern is the number of years without daily closing drawdowns, a whopping 8 of the 15 years. With this type of pattern, there appears to be a fundamental, repetitive reason for these statistics.

As a crucial reminder, while seasonal patterns can provide valuable insights, they should not be the basis for trading decisions. Traders must consider technical and fundamental indicators, risk management strategies, and market conditions to make informed, balanced trading decisions.

Assets to Trade Soybeans

Soybean Futures Contracts - Standard (ZS) Mini (XK):

- Soybean futures, traded on the Chicago Board of Trade (CBOT) through CME Group, are standardized contracts that allow buyers and sellers to agree on a price for soybeans to be delivered on a future date (e.g., November 2026 futures).

- Options on soybean futures, also traded on CBOT, give speculators the right, but not the obligation, to buy (call) or sell (put) soybeans at a specific price before or at expiration. These are useful for seasonal trading, allowing speculators to capitalize on price volatility (e.g., weather-driven spikes in June) with defined risk.

Agricultural ETFs (SOYB):

- Exchange-traded funds (ETFs) provide exposure to soybeans without direct futures trading. Making it accessible for speculators targeting seasonal price movements in soybeans.

In Closing…

For traders and hedgers, the current soybean market is offering more than just a seasonal setup. Strong crush demand tied to renewable diesel, improving technical structure, and supportive seasonal tendencies are all aligning at a time when the market continues to respect key support levels. While no seasonal pattern guarantees future performance, the historical consistency in this June window deserves attention — especially considering the pattern produced no daily closing drawdowns in 8 of the past 15 years during hypothetical testing. In a market where risk management is everything, that type of historical stability can be just as important as the profit potential. As weather and export developments take center stage in the weeks ahead, November soybeans remain a market that traders and hedgers will want to keep firmly on the radar.

On the date of publication, Don Dawson did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)