Valued at a market cap of $334 billion, The Procter & Gamble Company (PG) is a manufacturer of consumer packaged goods that serve as daily essentials for billions of people worldwide. The Cincinnati, Ohio-based company focuses on providing superior-quality, high-performance products across a streamlined portfolio of trusted, iconic brands.

This FMCG company has lagged the broader market over the past 52 weeks. Shares of PG have declined 10.7% over this time frame, while the broader S&P 500 Index ($SPX) has gained 26.6%. Moreover, on a YTD basis, the stock is up marginally, compared to SPX’s 5.2% rise.

Looking closer, PG has also underperformed the State Street Consumer Staples Select Sector SPDR Fund’s (XLP) 2.4% rise over the past 52 weeks and 7.5% uptick on a YTD basis.

On Apr. 24, shares of PG surged 1.7% after it delivered stronger-than-expected Q3 results. The upbeat performance was driven by broad-based volume growth and continued product innovation, with particularly strong contributions from the Skin and Personal Care segment, along with successful launches in cleaning and hair care products.

Its total revenue increased 7.4% year-over-year to $21.2 billion, exceeding consensus estimates by 3.6%. However, amid ongoing cost pressures, its adjusted EPS grew modestly by 3.2% from the prior-year quarter to $1.59, still beating analyst expectations of $1.56.

For the current fiscal year, ending in June, analysts expect PG’s EPS to grow 1.3% year over year to $6.92. The company’s earnings surprise history is promising. It topped the consensus estimates in each of the last four quarters.

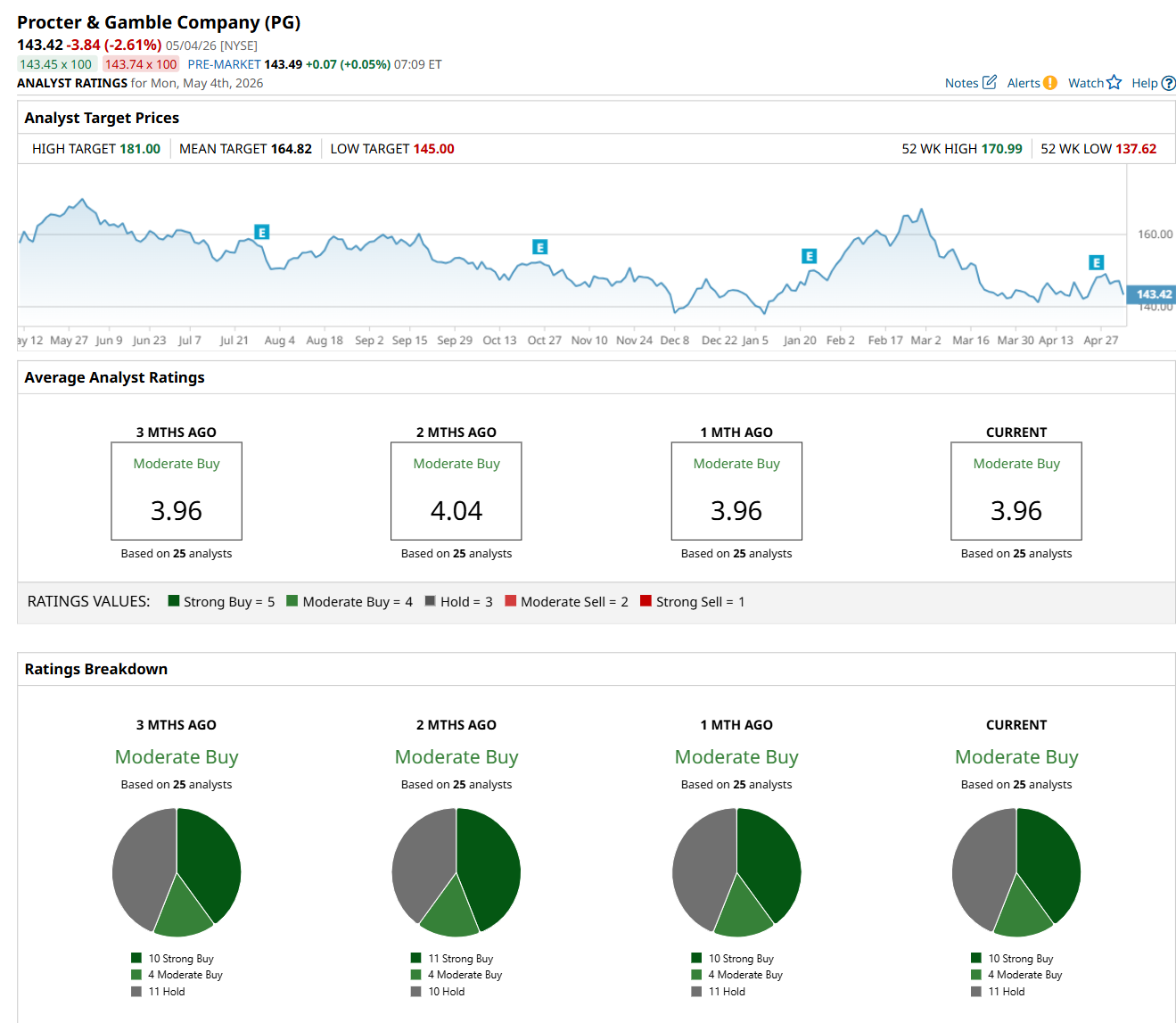

Among the 25 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on 10 “Strong Buy,” four “Moderate Buy,” and 11 “Hold” ratings.

The configuration is less bullish than two months ago, with 11 analysts suggesting a "Strong Buy" rating.

On Apr. 28, JPMorgan Chase & Co. (JPM) analyst Andrea Faria Teixeira maintained a “Buy” rating on PG and set a price target of $164, indicating a 14.3% potential upside from the current price levels.

The mean price target of $164.82 suggests a 14.9% premium to its current price levels, while its Street-high price target of $181 implies a 26.2% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)