/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

Tesla (TSLA) is back under the spotlight, though not quite for the reasons optimists would have scripted. Shares dipped following the company's Q1 earnings release on April 22, as a steeper-than-anticipated capital expenditure ramp spooked investors. Yet even as spending concerns cloud the near-term outlook, a compelling new narrative is quietly gathering momentum on Wall Street, one that could provide meaningful support for the stock.

At the center of it is SpaceX, Elon Musk's high-profile space venture, which is widely anticipated to go public later this year at a valuation nearing $2 trillion. Layered on top of that is swirling speculation around a potential Tesla-SpaceX merger, adding an extra dimension of intrigue that's hard for the market to ignore. While most analysts have kept their commentary focused on Tesla's expanding product pipeline, many caution that fading the stock entirely carries real risk with such a powerful catalyst looming.

Recently, Craig Irwin of Roth Capital pointed to Tesla's Q1 performance as evidence of resilient demand trends, sound pricing discipline, and a tailwind from select one-time factors. Looking ahead, Roth expects the anticipated SpaceX IPO to dominate the Tesla conversation in the near term, with ripple effects ranging from potential Cybertruck demand to the prospect of a deeper strategic alliance between the two Musk-led enterprises. On the back of that view, Roth reaffirmed its "Buy" rating on TSLA and a $505 price target. So, given this bullish outlook, here's a closer look at where Tesla's fundamentals actually stand.

About Tesla Stock

Founded in 2003 and headquartered in Austin, Texas, Tesla set out to make electric vehicles (EVs) the norm rather than the exception. Under the leadership of CEO Elon Musk, the company built its reputation on combining cutting-edge technology with genuine desirability, producing a lineup that grew from the niche, high-performance Roadster to the widely accessible Model 3 and Model Y, vehicles that collectively helped shift the global auto industry's direction.

What started as an EV company, though, has now grown into something far broader. Tesla today spans energy storage, solar power, AI, and robotics, with products like the Megapack, its Full Self-Driving (FSD) software, and the forthcoming Optimus humanoid robot reflecting just how far its ambitions have stretched. The company increasingly views itself not merely as an automaker but as a technology and energy platform, one using artificial intelligence (AI) and innovation as the backbone of everything it builds.

Currently sitting at a market capitalization of around $1.40 trillion, Tesla's stock has had a rough ride in 2026, weighed down by a combination of slowing EV demand, an aggressive capital expenditure outlook, and growing skepticism around its bold ambitions to reinvent itself as a physical AI company. After delivering an impressive 45% gain in 2025, the momentum has decisively faded.

TSLA shares have shed 16.33% year-to-date (YTD), a stark contrast to the S&P 500 Index ($SPX), which has gained roughly 4.67% over the same period. The pullback looks even sharper when measured from the stock's December peak of $498.83. Tesla has since tumbled 32.6% from that high. In fact, Tesla has also emerged as the worst-performing stock among the “Magnificent Seven” group this year, underscoring the rapid pace at which sentiment has cooled despite its long-term ambitions.

A Look Inside Tesla’s Q1 Financial Performance

Tesla’s fiscal 2026 first-quarter results, released on April 22, painted the picture of a company in the middle of a costly transformation, one that didn’t sit well with investors, sending the stock down roughly 3.6% in the following session. At first glance, the numbers were strong. Revenue grew 16% year-over-year (YOY) to $22.39 billion, beating expectations of $21.92 billion, while adjusted EPS came in at $0.41, topping the $0.36 estimate and jumping 52% from last year. Dig a little deeper, and it’s clear the core EV business is still doing the heavy lifting.

Automotive revenue shot up about 16% to $16.2 billion from $14 billion a year ago, proving that the legacy segment continues to anchor overall performance. Margins also showed meaningful improvement. Total GAAP gross margin expanded to 21.1% from 16.3% last year, while automotive gross margin, excluding regulatory credits, climbed to 19.2%, rebounding sharply from 12.5% in Q1 2025 and improving from 17.9% in the prior quarter.

However, Tesla isn’t pretending everything's rosy. The company flagged growing competitive pressure and an aging lineup, with plans to introduce more affordable versions of its Model Y SUV and Model 3 sedan. This comes as rivals, particularly Chinese players like BYD Company (BYDDY) and Xiaomi (XIACY), continue to push out newer, cheaper, and increasingly sophisticated vehicles.

From a liquidity standpoint, Tesla's position remains enviable. The company closed the quarter with $44.7 billion in cash, cash equivalents, and short-term investments, up slightly from $44.1 billion. That improvement was fueled by $1.4 billion in free cash flow and $1.2 billion from financing activities, though a $2 billion equity stake in SpaceX trimmed some of those gains. Still, the number that really rattled investors was the dramatic ramp in planned spending tied to Tesla's "Physical AI" vision.

The company raised its 2026 capital expenditure guidance to over $25 billion, a steep jump from $8.6 billion in 2025, as it ramps up investments in AI infrastructure, new products, and manufacturing capacity. Further, management warned that this heavy spending intensity, especially around AI training clusters and the Cybercab supply chain, could push free cash flow into the red for the rest of the year.

On the horizon, Tesla is prioritizing efficiency over expansion, focusing on maximizing output from current facilities before building new ones. Its next-generation lineup, Cybercab, Semi, and Megapack 3, remains on schedule for volume production in 2026. And early Optimus assembly lines are already being installed, pointing to a future where Tesla's identity stretches well beyond EVs into a broader AI-driven platform.

How Are Analysts Viewing Tesla Stock?

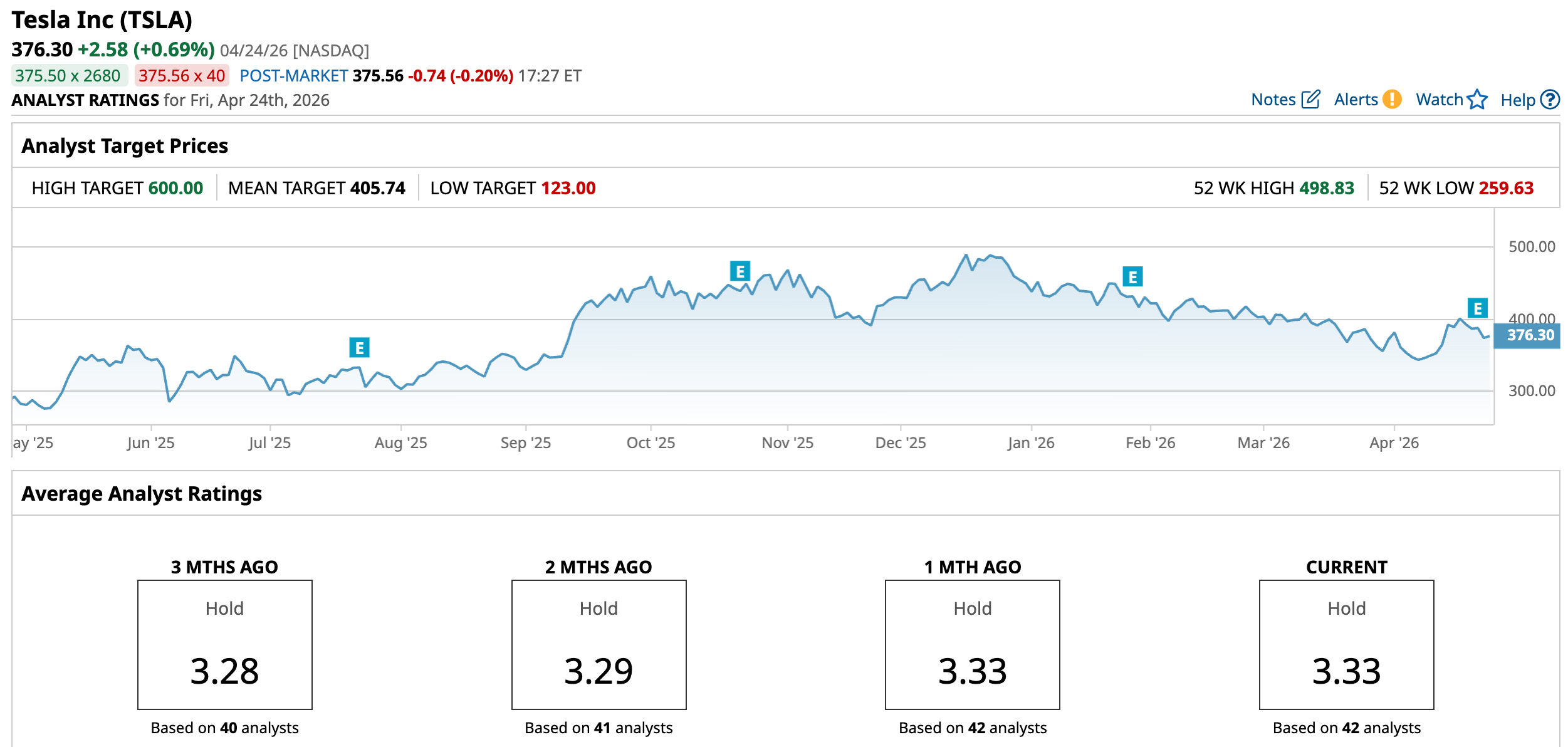

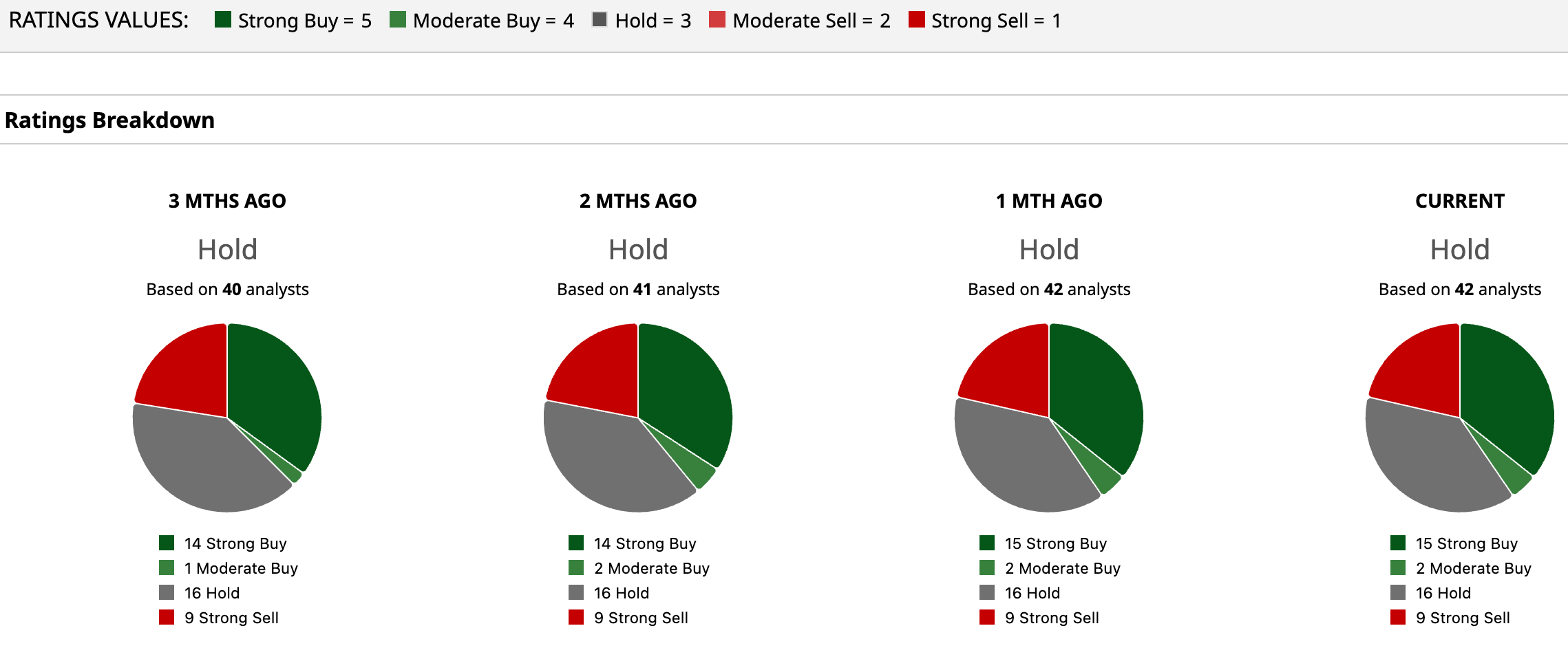

Despite Roth Capital’s optimistic outlook on Tesla, Wall Street’s overall stance on the company remains anything but unified, with the stock carrying a consensus “Hold” rating as opinions pull in opposite directions. Out of 42 analysts, 15 are firmly bullish with “Strong Buy” ratings, two lean “Moderate Buy,” 16 are sitting it out with “Hold,” and nine are outright bearish with “Strong Sell” calls.

The average price target of $405.74 points to a relatively modest 7.8% upside, signaling restrained expectations in the near term. However, the Street-high target of $600 implies a potential upside of as much as 60%, highlighting the wide divergence in views on where Tesla could ultimately head.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.