/Apple%20Inc%20Tim%20Cook-by%20John%20Gress%20Media%20Inc%20via%20Shutterstock.jpg)

Tech giant Apple (AAPL) is enjoying strong backing from Wall Street as it prepares to report its fiscal 2026 Q2 results later this month, building on the momentum of a blockbuster Q1 in late January. According to Morgan Stanley, the April 30 earnings could act as a crucial “clearing event,” one capable of resetting investor sentiment and potentially opening the door for a move toward the $300 level by September.

Analyst Erik Woodring noted that while gross margins may face some pressure from rising memory costs, stronger revenue in the June-quarter outlook is expected to more than offset that weakness. This could lead to a “better-than-feared” earnings outcome and serve as a catalyst heading into Apple’s Wordwide Developers Conference (WWDC) in June and its iPhone launch in September. Even with margins tracking below consensus, continued strength across iPhone, Mac, and Services is likely to keep earnings guidance broadly in line with Street expectations, which would still come as a positive surprise given relatively low expectations.

Woodring emphasized that the company is entering a “seasonally strong period of outperformance,” regardless of near-term results. He expects revenue growth to remain robust, potentially around 15%, supported by share gains across multiple markets. Historically, this time of year has also seen valuation multiples expand ahead of a new iPhone cycle. At the same time, expectations for Apple’s developer conference remain muted, while talk of a foldable iPhone this fall could spark fresh excitement.

So, given this bullish outlook, here’s a closer look at Apple stock as it gets ready to lift the curtain on its highly anticipated Q2 earnings report after the market hours on Thursday, April 30.

About Apple Stock

Headquartered in Cupertino, California, Apple has firmly cemented itself as one of the most dominant forces in global technology. Its strength lies not just in iconic products like the iPhone, Mac, Apple Watch, and AirPods, but in how seamlessly these devices are woven together through a tightly integrated ecosystem of hardware, software, and services, creating a unified, stickier user experience that keeps customers within its orbit.

Beyond devices, Apple’s footprint spans smartphones, personal computing, digital content, and cloud services. At the same time, the company is steadily leaning into future-facing areas such as artificial intelligence (AI), wearables, and mixed reality, signaling a strategy that blends innovation with its established strengths rather than depending solely on its legacy franchises.

Apple made headlines on April 20 with a major leadership shake-up, announcing that CEO Tim Cook will step down from his role on Sept. 1 after more than a decade at the helm. Cook isn’t exiting entirely. He will transition into the role of executive chairman, where he will continue supporting the company, including engaging with global policymakers. Stepping into the top job will be John Ternus, Apple’s senior vice president of Hardware Engineering, signaling a new chapter for the tech giant.

The leadership transition comes at a critical juncture for Apple as it steps up efforts to close the gap in AI, a space where rivals like Microsoft (MSFT) and Alphabet (GOOG) (GOOGL) have pulled ahead. The company is expected to unveil a revamped Siri powered by Google’s Gemini AI models at its WWDC conference this June, signaling a more aggressive push into AI-driven experiences.

At the same time, Apple is preparing for a major product evolution, a foldable iPhone that could debut soon after Tim Cook steps down, potentially reigniting excitement around its flagship lineup. Nevertheless, despite the leadership change and evolving strategy, Apple’s market dominance remains firmly intact. With a towering market cap of roughly $4 trillion, Apple continues to rank among the world’s most valuable companies, and its stock performance tells the same story.

Shares have climbed 37.8% over the past year, outpacing the broader S&P 500 Index's ($SPX) 36.95% gain. The strength extends into the near term, with AAPL up 7.48% in the last three months compared to the market’s 2.74% rise. Notably, the stock remains resilient, trading just 7.8% below its December peak of $288.62.

A Look Inside Apple’s Q1 Earnings Report

Apple kicked off fiscal 2026 with a headline-grabbing first quarter report that reinforced its status as a pillar of the tech sector. In results reported on Jan. 29, the company comfortably beat Wall Street expectations on both revenue and earnings, powered largely by the enduring strength of its iPhone franchise. Revenue jumped 15.6% year-over-year (YOY) to $143.76 billion, well ahead of the $137.81 billion consensus estimate.

Unsurprisingly, the iPhone remained the star performer. Sales surged 23.3% annually to $85.3 billion, driven by strong demand for the iPhone 17 lineup introduced in September 2025. CEO Tim Cook called it a “record-breaking quarter,” pointing to solid momentum across all regions. A standout highlight was Greater China, including Taiwan and Hong Kong, where revenue soared 38% to $25.5 billion, underscoring Apple’s deep global reach.

Outside of the iPhone, however, trends were more uneven. iPad revenue saw a modest 6.3% uptick, while Mac sales slipped 7%, reflecting softer demand in the broader PC market. Meanwhile, the Wearables, Home, and Accessories segment, spanning products like AirPods, Apple Watch, and Vision Pro, declined about 2%, hinting at some pressure on discretionary spending.

Even so, Apple’s ecosystem continues to scale impressively. Its active installed base grew to 2.5 billion devices, up from 2.35 billion a year ago, reinforcing the strength of its global footprint. At the same time, its high-margin services business, including Apple TV+, iCloud, advertising partnerships, and AppleCare, expanded 14% YOY to $30 billion, providing a steady and increasingly critical revenue stream.

On the bottom line, Apple delivered earnings per share of $2.84, up 18.3% YOY and comfortably above the $2.65 estimate. CFO Kevan Parekh also highlighted the company’s strong cash generation, with nearly $54 billion in operating cash flow, enabling Apple to return close to $32 billion to shareholders. Overall, it was a quarter that not only showcased Apple’s core strength but also highlighted the shifting dynamics across its broader business portfolio.

How Are Analysts Viewing Apple Stock?

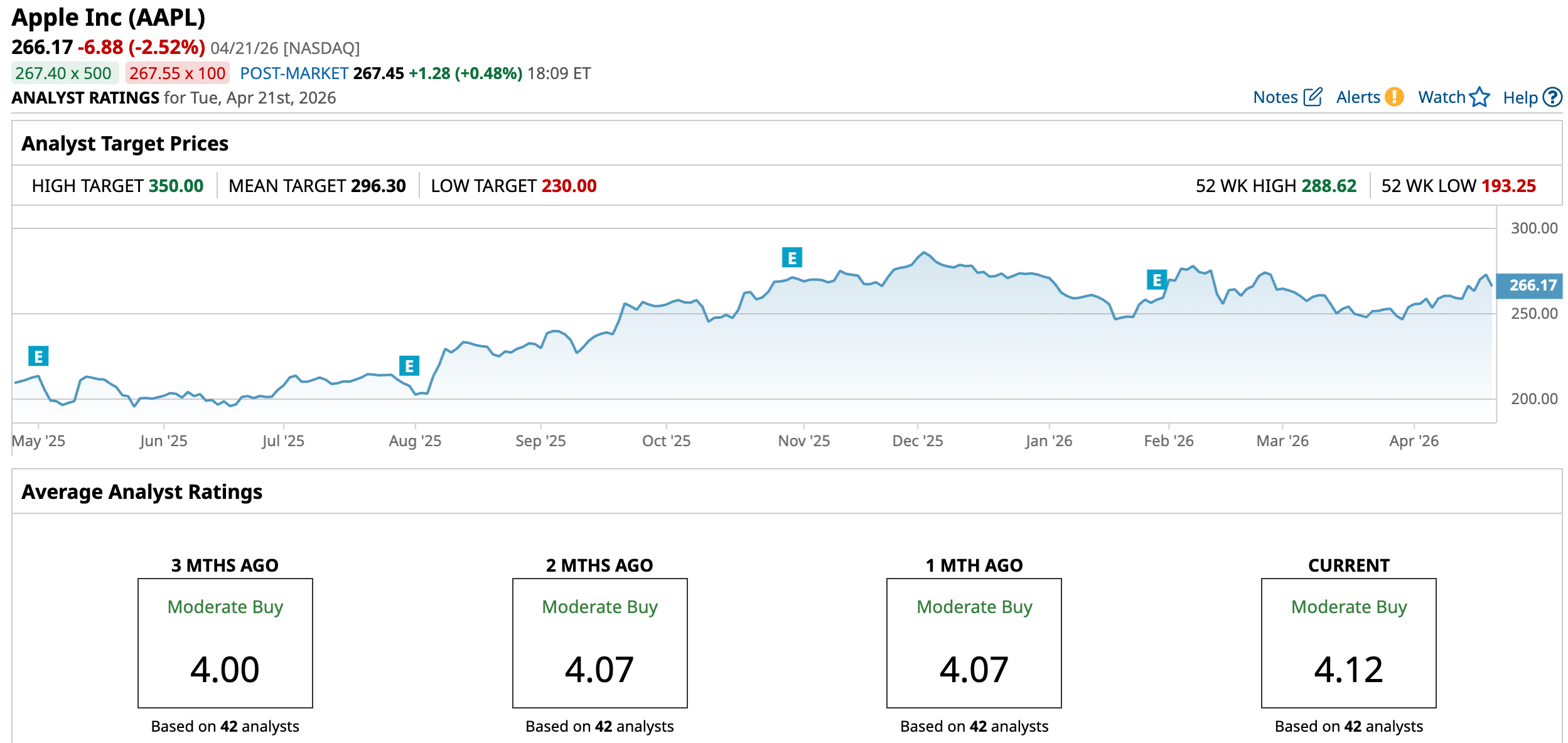

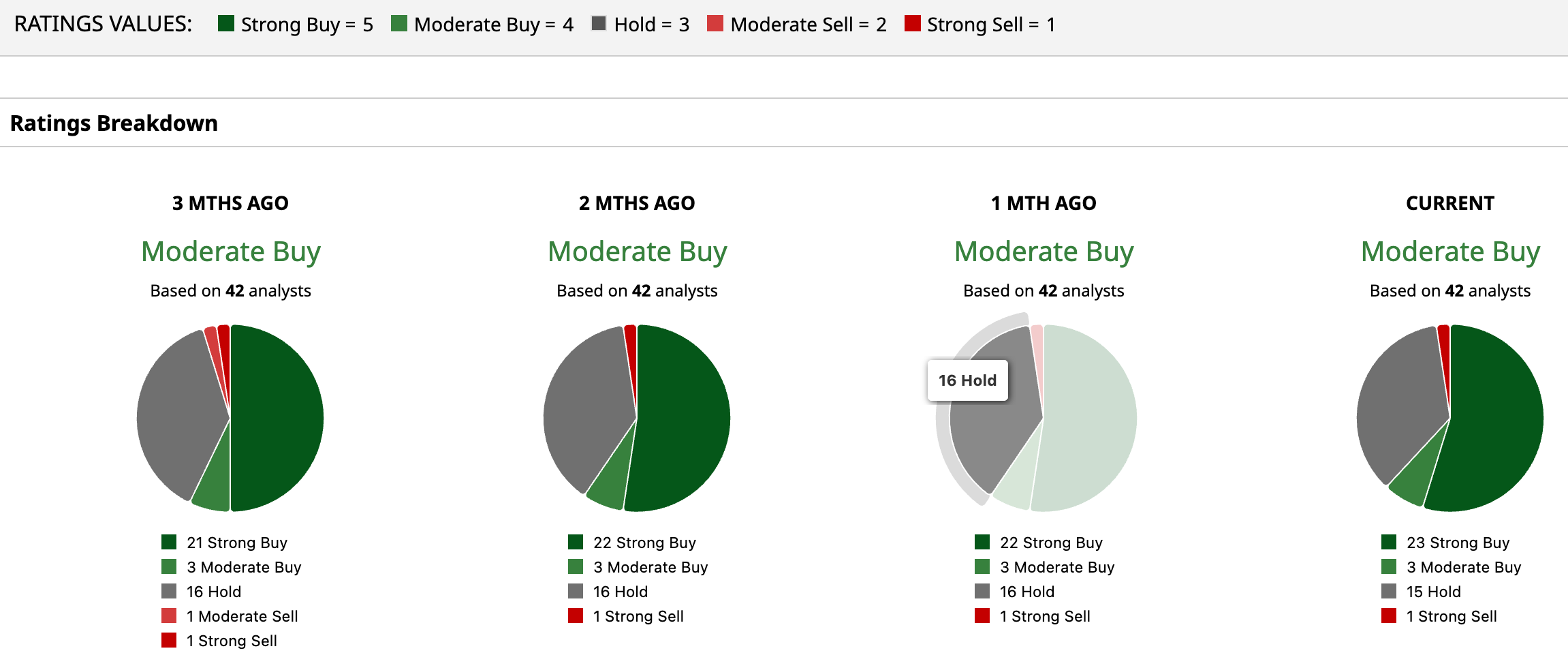

As Apple heads into its Q2 earnings, Wall Street sentiment remains notably positive. The stock holds a consensus “Moderate Buy” rating, backed by a strong majority of bullish calls, with 23 of the 42 analysts rating it a “Strong Buy,” three recommending “Moderate Buy,” 15 remaining neutral with “Hold,” and only one analyst taking a bearish “Strong Sell” stance. The upside case is still very much alive. The average price target of $296.30 signals a potential gain of 11.32%, while the Street-high target of $350 points to a possible rally of 31.5% in the coming months.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.