On February 8, the USDA released its latest WASDE report. The full text is available via this link. Prices mainly stayed the same since mid-January when I wrote about the January WASDE report on Barchart. At the end of that article, I wrote, “Given the ongoing war in Ukraine, the ever-growing demand for food, and new demand from the biofuel sector, any significant corrections in the soybean, corn, and wheat futures market could continue to be buying opportunities in 2023.” My view is the same as the price action since then, no material change.

Teucrium’s take on the February WASDE report

The Teucrium family of agricultural products, including the CORN, SOYB, and WEAT ETFs, track the futures contracts as they typically hold a portfolio of three actively traded delivery months. I reached out to Jake Hanley at Teucrium for his take on the USDA’s latest report. Jake told me:

Today's report was largely in line with trade expectations, with US corn ending stocks increased by 25 million bushels due to a decrease in ethanol demand, and US soybean ending stocks were raised 15 million bushels due to a reduction in crush expectations.

The report was a sleeper for wheat markets, however front-month wheat futures are up by over 1% for the day. This may be attributed to the ongoing war in Ukraine, and further speculation that Russia is planning a major offensive this Spring.

Still nothing in today’s reports change the fundamental fact that we in the US are expected to use more corn, wheat, and soybeans than we produced in the ’22-’23 crop year. With domestic balance sheets tightening we expect continued volatility over the next few months. Moving forward South American weather conditions should be closely monitored, particularly delays in Brazil's soybean harvest and subsequent planting delays for their 2nd crop corn. At the end of the month, the USDA's Ag Outlook Forum will provide an early outlook for the '23-'24 crop year.

While there were no significant changes in the February WASDE report, the balance sheets remain tight, putting pressure on farmers to produce a bumper 2023 crop.

Soybeans- Steady post-WASDE and before the 2023 planting season

The USDA reported lower U.S. stocks and higher global inventories but pushed the 2022/2023 price forecasts for soybeans and soybean meal higher while leaving soy oil unchanged.

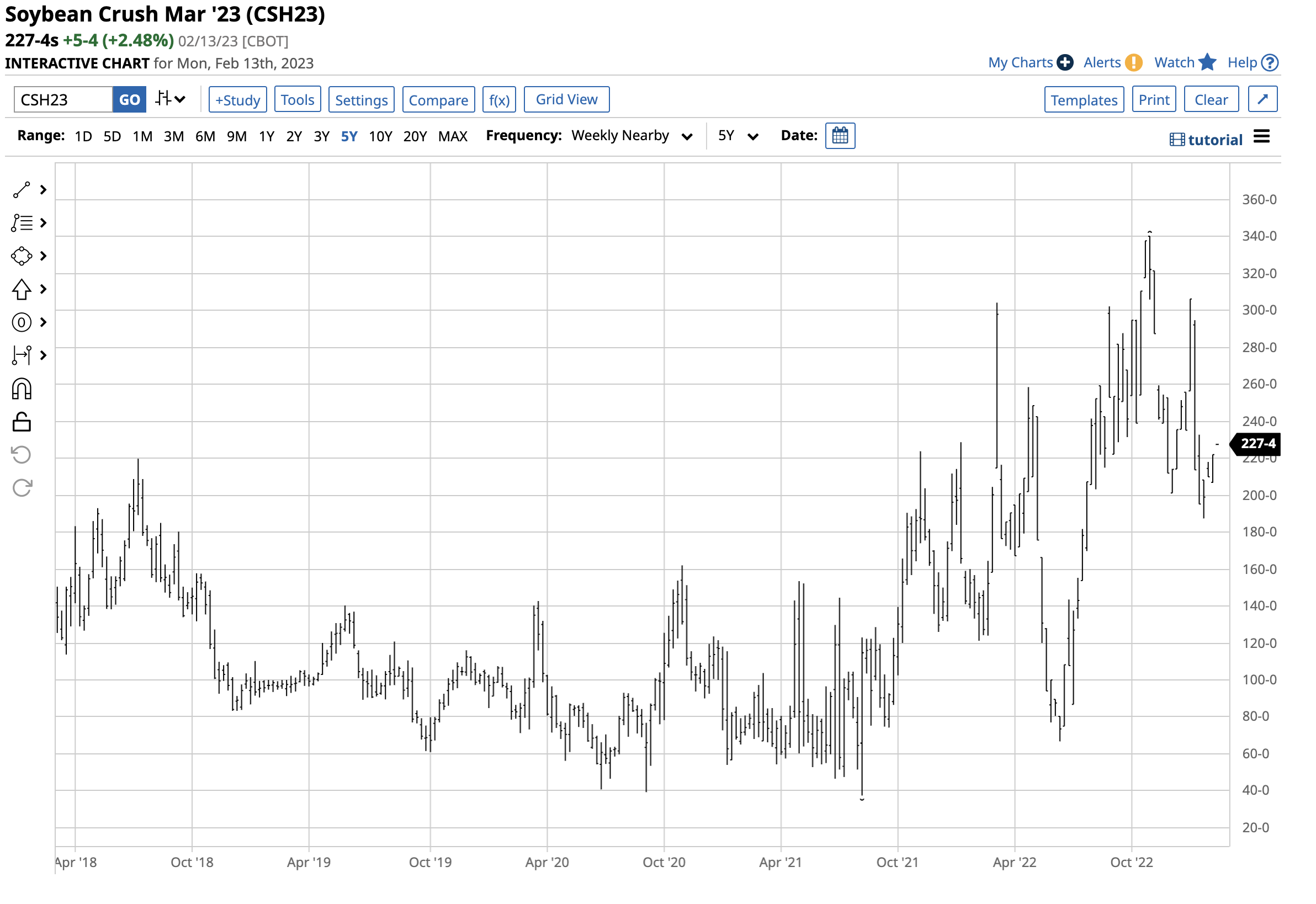

The chart highlights nearby March CBOT soybean futures have been trading around the $15 per bushel level in 2023, and the February WASDE had no dramatic impact on the price.

The March soybean crush spread, which measures the oilseed’s price against soybean meal and oil prices, remained elevated at the $2.2750 level on February 14.

Soybean futures are heading into the 2023 planting year within the 2021 range in February 2022, which was the highest February price since 2008.

Corn- Not much action post-WASDE

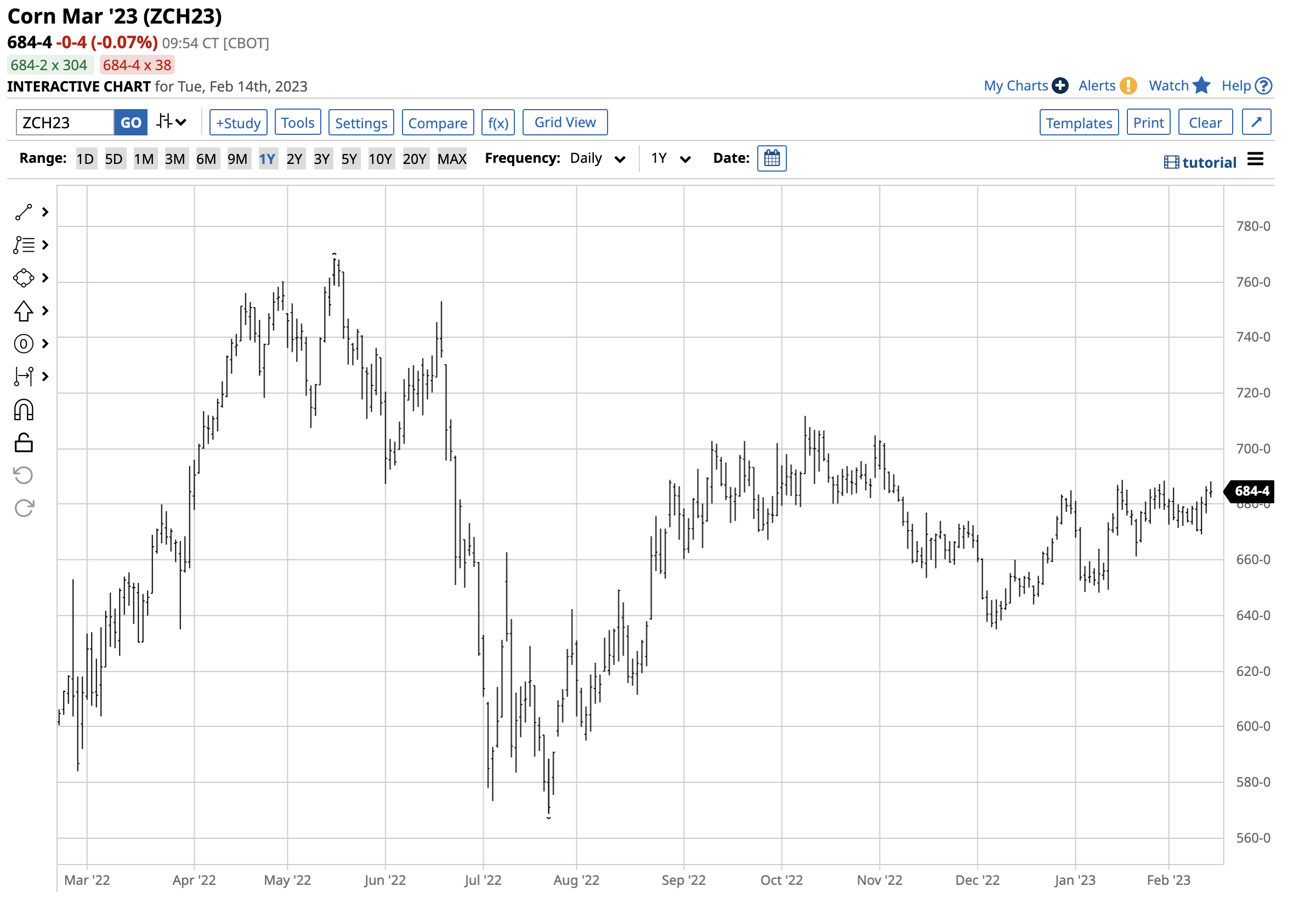

The USDA’s report told the corn market that while U.S. inventories rose, global stockpiles declined from the January report. The corn price forecast remained unchanged.

The chart of CBOT March corn futures highlights the lack of movement in corn futures after the latest WASDE report. At nearly the $6.85 per bushel level, corn futures are within the February 2022 and at the highest price in February since 2013.

In the U.S., corn is the primary ingredient in ethanol.

The chart of March Chicago ethanol swaps illustrates biofuel prices remain elevated in February 2023.

Wheat moves higher after the February report

The February 8, 2023, WASDE told the CBOT soft red winter wheat futures market U.S. stocks were mainly unchanged while global stocks increased. However, inventories remain at the lowest level since 2016/2017. The USDA slightly lowered its price forecast for 2022/2023.

The chart shows March soft red winter wheat futures moved higher in post-WASDE trading to the highest price since December 30, 2022. At over $7.95 per bushel, CBOT wheat futures were lower than in February 2022 but at the highest price in February since 2013.

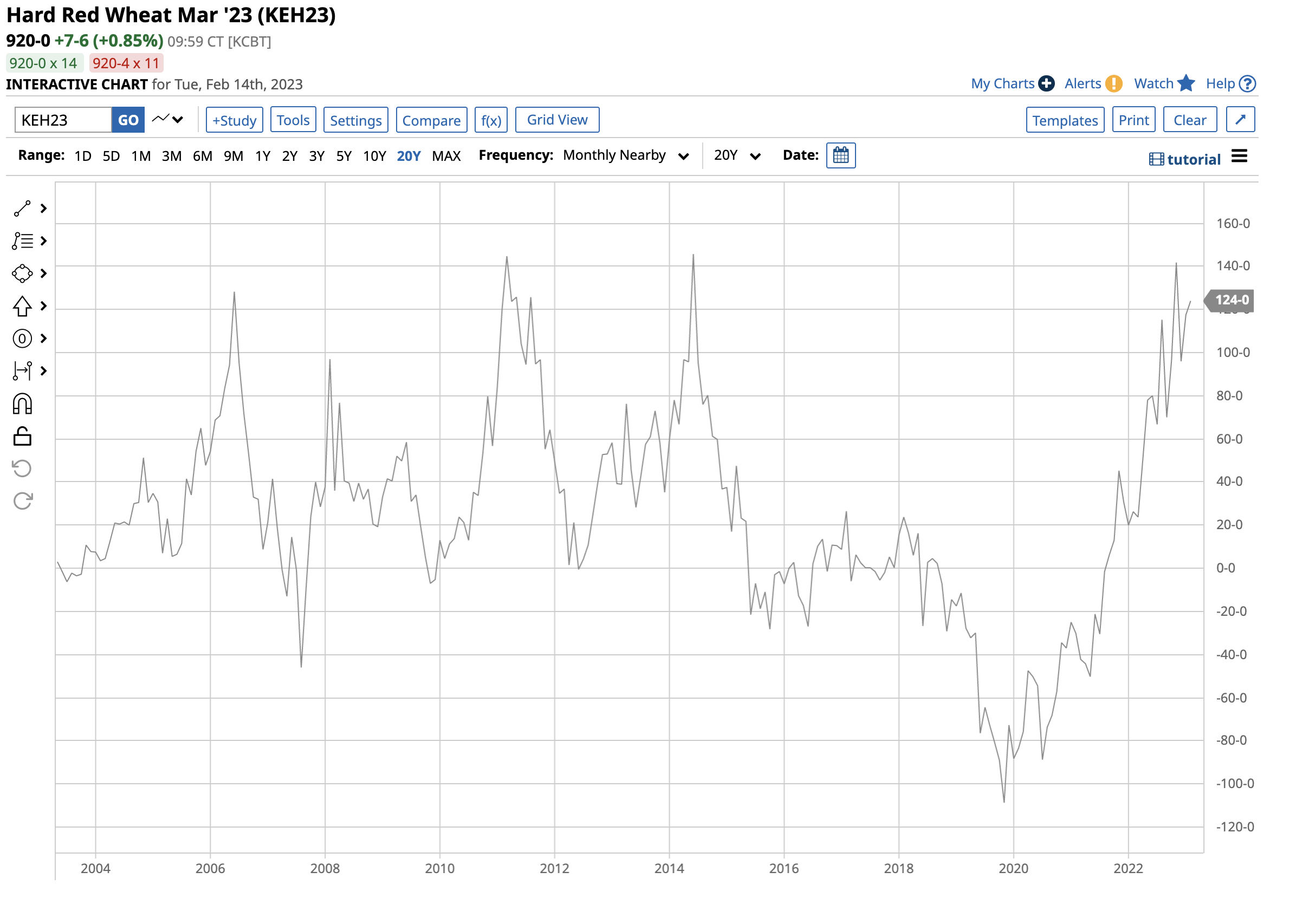

The chart of KCBT hard red winter wheat versus CBOT soft red winter wheat for March 2023 delivery ({KEH23}-{ZWH23}) shows at around a $1.24 premium for the KCBT wheat; the spread remains at the highest level in years. The high level of the spread indicates significant consumer hedging because of supply and price concerns.

Meanwhile, the total number of open long and short positions in the soybean, corn, and wheat futures markets has been rising, indicating speculative interest and increasing hedge transactions going into the 2023 crop year.

Fertilizer concerns as the rubber meet the road and farmers make final preparations for the 2023 planting season

A significant factor for the upcoming 2023 planting season is sky-high fertilizer prices and availability concerns. Inflation and fertilizer scarcity underpin prices, as does the ongoing war in Europe’s breadbasket.

Given the tight balance sheets, farmers will need to produce a bumper crop of grains and oilseeds to keep pace with the demand. While many factors underpin prices, the weather conditions across the fertile plains in the northern hemisphere will determine the path of least resistance of prices over the coming months. A drought or other widespread weather issues could cause prices to rise to all-time highs in the current environment.

More Grain News from Barchart

- Wheats Off Overnight Highs

- Soy Working Weaker into Monday

- Corn Mixed for Day Session

- Wheat Complex Posts Gains on Monday

On the date of publication, Andrew Hecht did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/CPU%20Chip.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Hands%20of%20robot%20and%20human%20touching%20on%20big%20data%20network%20connection%20by%20PopTika%20via%20Shutterstock.jpg)