/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

Qualcomm (QCOM) stock climbed 8% after investment firm GF Securities predicted that a “server CPU super cycle” is on the anvil and that the chipmaker may be one of the key beneficiaries of this trend. Analysts believe the server CPU market will grow at a five-year compound annual growth rate (CAGR) of 38% to reach $135 billion by 2030.

While also making the case for the likes of Intel (INTC) and Advanced Micro Devices (AMD), GF Securities highlighted that, in a bullish scenario, "assuming Qualcomm captures 30% of ARM-based CPU market in 2028 […] the resulting [$3.6 billion] in net profit would represent a ~30% boost to its annual non-GAAP earnings.” Here's what investors should know about QCOM stock today.

About Qualcomm Stock

Founded in 1985, Qualcomm is best known for its Snapdragon brand of processors for smartphones, which is a part of its Qualcomm CDMA Technologies (QCT) segment. Apart from processors, QCT products also include 5G modems and automotive chips, among other things. Another segment of the company's business is Qualcomm Technology Licensing (QTL), which licenses cellular patents and wireless technologies to global device manufacturers.

Valued at a market capitalization of $221.6 billion, QCOM stock is up 25% on a year-to-date (YTD) basis. Moreover, the stock offers a dividend yield of 1.5%, which is higher than the sector median. Notably, Qualcomm has been raising dividends consecutively for the past 22 years, and with a payout ratio of 36.6%, the scope for further growth remains.

What Qualcomm Offers the CPU Market

Qualcomm may be the new kid on the block in terms of the CPU market, but it has arrived with a clear plan built on the belief that the x86 CPU era is coming to an end. Now, it is ready to steer the CPU market into a fresh era.

That's where Qualcomm's Oryon CPU core comes in. Oryon is a custom ARM architecture CPU that the company inherited through its 2021 acquisition of Nuvia. The Oryon core promises improved performance, and at Computex 2025, CEO Cristiano Amon unveiled plans for data-center CPUs designed to connect with Nvidia's (NVDA) GPU infrastructure, a critical requirement for any chip hoping to be relevant in AI workloads. Further, Qualcomm's differentiation is not just about raw performance but about cost efficiency and integration with AI pipelines.

Meanwhile, as agentic AI increasingly becomes the next step in the tech revolution, Qualcomm is not standing still. In October 2025, the company unveiled two new AI inference processors for data centers, the AI200 and the AI250, with the AI200 available in 2026 and the AI250 following in 2027. Additionally, on the CPU side, Qualcomm is developing its first server-grade processor codenamed SD1, featuring 80 Oryon CPU cores, high-bandwidth memory support, PCIe 5.0, and compatibility with Nvidia's NVLink Fusion for tight integration in AI server environments.

Beyond chips, the company is building a full hyperscaler-grade software platform optimized for large-scale inference. Finally, the company's acquisition of Alphawave Semi for $2.4 billion in December 2025 strengthened its position in high-speed chip-to-chip connectivity, chiplets, and custom silicon for cloud customers. Qualcomm sees this deal as a multi-year structural bet rather than a quick opportunistic move.

However, what should worry investors amid all these developments is that Qualcomm has been here before. The company had entered the server CPU market years earlier but quit in 2018, only to reenter the space with the acquisition of Nuvia. Moreover, the x86 software ecosystem will be hard to dismantle, because for many IT decision makers, the incumbent solutions do not need to be better than Qualcomm's offering — they just need to be good enough. Finally, hyperscalers building their own custom ARM-based chips may act as a strong deterrent in terms of market penetration for Qualcomm as well.

Earnings and Revenue Fell Slightly

Qualcomm's second-quarter earnings report was marked by a slight decline in revenue and earnings. However, the report hinted that the constrained supply of memory chips carried the blame.

The company saw revenue of $10.6 billion in Q2, down 3% from almost $11 billion in the previous year. While the QCT segment saw a yearly decline of 4% in revenue to $9.1 billion, the QTL segment saw an uptick of 5% year-over-year (YOY) to $1.4 billion.

Earnings fell by 7% on a YOY basis to $2.65 per share. Yet, EPS managed to exceed the Street's estimate of $2.56 per share. Notably, this marked another consecutive quarter of an earnings beat from the company.

Guidance was in line with consensus estimates, too. For Q3 2026, revenue and EPS are forecast to range between $9.2 billion and $10 billion and $2.10 and $2.30, respectively. The midpoints of both these ranges are comparable to analysts' revenue and earnings estimates.

Meanwhile, for the first six months of fiscal 2026, Qualcomm reported net cash from operating activities of $7.4 billion, up from $7.1 billion in the year-ago period. Overall, the company exited March 2026 with a cash balance of $5.44 billion, which is much higher than its short-term debt levels of $498 million.

Unlike some peers in the chip market, QCOM stock is also trading at relatively reasonable levels even after its sharp rally. Qualcomm has a forward price-to-earnings (P/E) ratio of 29.7 times and a price-to-cash flow ratio of 20.7 times, while its forward price-to-sales (P/S) ratio is 5.6 times.

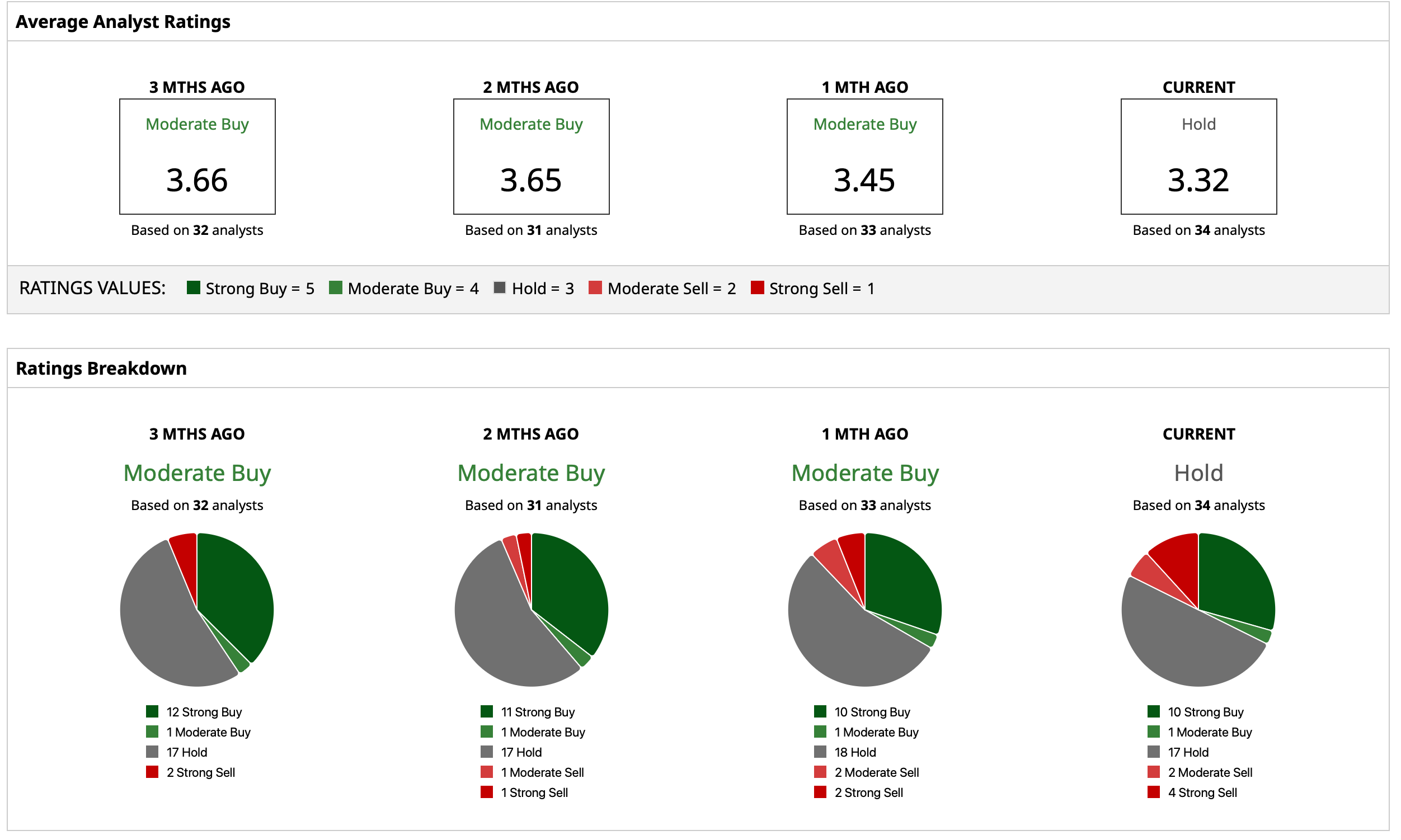

What Do Analysts Think of QCOM Stock?

Overall, analysts have a consensus “Hold” rating for QCOM stock. The mean target price of $180 has already been surpassed by shares. However, the high target of $300 denotes potential upside of about 41% from current levels. Out of 35 analysts covering the stock, 10 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 18 have a “Hold” rating, two have a “Moderate Sell,” and three analysts have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)