The ongoing wave of geopolitical tensions in the Middle East brought on by the U.S.-Iran war has done more than just rattle headlines. It has pushed energy markets higher, lifting oil and gasoline prices while adding fresh momentum to select pockets of the stock market. Even as hopes for a ceasefire emerge, economists caution that relief may not come quickly.

As seen in past cycles, fuel prices tend to spike fast and ease slowly, with supply chains taking months to fully stabilize. This lingering pressure is already showing up in inflation data, with the latest Consumer Price Index highlighting how sharply gasoline costs have weighed on household budgets.

That strain is beginning to reshape consumer behavior. With a larger share of income now going toward fuel, lower-income households are pulling back on discretionary spending, while higher-income groups remain relatively resilient. Neuberger Berman’s analyst John San Marco notes that rising gas prices have effectively offset tax benefits for a majority of consumers, but wealthier cohorts continue to hold up better, creating a widening gap in spending patterns.

In this environment, analysts are leaning toward consumer names that cater to more stable, higher-income demand. Companies like Home Depot (HD) and Costco Wholesale Corporation (COST) have emerged on the firm’s shortlist, seen as better positioned to navigate the pressure.

In a market shaped by uneven spending, these dividend-paying consumer stocks may be compelling buys now.

Consumer Stock #1: Home Depot

Founded in 1978 and headquartered in Atlanta, Georgia, Home Depot is one of the world’s largest home improvement retailers with over 2,300 stores in the U.S., Canada, and Mexico. The company offers a wide range of building materials, décor, lawn and garden products, along with maintenance and repair solutions. Also, it provides installation services for items like flooring, cabinets, and HVAC systems, alongside tool and equipment rentals. Home Depot serves DIY customers, professional contractors, and builders alike.

Its reach spans physical stores and a strong digital ecosystem, including multiple websites and mobile apps, making it a one-stop shop for home improvement needs. Its market capitalization currently stands at $341.4 billion.

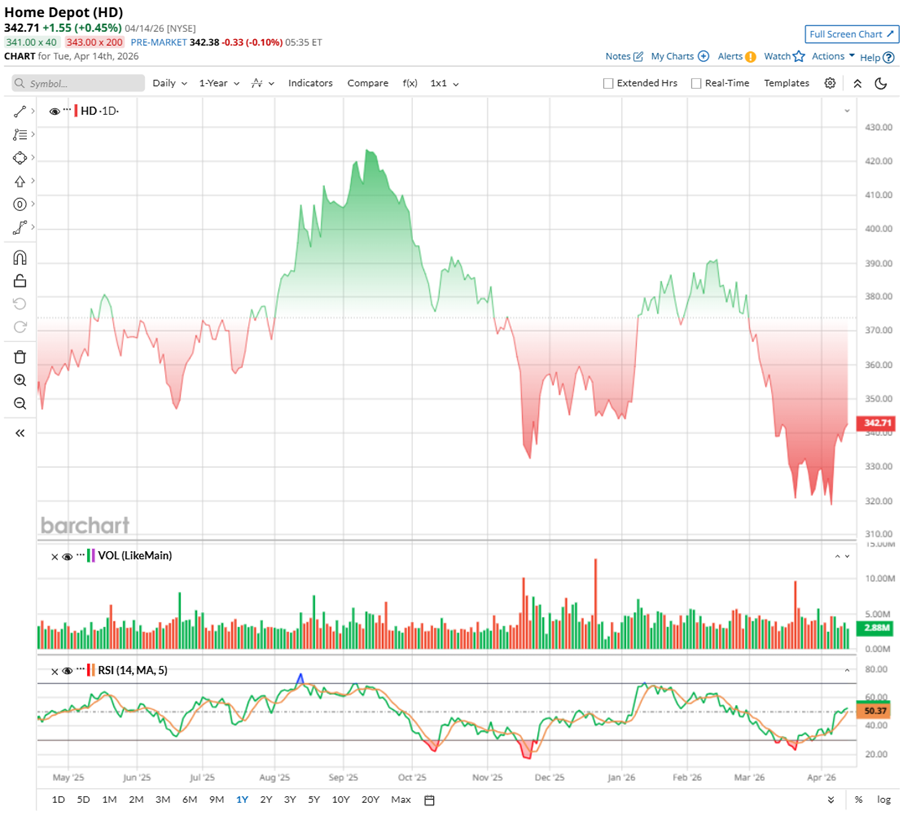

Despite its strength, shares of the home improvement retail giant have seen a mixed run lately, reflecting both pressure and recovery. Over the past 52 weeks, HD stock slipped about 4.52%, and in 2026 so far, the stock is marginally down by 1.74%. The weakness was more visible in the recent quarter, with the stock falling 8.8% over the past three months and touching a low of $315.31 in April.

However, the shorter-term trend is starting to look steady. Over the past month, the stock has been down only marginally, and in just the last five days, it has jumped 0.58%. Volume trends are also turning positive, with more green bars indicating stronger accumulation by investors.

From a technical standpoint, the 14-day RSI, which had dropped into the oversold zone in mid-March, has now rebounded to 49.27. This suggests the stock is stabilizing, with momentum gradually shifting back in favor of buyers.

HD stock has a balanced valuation story. It trades at 22.70 times forward adjusted earnings, above its sector and historical averages, showing investors are still willing to pay for its stability. But on the flip side, its price-to-sales ratio of 1.99 times sits below historical levels, hinting that the premium is not stretched and leaves some room for upside.

Home Depot adds another layer to its story through steady shareholder returns. The company has paid dividends for 38 consecutive years, with 16 straight years of growth, showing a clear commitment to consistency. Backed by strong cash flows, it comfortably funds dividends.

Currently, Home Depot offers a forward annual dividend of $9.32 per share, translating to a forward yield of around 2.72%, well above the State Street SPDR S&P 500 ETF Trust’s (SPY) 1.06% yield. With a payout ratio of 62.8%, it strikes a balance, returning a solid portion of earnings while still keeping room to reinvest and grow.

Home Depot is moving through a softer patch, but the story is not without balance. On Feb. 24, the company reported its fourth-quarter fiscal 2025 results, with sales coming in at $38.2 billion, down 3.8% year-over-year (YOY). Net earnings stood at $2.6 billion, down 14.2%, reflecting both a challenging demand backdrop and the impact of one fewer operating week compared to last year. Adjusted EPS came in at $2.72, lower than $3.13 a year ago. It’s worth noting that fiscal 2024 had an extra 14th week, slightly skewing the comparison. Even then, both revenue and adjusted EPS managed to beat the Street’s expectations.

The pressure largely came from external factors. A lack of storm-related demand hurt key categories, while the broader housing market remained a drag. High mortgage rates and elevated home prices have made housing less affordable, slowing home sales and, in turn, reducing demand for renovation projects. With fewer people moving homes, big-ticket improvement spending has naturally cooled.

Meanwhile, consumers are staying cautious. Concerns around inflation, job stability, and higher borrowing costs are making households think twice before taking on large discretionary projects – areas that typically drive higher-value sales for Home Depot.

Financially, the company remains stable. It ended fiscal 2025 with $1.4 billion in cash and cash equivalents, with net cash provided by operating activities amounting to $16.3 billion. Plus, long-term debt came in at $46.3 billion.

Looking ahead, management expects a gradual recovery. For fiscal 2026, Home Depot is guiding for total sales growth of 2.5% to 4.5%, with comparable sales expected to range from flat to up 2%. The company also plans to open around 15 new stores, with adjusted EPS projected to grow between flat and 4% from $14.69 in fiscal 2025.

Meanwhile, expectations on the Street remain steady for Home Depot. Analysts see fiscal 2026 adjusted EPS amounting to $15.03, reflecting a modest 2.3% YOY increase. Looking ahead, the tone turns more optimistic, with fiscal 2027 adjusted EPS projected to climb 8.8% annually to $16.35, signaling a gradual pickup in growth.

With fuel prices expected to remain elevated, spending may shift rather than disappear, and Home Depot could still find support. While higher costs may pressure budgets and slow large DIY and renovation projects, the picture isn’t entirely negative. As people delay moving, they tend to focus more on essential repairs and maintenance, keeping a steady base of demand intact. At the same time, Home Depot’s exposure to higher-income customers and professional contractors adds a layer of resilience in a tighter spending environment.

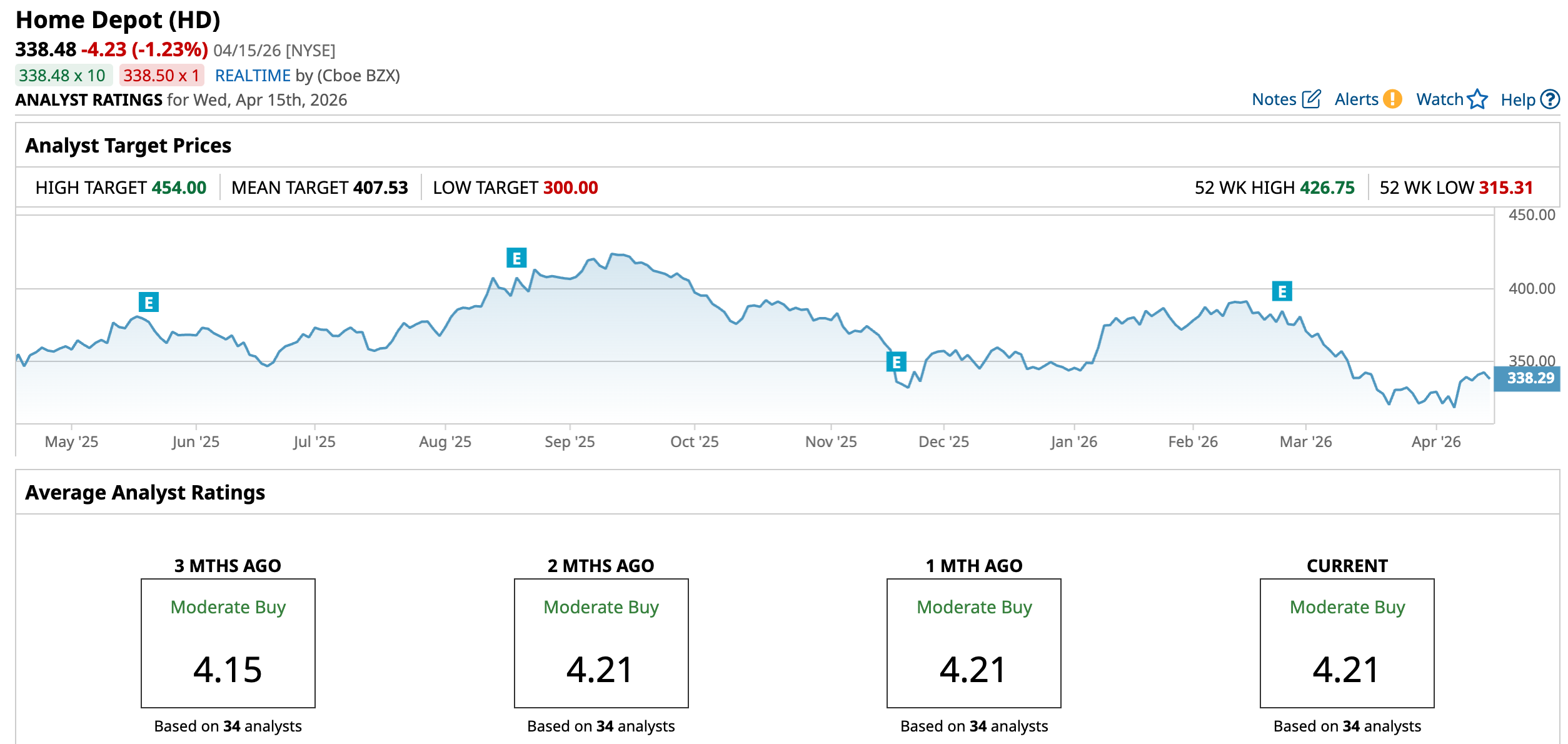

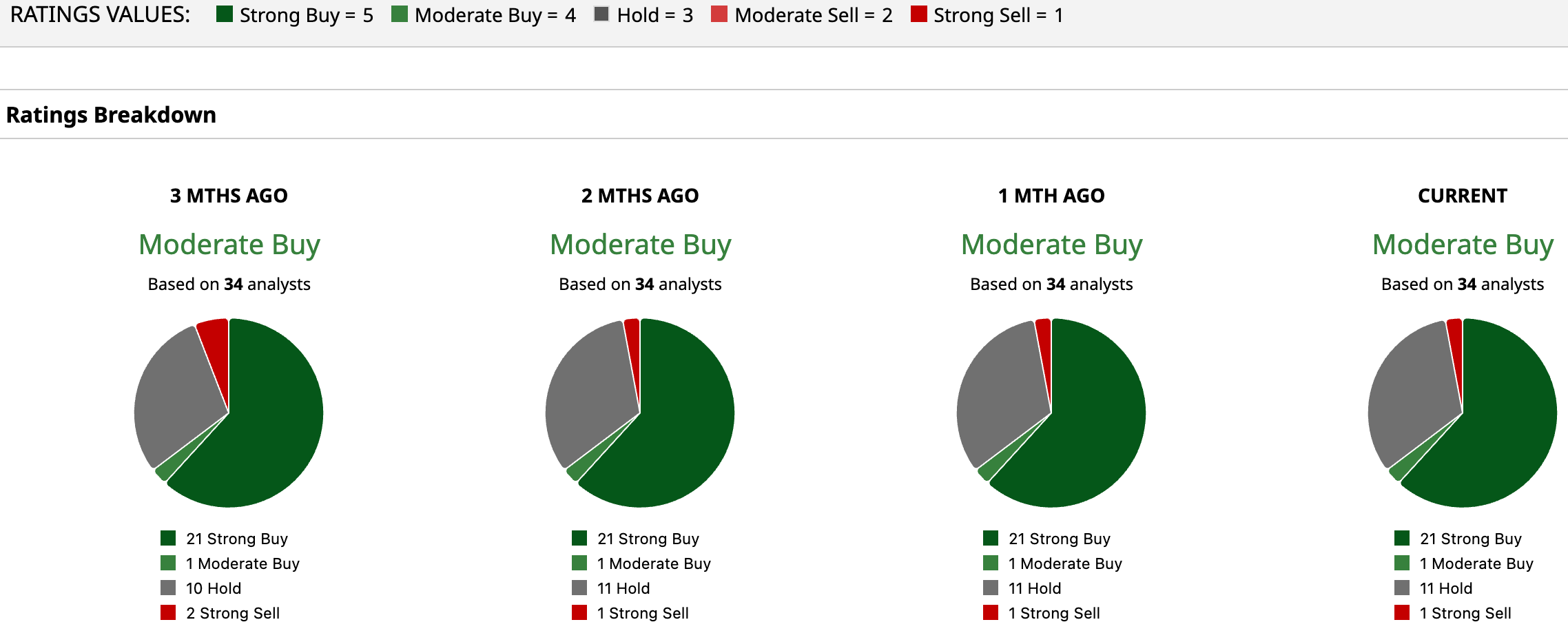

Overall, analysts are upbeat on HD, with a “Moderate Buy” consensus. Of the 34 analysts tracking the stock, 21 have a “Strong Buy,” one advises a “Moderate Buy,” 11 are on the sidelines with a “Hold,” and the remaining one analyst has a “Strong Sell” rating.

HD stock has an average price target of $407.53, implying roughly 20.4% upside potential from current levels. On the bullish end, the Street-high target of $454 points to even sharper gains of 34.13%. Together, these point to a setup where Home Depot could reward patient investors, with upside building as demand stabilizes and market sentiment improves.

Consumer Stock #2: Costco Wholesale

Costco, founded in 1976 and headquartered in Issaquah, Washington, is a global membership-only warehouse retailer and the world’s third-largest retailer, with a market cap of about $432.5 billion. It offers groceries, fresh produce, appliances, and essentials at low prices, alongside fuel stations, pharmacies, optical, and travel services.

Its model is driven by membership fees, allowing lower reliance on product margins. Costco caps markups at roughly 14% for national brands and 15% for its private label, Kirkland Signature – far below typical retailers – supporting high-volume sales, strong customer loyalty, and consistent long-term growth.

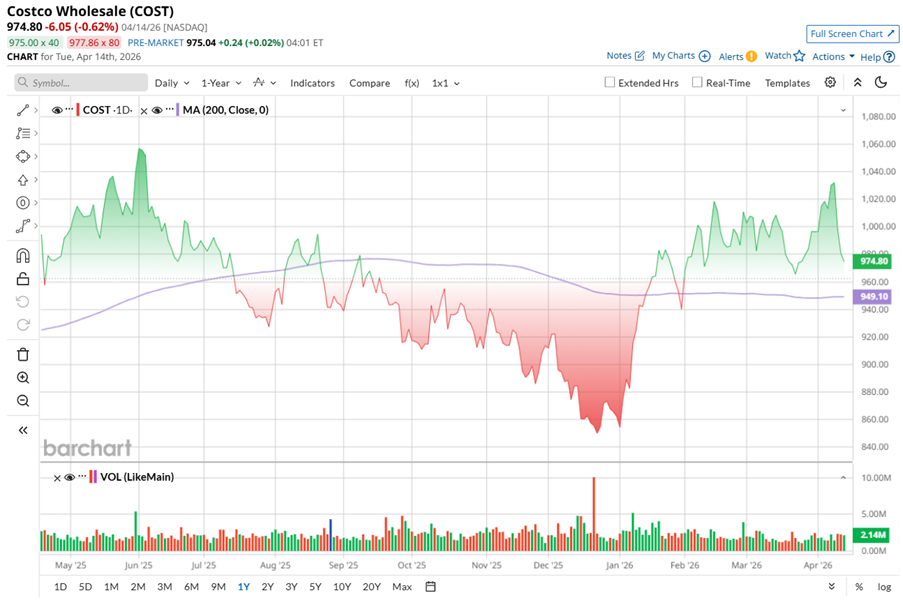

Shares of the membership warehouse operator have been showing a steady comeback, climbing 14.14% year-to-date (YTD). Last year, concerns around slowing comparable-store sales kept the stock under pressure, but things have started to turn. Recent monthly sales improvements have reassured investors, bringing confidence back into the story.

Technically, the stock is now trading above its 200-day moving average, which often signals a stronger, more stable trend. Volume trends are also encouraging, with more green bars indicating consistent buying interest.

Valuation-wise, COST stock is priced at 48.27 times forward adjusted earnings and 1.45 times sales, both above sector peers and its own five-year averages. But investors seem fine paying up, because Costco keeps delivering and backing that premium with consistent execution.

Then there’s the dividend piece, which plays a quieter but steady role. Costco has lifted its payouts for 21 consecutive years and currently offers $5.20 per share annually, translating to a modest 0.51% yield. Plus, a payout ratio of just 27%, leaves ample room for future increases without stretching its finances.

Costco shows why it stands out, even in a tricky consumer environment. On March 5, the company reported its fiscal second-quarter 2026 results, generating revenue of $69.6 billion, up 9.2% YOY, comfortably beating Street’s expectations, while EPS climbed 13.9% annually to $4.58, again ahead of estimates.

What adds more confidence is the balance sheet strength. Cash and cash equivalents stood at $17.4 billion as of Feb. 15, up from $14.2 billion as of Aug. 31, 2025. Membership, the core engine of Costco’s model, remained solid. Paid executive memberships grew 9.5% to 40.4 million, total paid members increased 4.8% to 82.1 million, and overall cardholders rose 4.7% to 147.2 million.

Additionally, the company stayed active on investments, with Q2 CapEx at $1.29 billion. Looking ahead, Costco plans to spend around $6.5 billion in fiscal 2026, focusing on expanding warehouses, upgrading key locations, and improving its supply and digital network. It aims to open 28 net new warehouses this year and maintain a pace of over 30 annually going forward, while also testing faster checkout systems with transaction times of about eight seconds.

The momentum carried into March as well. For the five weeks ended April 5, net sales came in at $28.41 billion, up 11.3% YOY. For the first 31 weeks, sales reached $173.26 billion, growing 9.1% annually. Even with one less shopping day due to the Easter shift, which impacted sales by around 1.5%, Costco’s growth trend remained intact, reflecting steady demand and rising store traffic.

Wall Street monitoring Costco anticipates its Q3 fiscal 2026 revenue to be $68.8 billion, while EPS is expected to rise 14.5% YOY to $4.90. For fiscal 2026, the bottom line is expected to grow nearly 13% annually to $20.32 per share, and then rise by another 9.9% to $22.33 per share in fiscal year 2027.

Costco is making an impressive move, expanding with standalone gas stations, and it fits perfectly into the current environment. With oil prices staying high due to ongoing geopolitical tensions, fuel has once again become a key pressure point for consumers. And that’s exactly where Costco has an edge. The company has always offered gas at lower prices, and now it is leaning deeper into that strength. As drivers look for ways to save, more of them are heading to Costco just to fill up.

But it might not stop there. Once customers are on-site, many walk into the warehouse and pick up everyday essentials, naturally lifting overall sales. That’s the real play. Gas may be a low-margin business, but for Costco, it acts as a magnet, bringing in traffic and reinforcing the value of its membership model. In a time when fuel costs are likely to remain elevated, this strategy quietly puts Costco in a strong position, turning cost pressure into a steady flow of customers and spending.

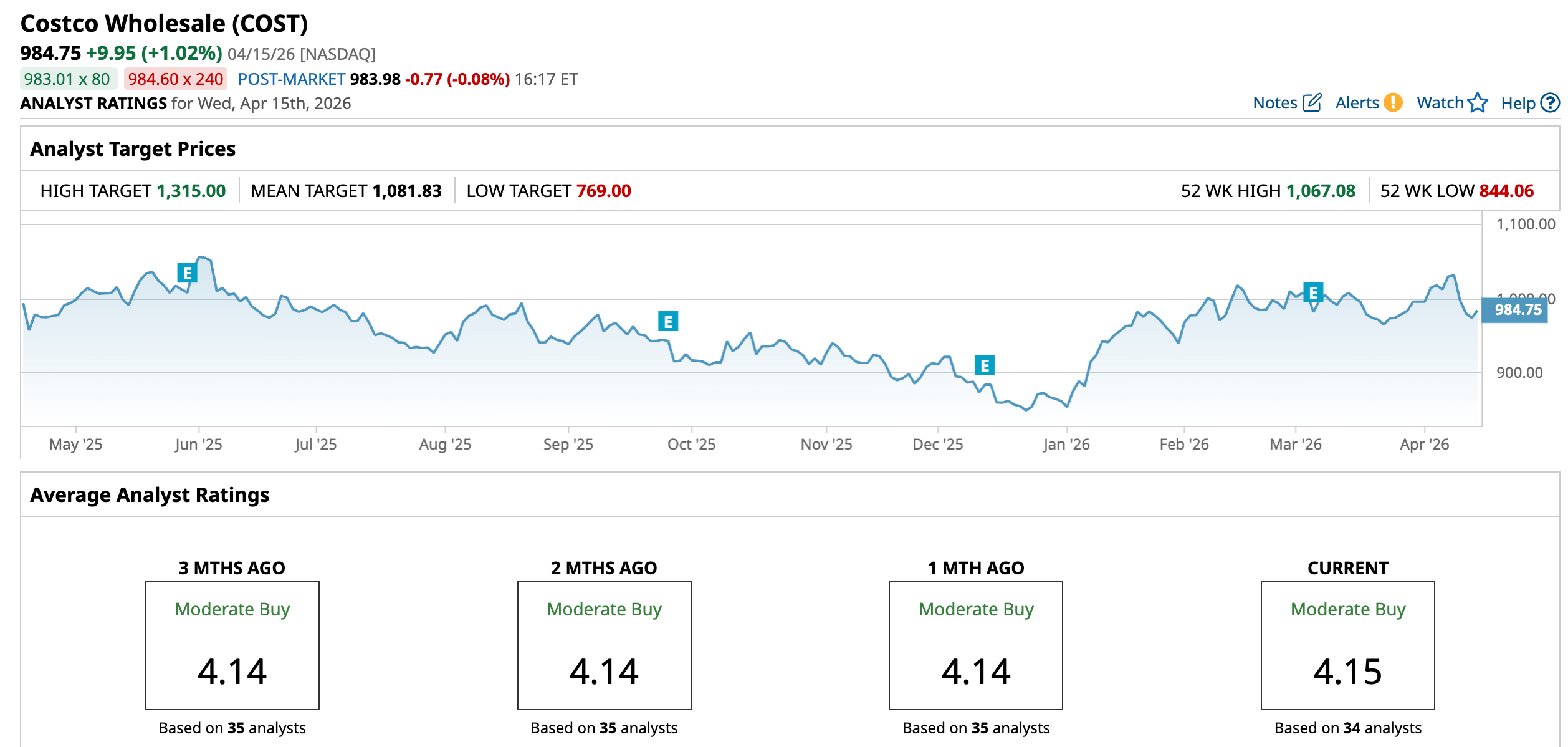

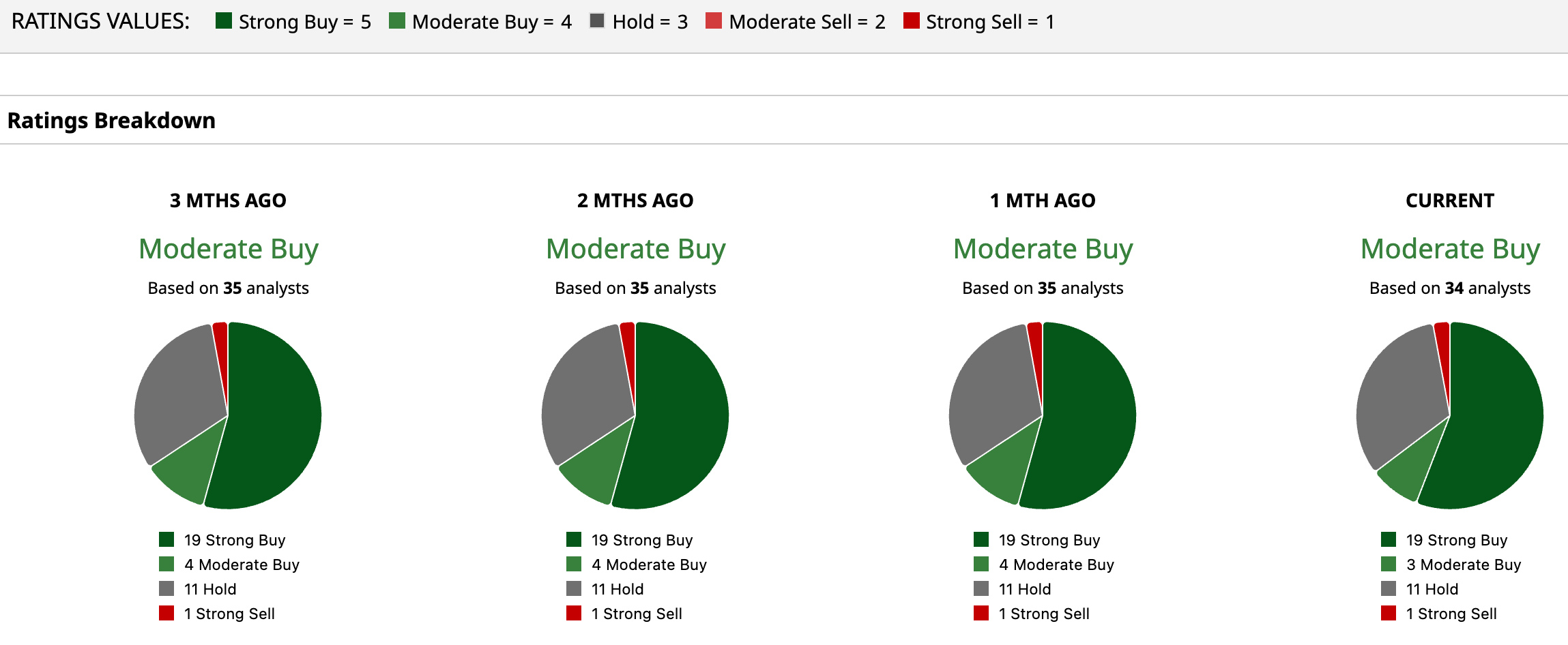

Overall, Costco has an overall rating of “Moderate Buy.” Of the 34 analysts covering the stock, 19 suggest a “Strong Buy,” three advise a “Moderate Buy,” 11 recommend a “Hold,” and one is skeptical, having a “Strong Sell” rating.

COST stock still has room to run, at least if analysts are right. The mean price target of $1,081.83 points to a decent 10% upside potential. Meanwhile, BMO Capital’s Street-high target of $1,315 suggests the stock could rise by as much as 33.54% from current levels.

That kind of optimism reflects confidence that Costco can keep growth steady, protect its margins, and keep milking its membership model as pricing trends start tilting in its favor.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)