/Chipotle%20Mexican%20Grill%20logo%20on%20building%20by-%20John%20Hanson%20Pye%20via%20Shutterstock.jpg)

With a market cap of $43.6 billion, Chipotle Mexican Grill, Inc. (CMG) is a restaurant company that owns and operates Chipotle Mexican Grill locations, offering Mexican-inspired foods like burritos, tacos, and bowls made with responsibly sourced ingredients. It also provides digital ordering through its website, mobile app, and delivery platforms, with operations across the United States and several international markets.

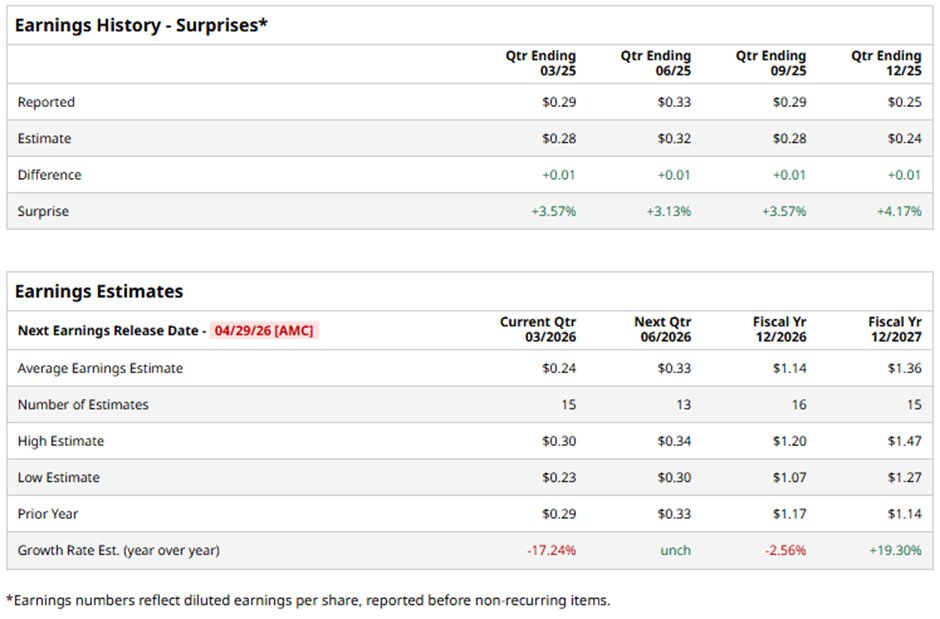

The Newport Beach, California-based company is set to announce its fiscal Q1 2026 results after the market closes on Wednesday, Apr. 29. Analysts predict CMG to report an EPS of $0.24, a 17.2% decrease from $0.29 in the year-ago quarter. However, it has surpassed Wall Street's earnings estimates in the past four quarters.

For fiscal 2026, analysts forecast Chipotle Mexican Grill to report an EPS of $1.14, a dip of 2.6% from $1.17 in fiscal 2025. Nevertheless, EPS is anticipated to increase 19.3% year-over-year to $1.36 in fiscal 2027.

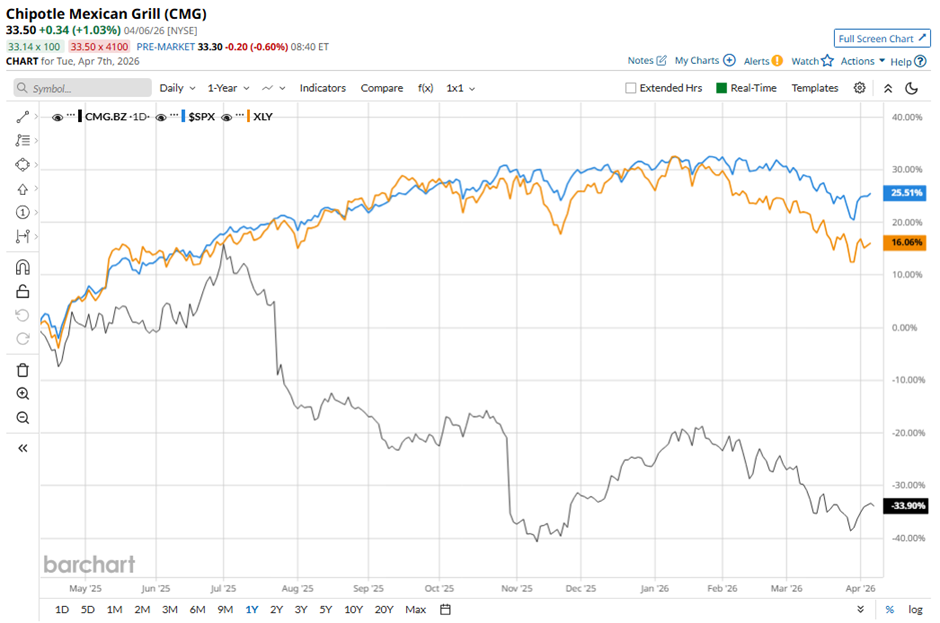

Shares of Chipotle Mexican Grill have declined 28.8% over the past 52 weeks, lagging behind the S&P 500 Index's ($SPX) 30.3% gain and the State Street Consumer Discretionary Select Sector SPDR ETF's (XLY) 19.7% rise over the period.

Shares of Chipotle Mexican Grill rose 1.9% following its Q4 2025 results on Feb. 3 as total revenue grew 4.9% year-over-year to $3 billion and full-year revenue increased 5.4% to $11.9 billion. Investors were also encouraged by earnings resilience, with Q4 EPS rising to $0.25 (up 4.2%) and full-year EPS reaching $1.14, alongside strong unit growth including 132 new restaurants in Q4 and 334 openings in 2025.

Additionally, confidence was supported by the launch of its “Recipe for Growth” strategy and an ambitious 2026 outlook calling for 350 - 370 new restaurant openings.

Analysts' consensus view on CMG stock is cautiously optimistic, with a "Moderate Buy" rating overall. Among 37 analysts covering the stock, 24 recommend "Strong Buy," three give "Moderate Buy," nine indicate “Hold,” and one has a "Strong Sell." The average analyst price target is $44.82, suggesting a potential upside of 33.8% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.