/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20in%20modern%20server%20room%20data%20center%20by%20Sashkin%20via%20Shutterstock.jpg)

The top-performing stocks in the S&P 500 ($SPX) over the last two years tell an obvious story. Markets have been dominated by AI stocks, but the nature of the companies doing the heavy lifting hasn’t been the same.

First, it was AI enablers like Nvidia (NVDA), Broadcom (AVGO), and Palantir (PLTR) that drove market returns. By 2025, it was another step in the value chain, one dominated by storage and memory players, that generated the most returns. In 2025, for instance, Sandisk (SNDK) was the top-performing S&P stock. The shares returned 559% to investors, closely followed by other storage and memory stocks like Western Digital (WDC) with 282% returns, Micron (MU) with 239% returns, and Seagate Technology (STX) with 219% returns.

2026 hasn’t been any different so far. SNDK’s 193% year-to-date (YTD) returns make it the top performer for Q1 2026. At this rate, the stock can easily match 2025 returns. But that thought process could land investors in trouble if they’re not careful. Sandisk’s outperformance isn’t a new trade idea. It is the extension of the same play from last year. We do not know when the music stops and traders move to the next set of stocks in the AI value chain. Past performance isn’t a guarantee of future performance. As long as investors know and appreciate this risk, taking a calculated bet at this point might still be worth it.

About Sandisk Stock

Sandisk is a data storage company that sells solid-state storage solutions and flash memory. Once it became clear that compute wasn’t the bottleneck in AI workloads and that progress was limited by the amount of data that could be processed, memory companies like Sandisk came to the forefront. The firm has achieved impressive results in delivering what its clients have expected over the last year and is likely to continue doing so under the leadership of CEO David Goeckeler.

SNDK stock had a perfect run in 2025, and all that seemed to continue until the beginning of February, when the stock was trading exactly where it trades now. AI has developed at a rapid pace, and it is only now that we have started seeing complete industries being potentially decimated due to AI technologies. The stock calmed down due to similar fears and nearly had a heartbreaking crash on the news of Google’s (GOOG) (GOOGL) TurboQuant algorithm.

Now that the stock has risen past the TurboQuant-induced fears, it is time to evaluate whether it can continue its run or face possible further headwinds. We know that Sandisk isn’t entirely being valued on its future earnings potential or cash flows. The company is the beneficiary of a supply crunch, and whether that supply constraint continues or not is what investors should focus on, rather than the stock’s valuation ratios.

Historically, memory shortages have been cyclical. This shortage is different. First, the shortage is so bad that companies have stopped servicing low-margin segments like PCs and similar consumer markets and reallocated resources to AI demand. The AI demand itself is so high that a supply that can only grow at 15% to 17% YoY is required to grow at a significantly higher rate. Moreover, this demand isn’t price-sensitive. Hyperscalers are willing to pay any price to get their hands on memory so that their AI develops faster than the rest of the pack. Major industry players will need two to three years of capex to bring enough capacity online to service this demand, and they’re reluctant to do that because of the past boom and bust cycles.

In short, Sandisk is a stock that can be bought not because it is cheap but because it happens to be the stock in the right place at the right time. You’re betting on the AI infrastructure investments to continue, and as long as they do, Sandisk is in the driver's seat to provide memory and storage solutions.

Management Optimistic About Future Memory Demand

On the company’s earnings call on Jan. 30, investors were looking forward to comments on memory supply and demand. Management pointed out that the ongoing supply constraints not only demand careful allocation planning but also close alignment with customer needs.

Bernstein analyst Mark Newman asked about the company’s long-term agreements, and CEO David Goeckeler replied that the company had consistently received messages from multiple customers to prioritize or guarantee supply. The firm is investing billions of dollars in capex, as per Goeckeler, and this should drive sustainable mid-teens to high-teens growth going forward. Sandisk’s commercial relationships with customers are evolving, and multiyear agreements will help secure pricing certainty and supply, leading to sustained long-term earnings. The upcoming earnings report on April 30 will provide more insights into the current status of the industry.

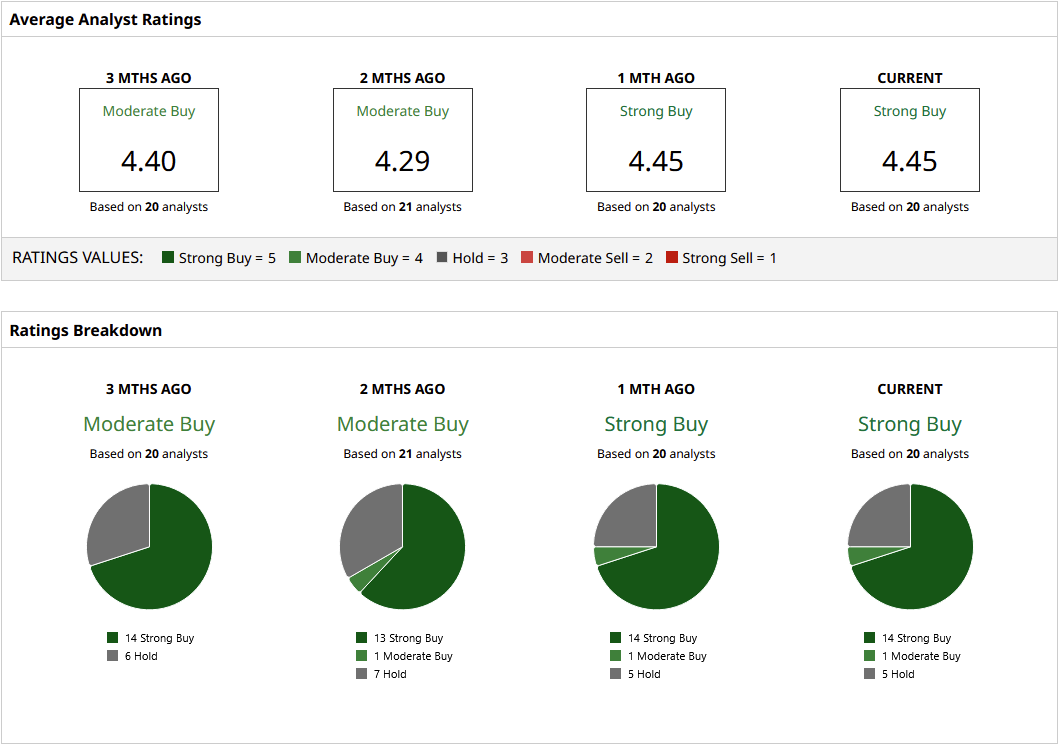

What Are Analysts Saying About SNDK Stock?

Sandisk has received a lot of analyst interest in the last few days. On March 31, Bernstein analyst Mark Newman assigned a target price of $1000 to Sandisk shares. This is currently the highest price target on Wall Street. Two more analysts expressed similar bullish sentiment before him. On March 27, Citi assigned a price target of $875, while Bank of America Securities assigned a price target of $900 to SNDK.

Twenty analysts currently cover SNDK stock on Wall Street. Fourteen of them rate the stock a “Strong Buy.” It is worth noting that there is not a single analyst with a “Sell” or “Strong Sell” rating. The mean target price of the shares is $752.24. This suggests analysts, on average, believe the stock could go up by 9%. However, if Bernstein’s price target of $1000 were to materialize, it would result in a 44% gain for investors.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)