/Quantum%20Computing/Image%20by%20Funtap%20via%20Shutterstock.jpg)

The quantum computing market has steadily gained traction over the past few years as businesses and governments race to develop next-generation computing power for artificial intelligence, cybersecurity, and complex data analysis. That momentum has also pushed several quantum-focused stocks into the spotlight, including Quantum Computing (QUBT).

The company recently grabbed Wall Street’s attention after reporting first-quarter revenue growth of over 9,000%, fueled by acquisitions and expanding demand for its photonics and quantum communication technologies. The stellar growth helped reignite momentum in QUBT stock – up 15.7% in a single trading session – which has already seen wild swings over the past few years.

Still, analysts remain cautious despite the rapid top-line growth. Wedbush Securities recently initiated coverage with a “Neutral” rating, arguing that quantum computing remains in its early commercial stages. While the brokerage firm sees quantum as a potential generational investment theme driven by massive market opportunities and real-world optimization benefits, it noted that the stock still faces intense competition and has yet to prove it can consistently generate meaningful revenue at scale.

About Quantum Computing Stock

Quantum Computing is an innovative photonics and quantum computing company focused on making advanced quantum technology practical, scalable, and commercially accessible. Founded in 2001 and headquartered in Hoboken, New Jersey, the company develops room-temperature, low-power quantum photonic systems designed to process complex data, strengthen cybersecurity, support AI, and improve remote sensing capabilities.

Rather than relying on expensive cooling infrastructure, QUBT aims to deliver affordable quantum solutions that simplify critical decision-making and reduce operational costs. With a market capitalization of roughly $2.66 billion, the company is positioning itself at the forefront of next-generation computing and secure communications.

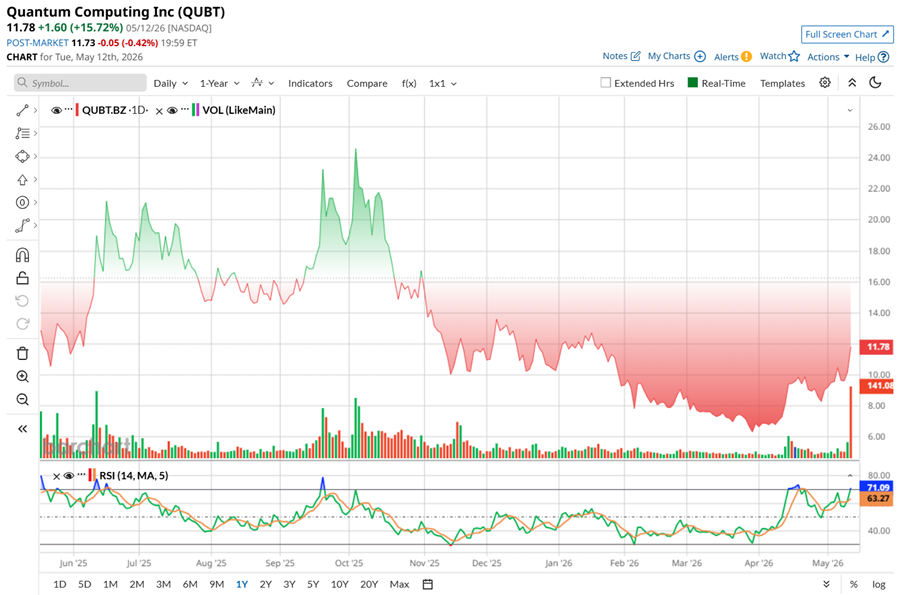

After delivering a staggering 1,710% rally in 2024, Quantum Computing entered 2025 facing a far tougher market environment. QUBT became one of the weakest-performing pure-play quantum stocks as volatility swept through speculative growth names. The stock plunged 38% during 2025, giving back a significant portion of its earlier gains. Shares hit a 52-week high of $25.84 in October before sharp valuation-driven selloffs rattled the broader quantum sector. Another wave of declines followed in November as investors grew increasingly concerned that AI and high-growth tech stocks had entered bubble territory.

Momentum started shifting again in early 2026 as investor sentiment improved around the company’s acquisitions and bullish analyst commentary. More recently, QUBT surged nearly 16% after reporting strong top-line growth, pushing the stock up 9.21% year-to-date (YTD) and 27.47% over the past 52 weeks. Shares have also rebounded 78.5% from their March low of $6.18.

Over the past month alone, the stock has soared 54.13%, fueled partly by enthusiasm surrounding Nvidia (NVDA) and its launch of Ising in April. That’s a new suite of open-source AI models designed to support quantum error correction and calibration. Those tools could become highly valuable for smaller quantum developers like QUBT, which often operate with limited financial resources.

Still, despite the recent rally, technical indicators suggest the stock may be overheating. QUBT’s 14-day RSI recently climbed to 71, placing it in overbought territory and signaling that a near-term pullback could be possible. Hence now, that 14-day RSI is sitting at 65.08.

Quantum Computing’s Impressive Q1 Report

Quantum Computing delivered a strong first-quarter 2026 report on May 11, witnessing meaningful contributions from its recent acquisitions, while continuing to expand its quantum photonics business. Revenue surged to $3.69 million from just $39,000 a year earlier and came in ahead of Wall Street's expectations. Much of that growth was driven by the acquisitions of Luminar Semiconductors in February 2026 and NuCrypt in March 2026. Excluding those deals, Quantum Computing generated $204,000 in quarterly revenue, mainly from foundry order deliveries and work tied to a NASA research subcontract.

Management said Luminar’s semiconductor capabilities are already helping accelerate the development of the stock's quantum devices and systems, while NuCrypt strengthens the company’s quantum communications portfolio by adding secure networking technologies that complement its existing platform. Together, the acquisitions aim to create a broader, end-to-end quantum toolbox for customers.

Despite strong revenue growth, Quantum Computing posted a net loss of -$4.1 million, or -$0.02 per share, compared with net income of $17 million, or $0.13 per share, in the prior-year quarter. Management noted that last year’s profit was largely tied to a one-time non-cash accounting gain related to warrant liabilities from the company’s 2022 merger with QPhoton.

Financially, the company remains well capitalized. Quantum Computing ended the quarter with roughly $1.4 billion in cash equivalents and investments, with interest income climbing sharply to $13.5 million from $1.7 million a year ago. The company also reported a contract backlog of $16 million.

Looking ahead, management is focusing heavily on scaling operations. QUBT is actively planning a second and larger foundry facility, known as Fab 2, to support higher-volume manufacturing as demand for its photonics and quantum technologies grows.

Still, analysts expect the company to remain unprofitable for the next several years, with projected losses of roughly -$0.24 per share in fiscal 2026 and -$0.29 per share in fiscal 2027 as it continues to invest aggressively in growth and infrastructure.

What Do Analysts Expect for Quantum Computing Stock?

Even with the market closely watching Quantum Computing after its strong first-quarter revenue growth, analysts at Wedbush Securities believe the company’s story is still just beginning. Wedbush noted that Quantum Computing has emerged “bigger and better” following its recent acquisitions, particularly the addition of Luminar Semiconductor, which is expected to strengthen the company’s semiconductor and photonics capabilities.

Analyst Antoine Legault expects the Luminar Semiconductor acquisition to contribute roughly $20 million to $25 million in revenue during 2026, while also helping QUBT expand its reach in the growing integrated photonics market. The deal could improve the company’s ability to scale production and compete more effectively across quantum and semiconductor applications.

Still, despite the encouraging quarter and improving outlook, Wedbush remains cautious on the stock. The brokerage firm kept its “Neutral” rating and $12 price target, arguing that the company remains a “show me” story because it is still in an earlier stage of development than many of its publicly traded quantum peers and continues to generate a comparatively smaller quantum hardware revenue base.

Meanwhile, Cantor Fitzgerald maintained its “Neutral” rating, but still sees meaningful long-term potential. The brokerage firm estimates Quantum Computing could capture roughly 5% of the global quantum hardware, software, and services market by 2035 – a share that could translate into nearly $375 million in annual revenue over the next decade.

Lake Street analyst Maxwell Michaelis is still firmly bullish on Quantum Computing, reiterating his “Buy” rating and $16 price target, pointing to the company’s rapidly expanding quantum portfolio and growing manufacturing footprint. Michaelis believes that the Luminar Semiconductor acquisition is already paying off, helping drive Q1 revenue higher while strengthening QUBT's semiconductor and photonics capabilities. Meanwhile, NuCrypt – a deal that was not even baked into earlier forecasts – gives the company another growth lane through secure quantum networking and communications. The analyst expects Luminar’s LSI unit to stay QUBT's biggest revenue driver through 2026, while NuCrypt broadens the company’s reach into cybersecurity and quantum communications.

He also pointed to growing momentum at QUBT's Fab 1 facility in Tempe, which has already begun generating early foundry revenue from small-batch production runs. Quantum computing may still be in its early chapters, but Michaelis believes Quantum Computing has the balance sheet, product lineup, and expansion plans to stay in the game for the long haul.

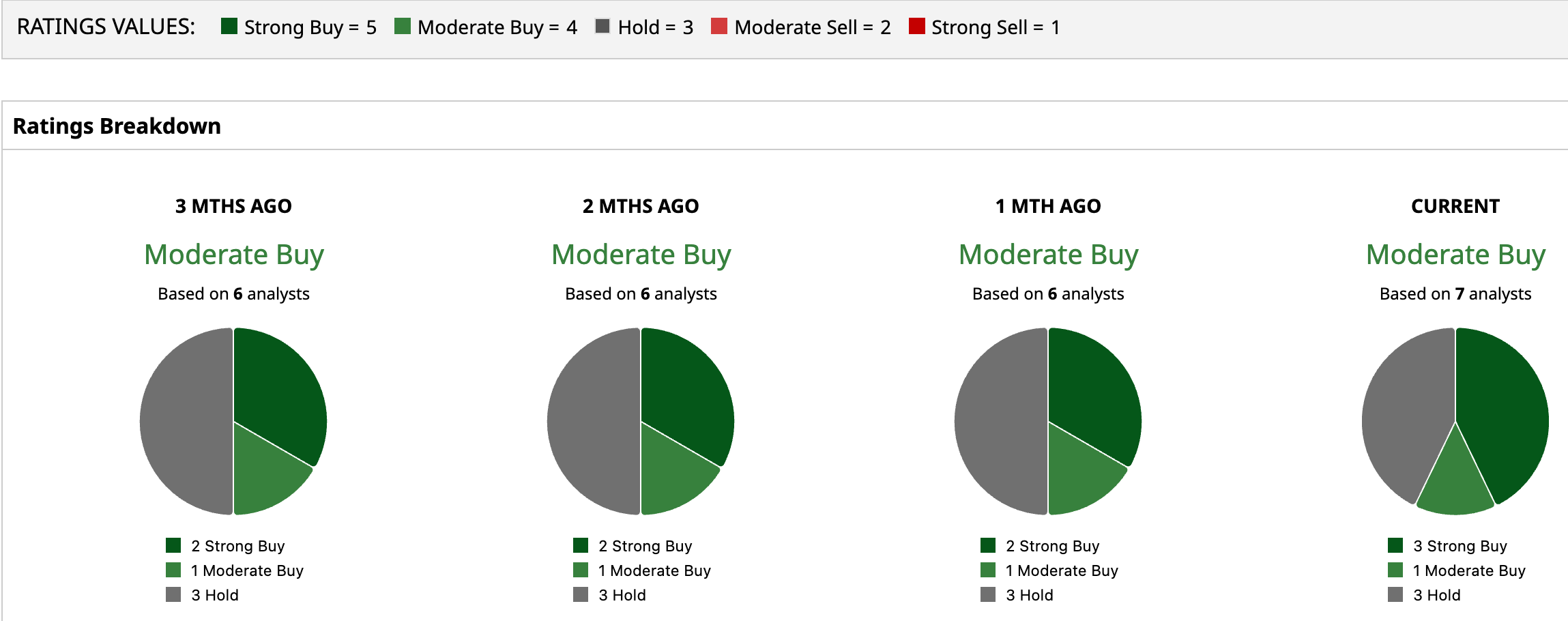

QUBT stock currently has a consensus “Moderate Buy” rating overall. Of the seven analysts covering the stock, three advise a “Strong Buy,” one has a “Moderate Buy,” and the remaining three play it safe with a “Hold.”

While QUBT’s mean price target of $17.83 suggest a rebound potential of 62.24% from the current price levels, the Street-high target price of $27 implies that the stock could rally as much as 145.7% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)