/Lululemon%20Athletica%20inc_%20phone%20and%20website%20by-%20T_Schneider%20via%20Shutterstock.jpg)

I’ve followed Lululemon (LULU) for over a decade. When LULU came across my radar, it didn’t have a men’s line, it wasn’t in China, and the American market was starting to pop with 171 stores. Today, there are 379.

Therein lies the problem.

Americans have stopped shopping at its stores. Well, not completely; they’re just not visiting as often. That’s sent the stock to 37 new 52-week lows in the past 12 months alone. Yesterday, it hit a five-year low of $123.51.

On a scale of 1 to 10, this falling knife is an 11. The Barchart Technical Opinion rates it a 100% Strong Sell in the near-term. You can’t get any worse than that.

Founder Chip Wilson, the company’s third-largest shareholder with 7.17% of the stock, continues to fight the board over its management of the brand he created in 1999, ran until stepping down as CEO in 2005, and finally, his role as chairman in 2013.

At LULU’s all-time high of $516.39 in December 2023, Wilson’s current holdings were worth $4.26 billion. Those same holdings are worth just over $1 billion today.

He’s got a right to be upset about what’s happened to the brand. Forbes estimates his net worth at $5.5 billion, which isn’t chump change, but it would be a lot higher if not for the collapse in Lululemon’s share price.

On May 6, Wilson released a public letter to shareholders, outlining his concerns about the company, most notably, its board, and their inability to understand what brought LULU to the dance: Innovation and disruption.

There is no question that the company is at a crossroads. What it does in the next 12-18 months will define its future.

If you’re a contrarian risk-taking investor, here’s why you should be interested in a possible high-risk bet.

There’s Been Plenty of Fires to Put Out

As I said, I’ve followed LULU for a long time. There have been many short-term fires to put out over the years.

Wilson himself was at the center of the 2013 controversy, where he said in a Bloomberg TV interview, “Some women’s bodies just don’t work” for his yoga pants.

“Even our small sizes would fit an extra large, it’s really about the rubbing through the thighs, how much pressure is there…over a period of time, and how much they use it,” CBC reported his 2013 comments.

He’s been paying for those comments ever since.

Next up is former CEO Laurent Potdevin. The board hired him in December 2013 to replace outgoing CEO Christine Day, who had struggled to keep Lululemon growing under intense competition.

Potdevin, who was CEO of Burton Snowboards between 2005 and 2010, spent the next four years growing the company and solidifying its brand position in apparel. The stock did reasonably well under his tenure.

However, in February 2018, he stepped down after admitting he had a multi-year relationship with one of the company’s female designers.

The search for a new CEO would take five months, and the company would hire Sephora’s CEO for the Americas, Calvin McDonald, who stayed with Lululemon until stepping down in January.

During McDonald’s tenure, LULU stock did well until the end of 2024. By the time he was done, the share price had fallen by 50%. You know what’s happened in the three months since.

Wilson’s been quick to point out that the company has lost its passion for innovation and disruption. Even McDonald admitted as much, saying last September that its products had become “too predictable.”

Finally, in 2026, there was the controversy over its new leggings being too transparent. It made things worse by saying women weren’t wearing them right. The brand's quality, which had been its hallmark, really came into question.

And now it has hired former Nike (NKE) executive Heidi O’Neill as the champion of its turnaround.

Mixed Opinions

On April 22, Lululemon announced that O’Neill would become the next CEO effective Sept. 8. Wait, what? That’s almost four months from now. I get that the woman has things to wrap up in her life, but she stepped down from her role at Nike in May 2025.

Don’t get me wrong, I’m pro LULU, but that’s another example of the board not showing urgency in the company’s situation. Weren’t there any high-caliber candidates available who could start on June 1? May 1? Not a good look.

There are plenty of pros and cons to O’Neill’s appointment. You can find them all over the internet.

The things that I like.

She’s a woman. That’s key. She worked for almost 30 years at a company focused on athletic performance, though it has lost its way in recent years. She was a potential CEO candidate to lead the Nike turnaround plan, which ultimately went to her longtime colleague, Elliott Hill. That alone suggests she’s more than capable of leading Lululemon. Lastly, O’Neill’s experience with strategy and product development makes her an ideal person to address Lululemon’s current shortcomings.

The things I don’t like.

Well, I already mentioned the late starting date, but that’s not a dealbreaker. There’s nothing in O'Neill's resume that screams red flag. The biggest problem is she’s got a board that’s fighting with Wilson on one side and an American consumer who’s lost their enthusiasm for spending buckets of money there. Last time I looked, American consumers have no such problem spending lots at Aritzia (ATZ.TO), its Vancouver-based peer. That’s got to be remedied before it can take on serious international expansion.

There’s no question O’neill’s entering the hornet’s nest.

The Last Time LULU Traded Under $100

The answer to that is April 2018, slightly more than eight years ago. I mention this benchmark because it’s important to stress that LULU stock could easily fall another $25 in the next month or two.

That’s the reality. If you can’t afford to lose in the near-term, you shouldn’t even be contemplating a risk-on bet like this.

However, if you have ironclad risk tolerance, the profit potential over the next 24 to 36 months could be tremendous. But that’s a big if.

The biggest thing Lululemon has going for it is its cash flow generation.

When its share price hit an all-time high in December 2023, the company reported cash flow of $2.30 billion for that fiscal year on revenue of $9.62 billion. Its free cash flow margin was 17.0%. In 2025, it was $1.60 billion on $11.10 billion in revenue. Its free cash flow margin was 8.3%.

On the one hand, its free cash flow margin has fallen by 51% in just 24 months. On the other hand, the free cash flow margin of 6.4% is 280 basis points higher than at the end of 2023.

While there’s a good chance cash flow will continue to decline until a plan gains traction, the upside, if all goes well, is too great to overlook.

As I check the options trading this morning, I see two possible trades on long calls.

The first is a speculative bet that Lululemon’s Q1 2026 report on June 4 will beat expectations. I’m not holding out much hope. The July 17 $130 call is about 22% OTM (out-of-the-money). Expiring well after earnings are out, you’ve got some time to recover if things are worse than expected. Worst case, you’re out $850 or 2.5% of LULU’s share price.

The second is a LEAPS (Long-Term Equity Anticipation Securities) bet. I tried to find something about 18 months out from O’Neill’s September CEO start. This gives her a year to get to know the business and develop a strategy, and then another six months to see it gain traction.

The second is a LEAPS (Long-Term Equity Anticipation Securities) bet. I tried to find something about 18 months out from O’Neill’s September CEO start. This gives her a year to get to know the business and develop a strategy, and then another six months to see it gain traction.

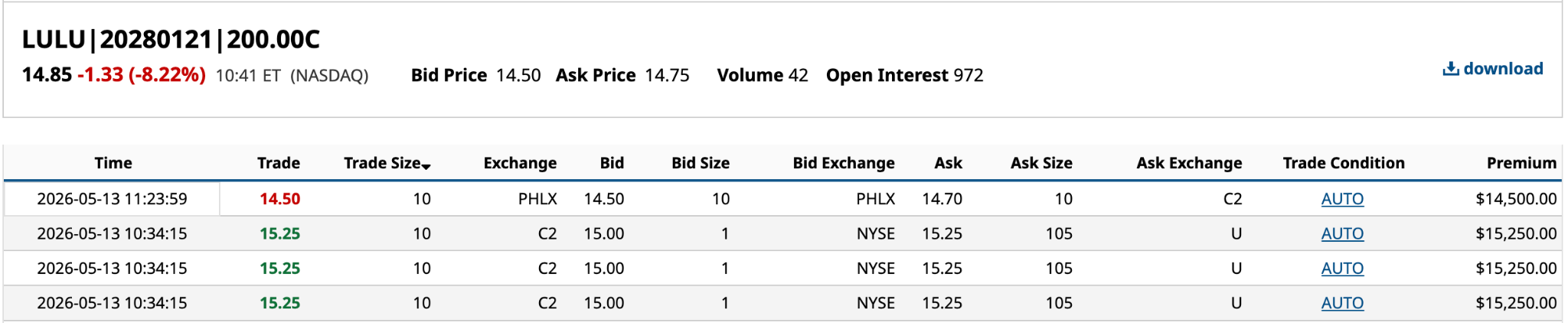

The best I could find with volume today and the closest to March 2028 was the Jan. 21/2028 $200 call. It had four trades of 10 contracts each as I wrote this.

OTM by 63%, even at $15.25, the call is just 12% of LULU’s share price. With a delta of 0.3688, you can double your money if the share price appreciates by $41.35 (33.6%) and you sell to close the position before expiration. The expected move, up or down, is 43.06%, so it’s possible, if not likely. Worst case, you roll it out 6-12 more months if the play still looks worthwhile.

Good luck.

On the date of publication, Will Ashworth had a position in: LULU . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.