/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)

Tesla (TSLA) and SpaceX appear to be laying the groundwork for something far bigger than a semiconductor project. Over the weekend, Elon Musk introduced plans for “Terafab,” a massive chip fabrication initiative in Austin, Texas.

The project brings both companies under one roof to build advanced semiconductor capacity tailored for artificial intelligence (AI), robotics, and space computing. Wedbush Securities sees more than just vertical integration here. The firm is reading this as the first real step toward a potential merger, possibly as early as 2027.

The facility could cost up to $25 billion and span everything from chip design and lithography to packaging and testing. Initial output targets 100k wafer starts per month, with ambitions to scale to one million, a level that would approach nearly 70% of Taiwan Semiconductor Manufacturing Company Limited’s (TSM) global output.

Current AI compute output sits near 20 gigawatts annually, barely scratching roughly 2% of internal demand. Supply constraints are continuing to choke progress. By taking control of chip production, Tesla and SpaceX would remove that bottleneck and accelerate their AI roadmap. If executed well, this move would reshape the playing field.

About Tesla Stock

Best known for its electric vehicles (EVs), Tesla has steadily expanded into energy storage, solar solutions, and software-driven services. The Austin, Texas-based company operates with a vertically integrated model, selling vehicles directly while building its own batteries, AI systems, and charging infrastructure.

Tesla carries a market cap of approximately $1.45 trillion, reflecting both dominance and expectation. Over the past 52 weeks, the stock has gained nearly 36.77%, though it has pulled back 17.26% year-to-date (YTD), signaling some near-term pressure.

Valuation adds tension to the narrative. The stock is currently trading at 185.52 times forward adjusted earnings and 14.02 times sales. The figures sit well above both industry peers and their own five-year historical averages, reflecting a premium.

Tesla Surpasses Q4 Earnings

On Jan. 28, Tesla delivered Q4 fiscal 2025 results that beat both top and bottom line expectations, even as the underlying picture stayed uneven. The company reported revenue of $24.9 billion, down 3.1% year-over-year (YOY) but ahead of the $24.79 billion analyst estimate. Adjusted EPS came in at $0.50, down 16.7% from the prior year’s period but cleared the $0.45 Street forecast.

The pressure showed up clearly in automotive. The segment pulled total revenue lower, with automotive sales dropping 10.6% year over year to $17.7 billion. At the same time, other parts of the business picked up the slack. Energy generation and storage revenue rose 25.4% to $3.9 billion, while services and other revenue jumped 18.4% to $3.4 billion.

Margins moved in the same direction as automotive. Adjusted EBITDA fell 4.1% to $4.1 billion, and non-GAAP net income declined 16.4% to $1.8 billion. Deliveries also slipped, down 15.6% to 418,227 units, reinforcing the softer demand backdrop.

Cash flow held up better than expected. Free cash flow reached $1.4 billion, and CapEx came in slightly below the previous guidance of $9 billion. The restraint will not carry forward. Management is preparing for a heavy investment cycle, with CapEx set to exceed $20 billion.

The company plans to fund six major facilities, including a refinery, LFP factory, Cybercab, Semi, a new Megafactory, and the Optimus factory, while continuing to build out AI compute infrastructure and expand Robotaxi and Optimus deployments.

All being said, analysts expect Q1 fiscal year 2026 EPS to rise 60% YOY to $0.24. For the full year, the bottom line is projected to climb 32.1% to $1.44, followed by another 36.1% increase to $1.96 in fiscal year 2027.

What Do Analysts Expect for Tesla Stock?

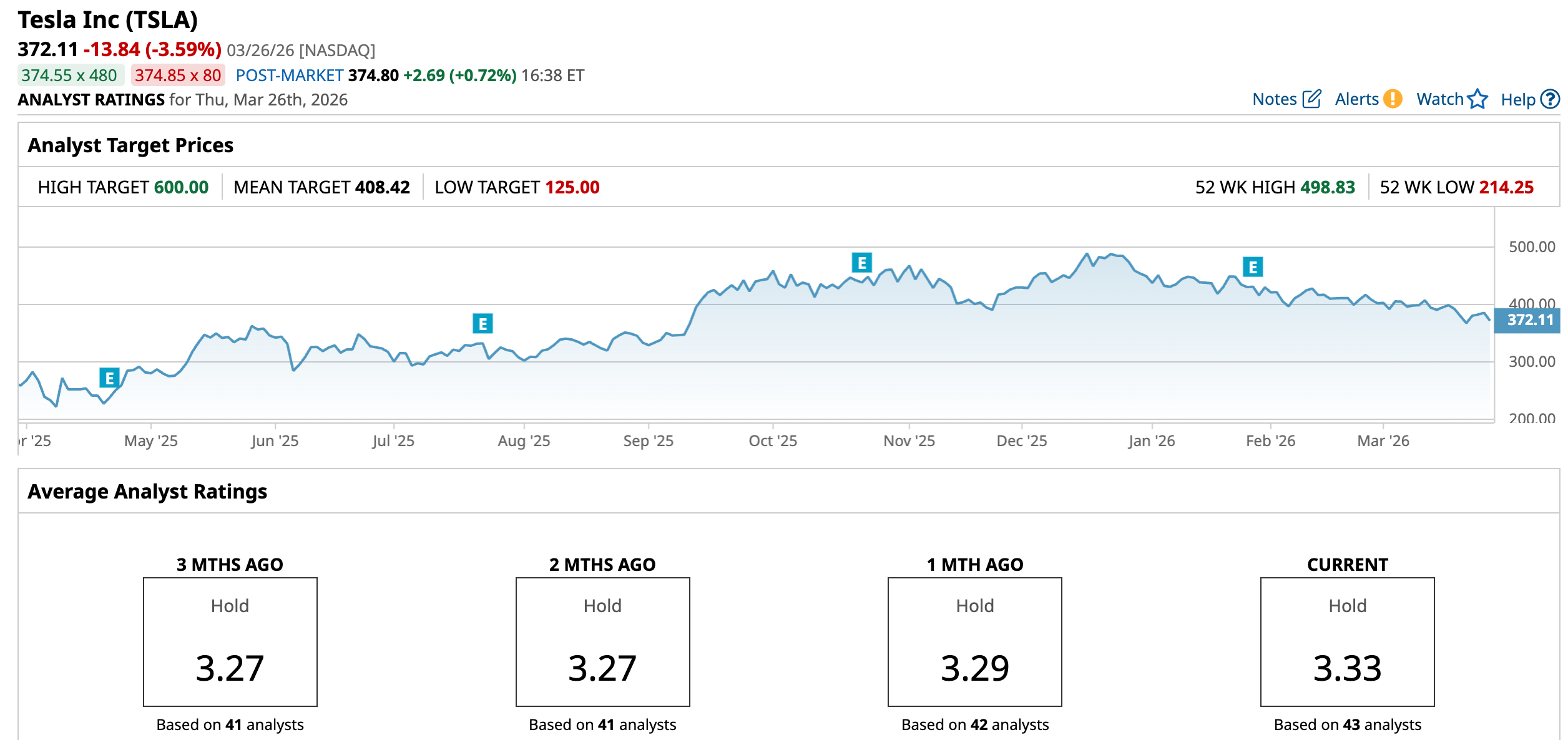

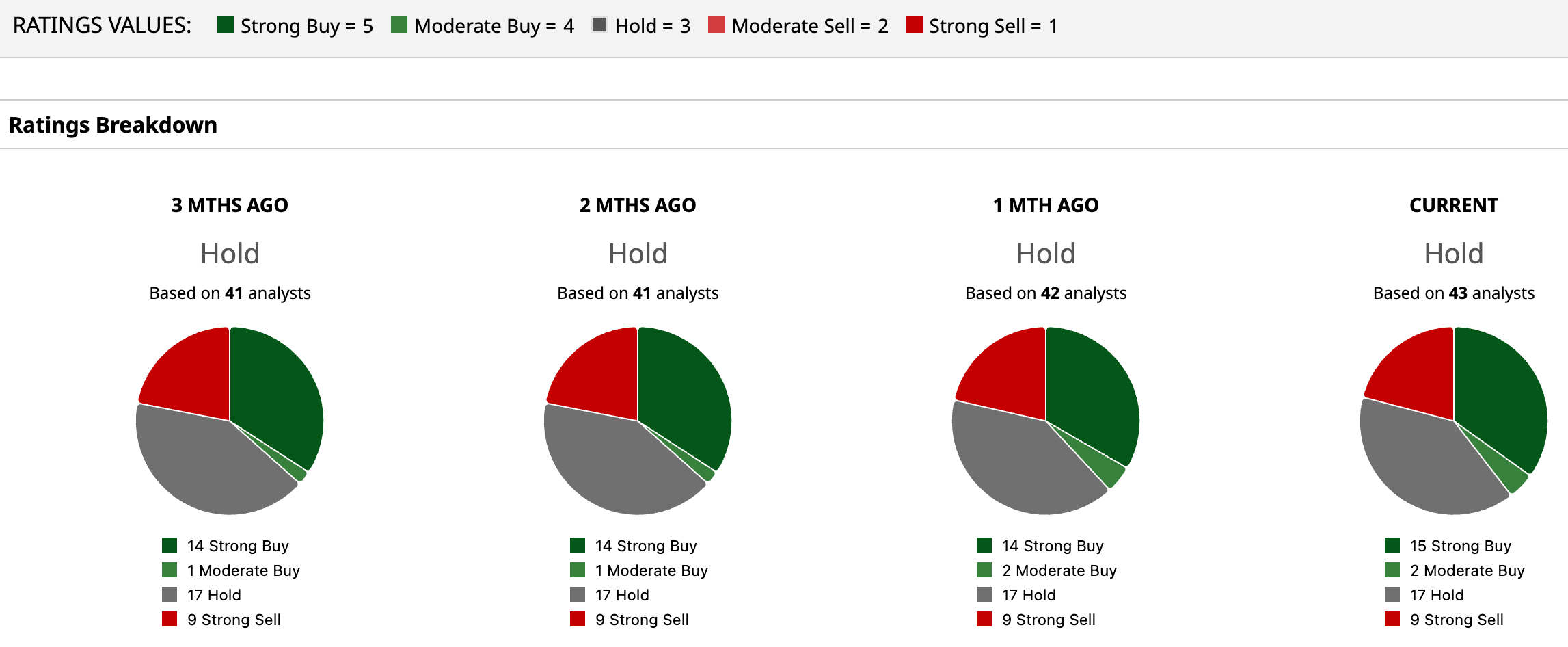

Currently, the broader analyst community has assigned the stock an overall rating of “Hold.” Among 43 analysts covering the stock, 15 have rated it a “Strong Buy,” two suggest “Moderate Buy,” 17 opt to “Hold,” while nine have flagged a “Strong Sell.”

Price targets lean optimistic, though. The mean price target of $408.42 signals potential upside of 9.8%. Meanwhile, the Street-high target of $600 set by Wedbush analyst Daniel Ives suggests a gain of 61.2% from current levels. He maintains an “Outperform” rating, anchored in confidence around Tesla’s growth trajectory.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)