- Despite continued short-term and long-term bullish fundamentals in corn and soybean, investment funds have been exiting the markets since last February and March.

- Some of this is due to the global fight against inflation, most notably central banks around the world raining interest rates.

- However, this action has changed supply and demand, and with weather bubbling up again both corn and soybeans could find renewed investor buying interest once the July Fed meeting is out of the way.

As most of you probably know, Barchart sponsors the daily market segment on RFD-TV that I take part in each Tuesday (8:15 CT) and Wednesday (8:45 CT). Usually, I get to visit with my friend Marlin Bohling, as was the case earlier today (Wednesday, July 27). As our conversation unfolded, we started talking about the expected interest rate hike by the US Federal Reserve early in the afternoon, the general consensus seemingly settled on 75-basis points. My thought on the subject, and what I shared on air, is once today has come and gone it could be invitation for investment traders to come back to the commodity complex. This could be a boon for those markets with bullish long-term fundamentals (most energies, softs, grains and oilseeds), with the spotlight possibly on corn and soybeans.

You’ll likely recall I jumped the gun with my piece from early in July, though I stick by the major premise that supply and demand will trump interest rate hikes by central banks around the world. After all, there is such a thing as Newsom’s Market Rule #6: Fundamentals win in the end. As I’ve talked about numerous times of late, the supply and demand situation for both US corn and soybeans remains tight heading into the end of the 2021-2022 marketing year and beginning of 2022-2023.

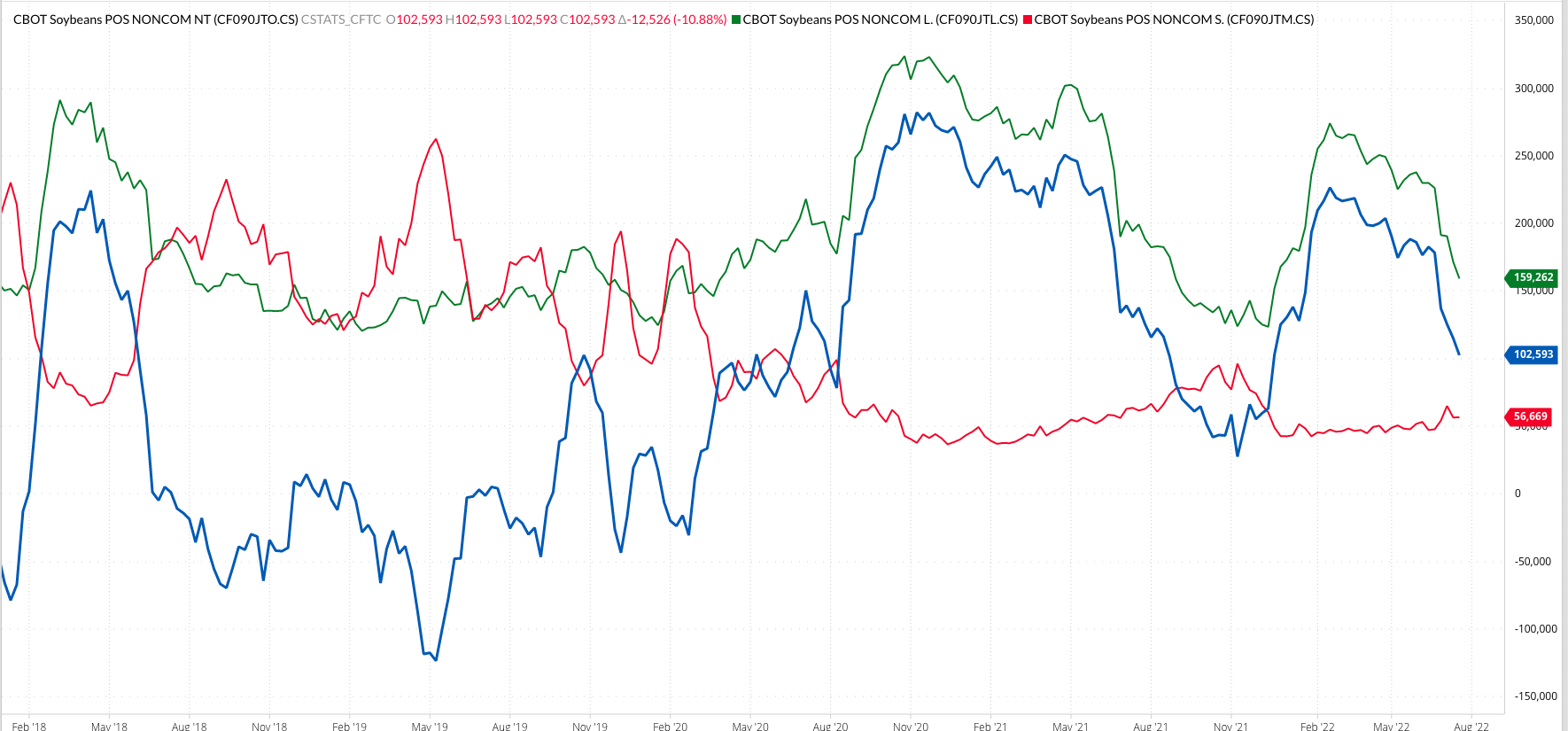

Starting with soybeans for a change, this week has seen the market explode higher. While all the attention is on the new-crop November futures contract (ZSX22) as weather forecasts for the first-half of August remain hot and dry[i], we can’t forget about what is going on with old-crop. The August and September futures contracts are largely forgettable, and a key reason why nearby-futures only funds have stayed out of the soybean market for a while, but a look at the daily close-only chart for this spread shows the inverse has moved out to $1.50. This is reminiscent of the move made in 2013, the last time national cash indexes were as high as they are at this point of the marketing year. This tells us US available stocks-to-use are indeed as tight as what I’ve been talking about, making the margin for error for 2022 production near non-existent. Add in the fact the forward curves for both soybean oil and meal are inverted, indicating bullish long-term fundamentals for those markets as well, and funds could see this as an opportunity to buy back into November futures with August going into delivery at the end of this week. Keep in mind this group has reduced its net-long futures position by 55% since late February, so there is ample room to rebuild on bullish fundamentals.

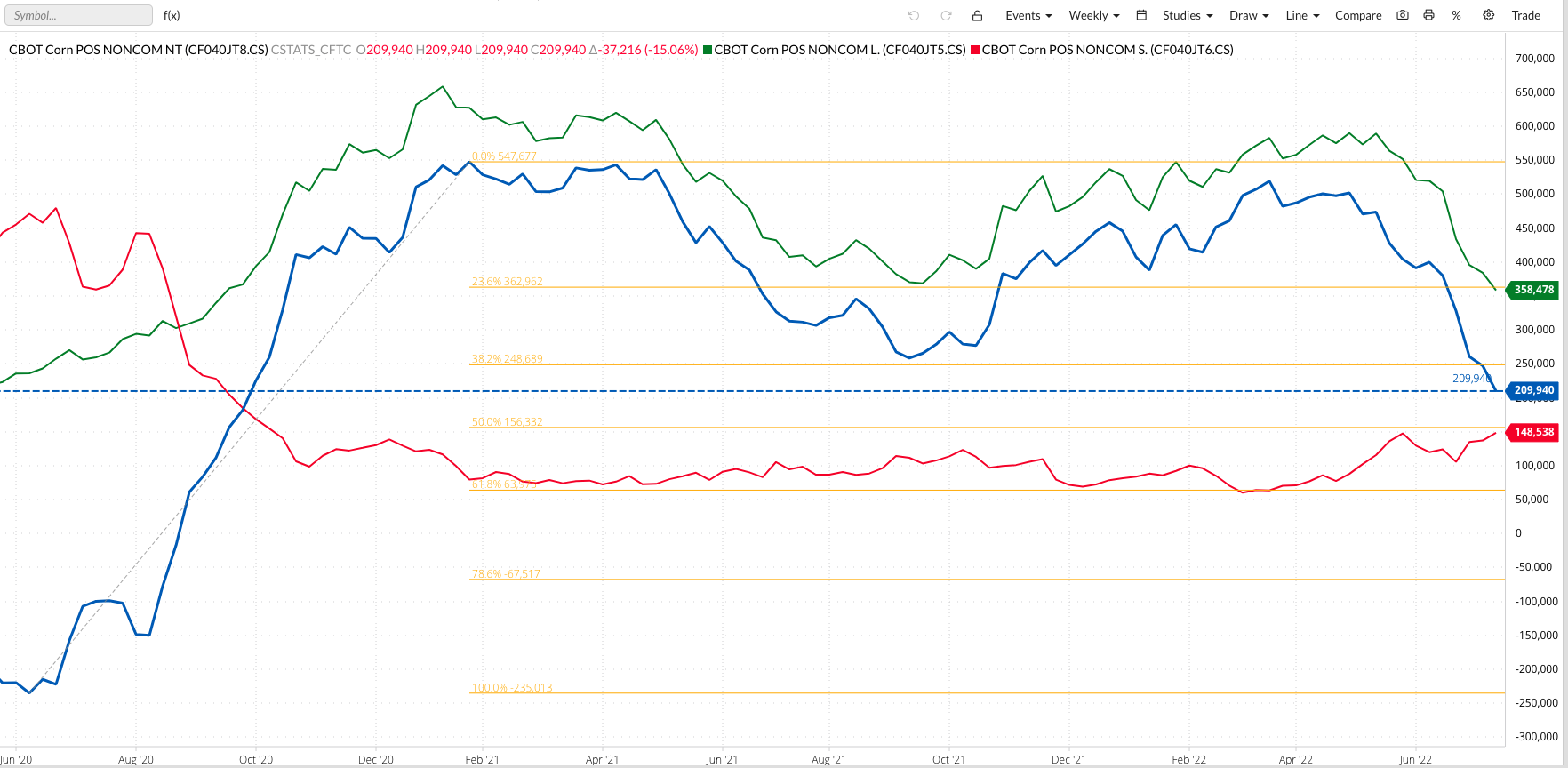

My thoughts on corn are well documented, but I’ll say it again: Corn remains fundamentally bullish both short-term and long-term. We can see this in the strength of the Barchart National Corn Basis Index (ZCBAUS.CM) and the weak carry of the Dec-July futures spread. Noncommercial interest have reduced their net-long futures holdings by about 60% since late March, all while those funds still in the market are set to roll their position from September to more heavily traded December issue the first week-plus of August. Again, I don’t think investment traders have anything to fear from the Fed, and instead could feed on the fact the latest interest rate hike is out of the way, putting the 2022 crop center stage for the next few months.

[i] It is August, after all, also known as the Dog Days of Summer. The month didn’t earn this nickname because it is usually cool and comfortable.

More Grain News from Barchart

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)