Tyson Foods, Inc. (TSN), headquartered in Springdale, Arkansas, is a global leader in food processing, specializing in chicken, beef, and pork products. Its expansive operations include supplying high-quality protein to retail and food service markets across more than 80 countries.

With a market capitalization of $18.28 billion, Tyson Foods has announced new product launches and strategic investments to strengthen its market position and drive future growth, demonstrating a commitment to innovation and sustainability.

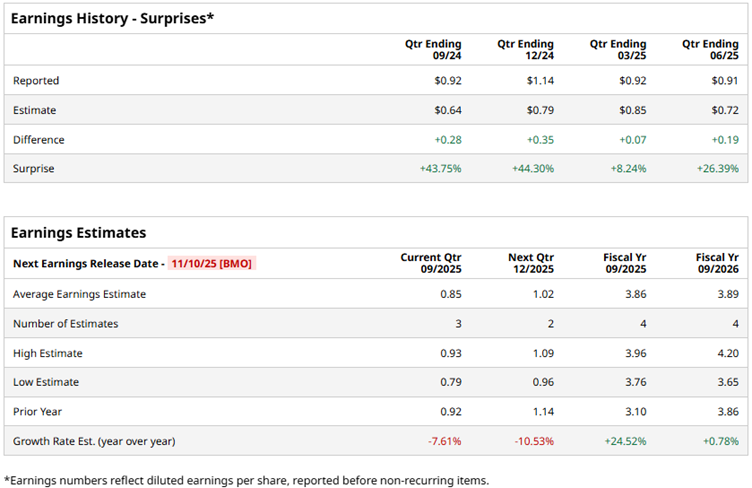

Tyson Foods is set to report its fourth-quarter results for fiscal 2025 on Nov. 10 before the market opens. Ahead of the results, Wall Street analysts have a mixed view about the company’s bottom-line growth trajectory.

For the quarter about to be reported, analysts expect Tyson Foods’ profit to decline by 7.6% year-over-year (YOY) to $0.85 per diluted share. On the other hand, for the current fiscal year, profit is projected to climb 24.5% annually to $3.86 per diluted share. It should also be noted that the company has a solid history of beating consensus estimates in each of the trailing four quarters.

The company is facing pressures such as tight supply and rising costs, including an agreement to pay $85 million to settle a lawsuit alleging the company colluded with rivals to inflate pork prices by limiting supply.

As a result, Tyson Foods’ stock has been underperforming the broader market. Over the past 52 weeks, the stock has dropped by 11.2%, and it is down 9.3% year-to-date (YTD), while the broader S&P 500 Index ($SPX) has gained 18.4% and 16.9% over the same periods, respectively.

Comparing it with the Consumer Staples Select Sector SPDR Fund (XLP), we see that the ETF has dropped 2.3% over the past 52 weeks and has marginally gained YTD. Therefore, Tyson Foods has underperformed its sector over these periods.

On Aug. 4, Tyson Foods reported its third-quarter results for fiscal 2025 (the quarter that ended on June 28). As the earnings topped estimates, the company’s stock gained 2.4% intraday on the same day. Its Q3 revenue increased by 4% YOY to $13.88 billion. Its adjusted EPS of $0.91 increased 4.6% from the prior year’s period and surpassed the analysts’ estimated figure of $0.72.

Wall Street analysts are cautious about Tyson Foods. Among the ten analysts covering the stock, the consensus rating is “Hold.” The ratings configuration is more bearish than it was a month ago, with the addition of one “Strong Sell” rating. The ratings are completed by two “Strong Buys” and seven “Holds.”

The mean price target of $59.90 indicates a 15% upside from current levels, while the Street-high price target of $75 implies a 44% upside.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)