/Supermicro%20headquarters%20in%20San%20Jose%2C%20By%20JHVEPhoto.jpeg)

With a market cap of $16.2 billion, Super Micro Computer, Inc. (SMCI) is a global leader in Application-Optimized Total IT Solutions, delivering innovative infrastructure for enterprise, cloud, AI, 5G, and edge computing. With in-house design and manufacturing across the US, Taiwan, and the Netherlands, the company provides high-performance, energy-efficient server, storage, networking, and AI solutions that help customers optimize performance while reducing total cost of ownership and environmental impact.

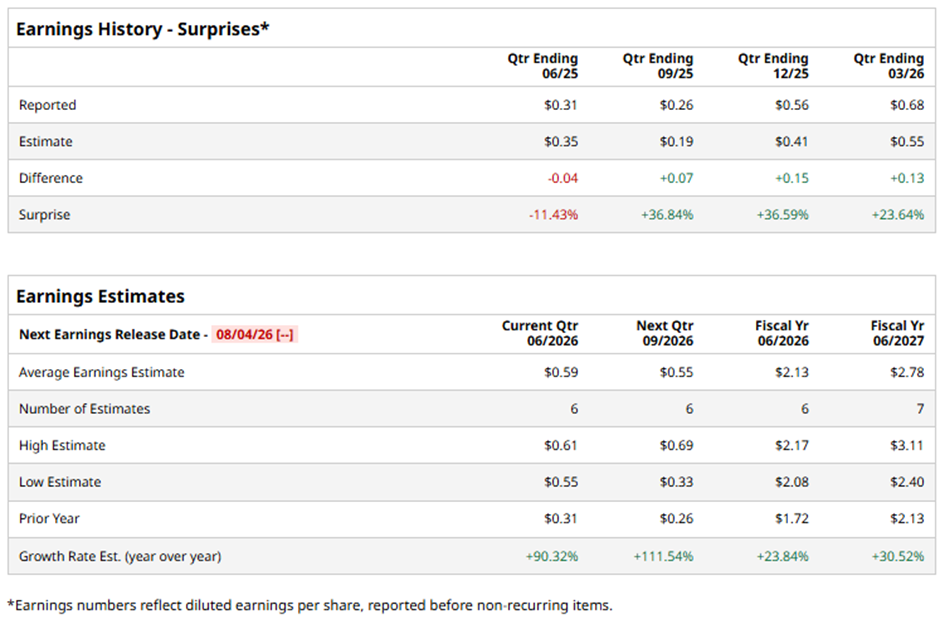

Headquartered in San Jose, California, the company is set to announce its fiscal Q4 2026 results soon. Ahead of this event, analysts expect SMCI to report an EPS of $0.59, a 90.3% surge from $0.31 in the year-ago quarter. It has exceeded Wall Street's earnings expectations in three of the past quarters while missing on another occasion.

For fiscal 2026, analysts predict the server technology company to post EPS of $2.13, an increase of 23.8% from $1.72 in fiscal 2025. Moreover, EPS is anticipated to grow 30.5% year-over-year to $2.78 in fiscal 2027.

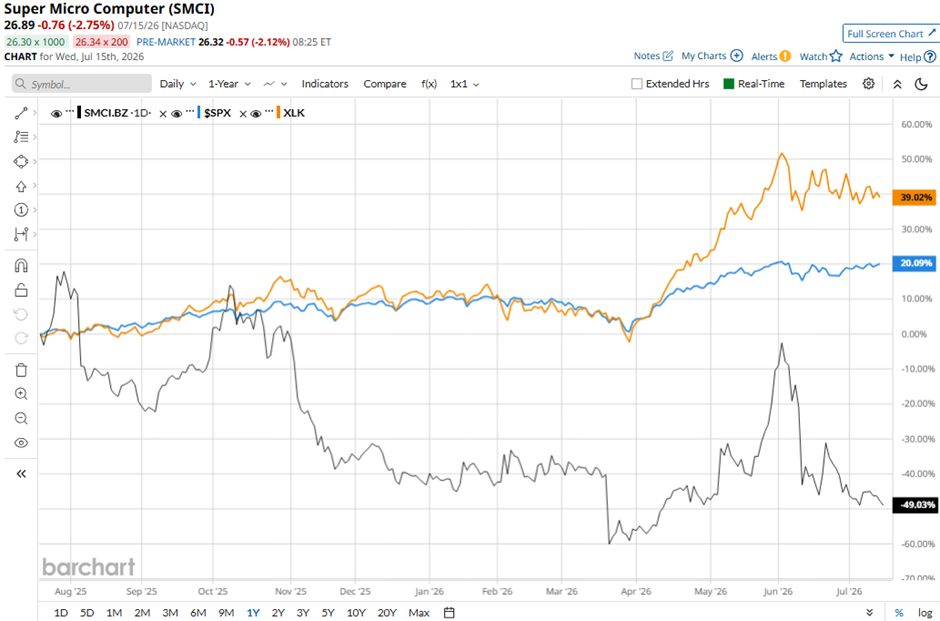

Shares of Super Micro Computer have dipped 49.4% over the past 52 weeks, lagging behind the broader S&P 500 Index's ($SPX) 21.3% return and the State Street Technology Select Sector SPDR ETF's (XLK) 40.8% gain over the same period.

Super Micro Computer shares soared 24.5% following its Q3 2026 results on May 5 after the company issued a strong Q4 outlook, forecasting revenue of $11 billion - $12.5 billion and adjusted EPS of $0.65 - $0.79, well above the consensus estimate. Investor sentiment was also boosted by management's confidence in robust AI server demand, aggressive capacity expansion across Taiwan, Malaysia, and the Netherlands, and confirmation that its relationships and AI chip allocations from Nvidia, AMD, and Intel remained unaffected despite the U.S. Justice Department investigation.

Analysts' consensus view on SMCI stock remains cautious, with an overall “Hold” rating. Out of 20 analysts covering the stock, three recommend a "Strong Buy," two "Moderate Buys," 12 "Holds," one has a "Moderate Sell," and two give a "Strong Sell" rating. The average analyst price target is $35.56, indicating a potential upside of 32.2% from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)