/Apple%20Ipad%20via%20Storyblocks.jpg)

The battle between Apple (AAPL) and OpenAI is becoming more serious than many thought. The iPhone maker recently sued Sam Altman’s OpenAI, alleging they stole company secrets to build their hardware business. Apple isn’t complaining about a single leak or an individual. The firm believes OpenAI, through interviews and former Apple employees, ran a planned operation to steal Apple’s trade secrets. It alleges that OpenAI’s senior management was involved, including Tang Tag, a 24-year Apple veteran who oversaw flagship products like the iPhone and Apple Watch.

The reason this is important for Apple is that the tech giant is already struggling to build its AI credibility. Its much-hyped AI-enhanced Siri only recently started shipping after a two-year delay, built on Google's (GOOG) (GOOGL) Gemini instead of the company’s own AI model. The company chose Google because of OpenAI’s hardware ambitions, which it saw as a threat. By launching the lawsuit, Apple is now conceding that it needs outside AI help to compete and feels threatened by OpenAI, irrespective of whether Sam Altman’s firm stole the tech or not.

Investors are keenly following the lawsuit not because they want to find out if Apple’s accusations are true or not. There is much more at stake than OpenAI’s hardware ambitions. OpenAI is already struggling to achieve its internal revenue and user growth targets. It is also a part of Project Stargate, the U.S. government’s initiative to ensure America’s dominance in artificial intelligence. Larry Ellison’s Oracle (ORCL), which boasts a $638 billion backlog, depends on OpenAI for half of it. And that’s what is spooking investors more about OpenAI than any shenanigans on the hardware division front. There is so much at stake here that a misstep by OpenAI, which doesn’t enjoy a great reputation to begin with, could bring down with it a major part of the AI ecosystem. In this way, stock market participants are hoping OpenAI can survive this without triggering an AI bubble burst.

About Apple Stock

Apple is one of the world’s largest technology companies that designs and manufactures consumer electronics, digital services, and software. Its product portfolio includes the iPhone, iPad, Mac, AirPods, Apple Vision Pro, and Apple Watch. The company also offers services such as iCloud, Apple Music, Apple Pay, and the App Store. Founded in 1976, the company is headquartered in Cupertino, California.

Over the last 12 months, AAPL stock has risen 57%, comfortably outperforming the S&P 500’s ($SPX) 20.8% gain over the same period. The rise was driven primarily by a record earnings quarter and strong iPhone 17 demand. The stock went up further after Apple’s AI announcements at WWDC 2026 were well received by investors. However, the stock price has taken a hit recently, falling over 6% on June 25 alone. The decline comes after Apple increased prices across its Mac and iPad products to overcome what the CEO believes is a hundred-year flood in memory and storage costs.

Apple’s valuation sits at a slight premium to its historical norms. The forward GAAP P/E is 32.40x compared to the firm’s 5-year average of 29.03x, while the forward price-to-sales ratio is 8.71x compared to the 5-year average of 7.46x. The premium reflects investor confidence in Apple’s growing services revenue and long-term AI potential. EPS growth trajectory looks healthy, with a 17% gain expected in 2026. It is expected to slow down in the next couple of years while maintaining positive growth and then reaccelerate to over 19% in 2029. Capital structure remains one of Apple’s greatest strengths. A net debt of $16.2 billion feels insignificant for a company with an extraordinary $4.17 trillion market cap. This financial strength gives investors confidence to pay a premium for Apple’s stock, even during a period of high AI investments and a severe memory chip shortage. The company has also recently returned $100 billion to shareholders through buybacks.

Apple Delivers Another Solid Quarter

Apple reported its second-quarter fiscal 2026 earnings on April 30. The firm beat the analyst consensus on both key metrics. Revenue increased 17% year-on-year (YoY) to $111.2 billion, while the diluted EPS had an even bigger growth of 22% to $2.01. CEO Tim Cook described the results as the best March quarter in the firm’s history, with iPhone revenue also reaching a record high. The services revenue reached a record $26.65 billion, up 14% YoY, while the gross margin also increased considerably by nearly $10 billion. The CFO noted that strong customer demand helped Apple reach a new all-time high in its installed base of active devices across all major products and geographic segments.

For the third quarter, the CFO guided revenue to grow 14% to 17% YoY, easily beating the analyst consensus of 9.5%. The revenue outlook improved after Apple decided to increase its Mac and iPad product prices by 15-25%. However, this also raised concerns among the investors as the increase was due to Apple trying to tackle the surging memory costs issue. The management has also acknowledged a supply constraint issue, with the supply unlikely to match demand for several months. Apple also faced a 19% YoY decline in China iPhone shipments, making its market share fall from 16% to 11%.

What Analysts Are Saying About AAPL Stock

Wedbush analyst Daniel Ives has set AAPL stock's price target at $400 while maintaining an “Outperform” rating. The analyst believes that the recent price hikes do not carry a significant risk for Apple, since the company has a large, higher-end customer base that will be less price sensitive than the market reaction suggests. Some analysts, such as Barclays’ Tim Long, feel the investors’ concern is justified, maintaining a “Sell” rating for the firm.

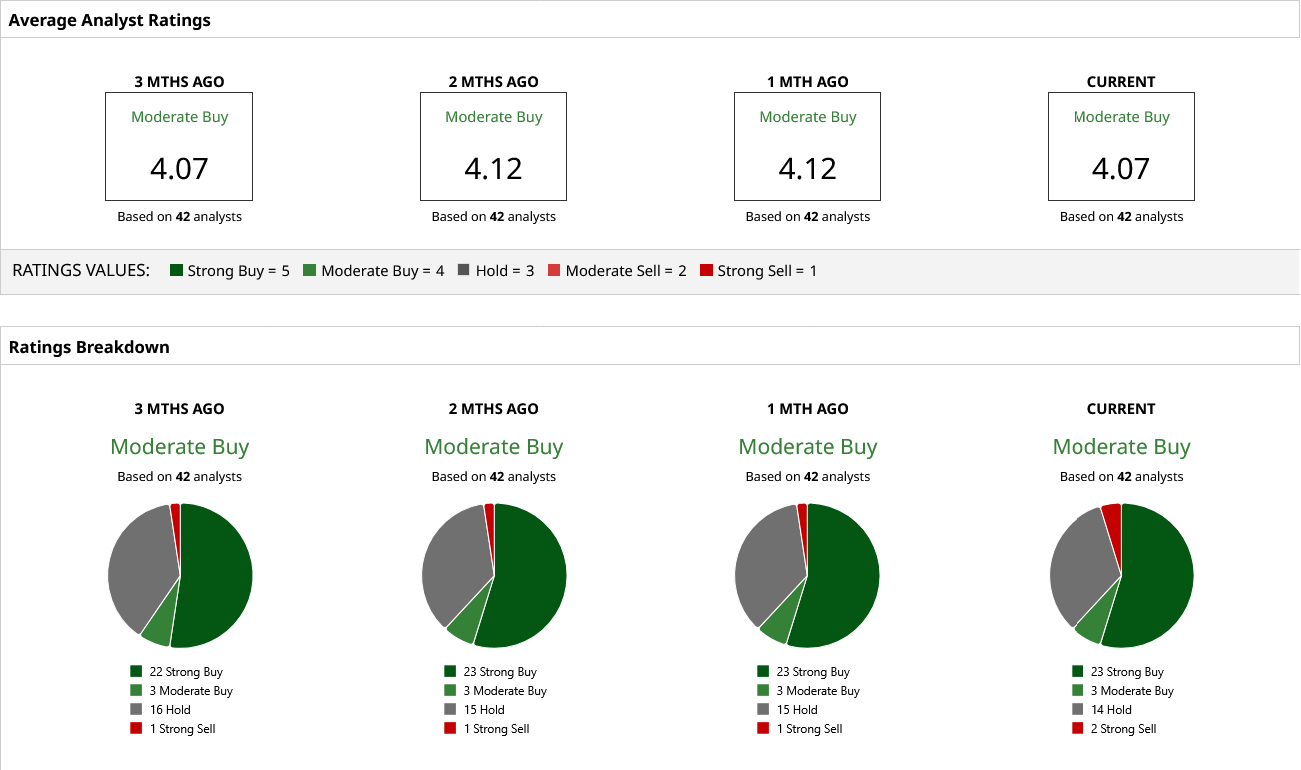

Based on the 42 Wall Street analysts, AAPL holds a consensus “Moderate Buy” rating with a mean price target of $316.73, which the stock currently trades just slightly above. The wide price target range of $235 to $400 reflects differing views on the stock's value. While the bulls continue to believe in the firm’s long-term potential, the bears remain cautious about the memory cost pressure and the China market share decline.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)