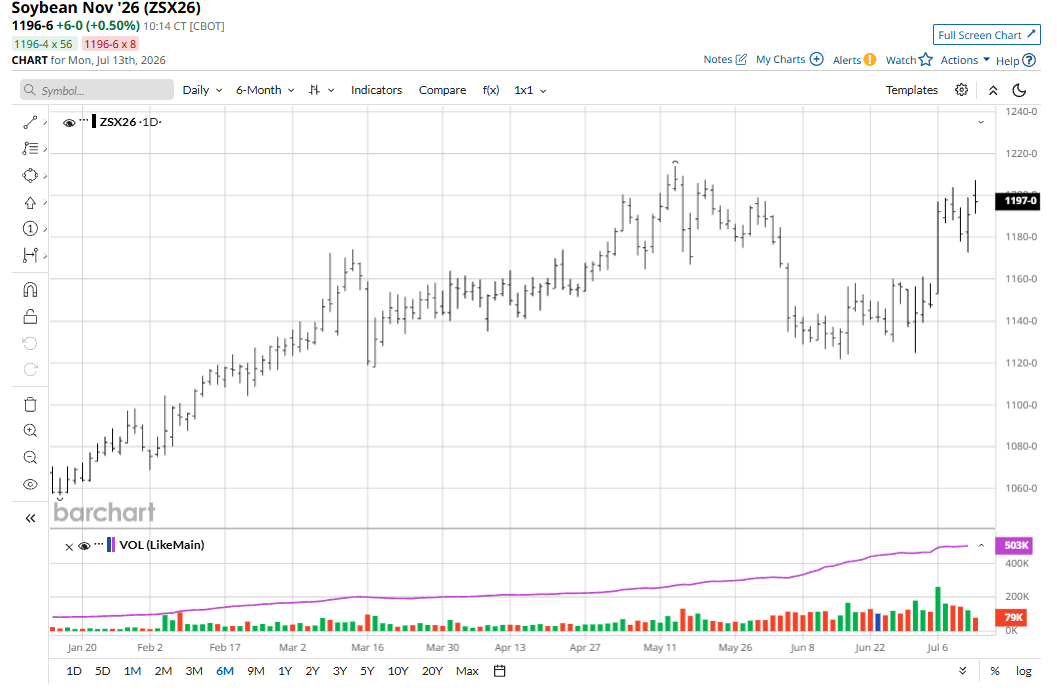

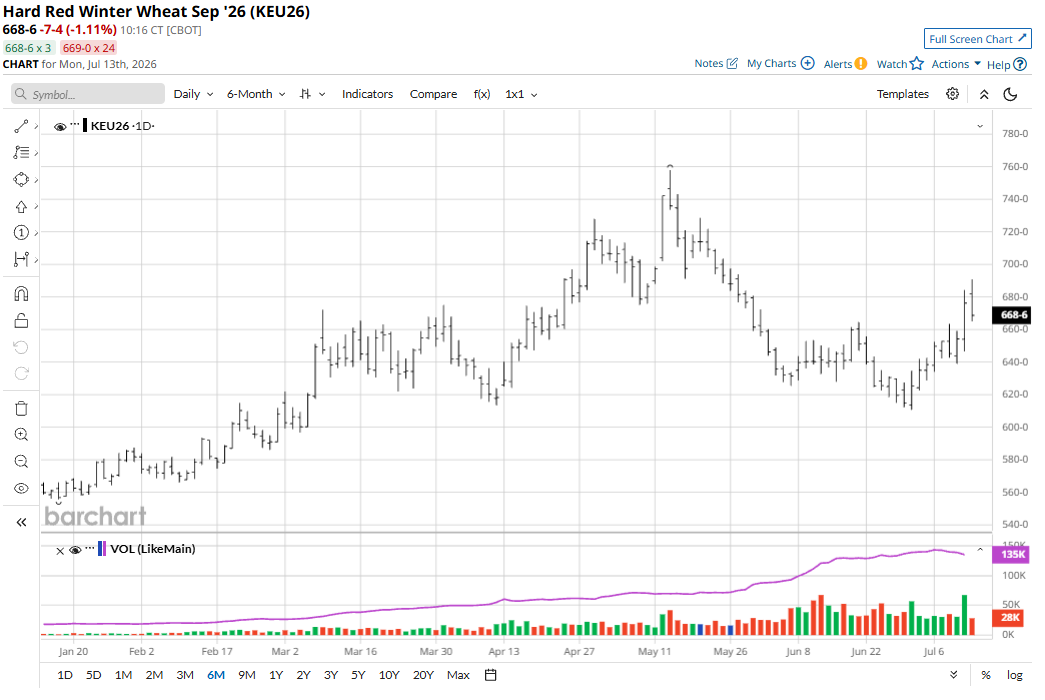

December corn (ZCZ26) futures on Friday rose 9 cents to $4.61 and for the week were up 19 1/2 cents. November soybeans (ZSX26) on Friday rose 9 1/4 cents to $11.90 3/4 and for the week gained 43 cents. September soft red winter (SRW) (ZWU26) wheat futures rallied 20 1/2 cents to $6.40 1/4, hit a six-week high, and for the week were up 40 1/2 cents. September hard red winter (HRW) wheat (KEU26) futures rose 22 cents to $6.76 1/4, also hit a six-week high, and for the week gained 37 3/4 cents.

Corn Bulls Gain Confidence as U.S. Midwest Weather Turns Hotter, Drier

The corn market bulls rebounded smartly on Friday to gain fresh technical momentum after shaky trading days last Wednesday and Thursday.

Last Friday’s USDA monthly supply and demand report showed no bearish surprises for the corn market, and bulls were also encouraged by that. The USDA cut its old-crop corn carryover by 125 million bushels from last month while stocks were 59 million bushels below the average pre-report trade estimate. The USDA made no change on the supply side of the old-crop balance sheet. The agency put the national average on-farm cash corn price for 2025-26 at $4.15, steady from last month. U.S. corn production for 2026/27 is up fractionally. The average U.S. corn yield is unchanged at 183.0 bushels per acre.

While much of the U.S. Midwest will see favorable conditions for corn pollination for at least the next week, traders will be eyeing the potential for a heat dome building over the Rockies that may expand farther east to impact the western Corn Belt, some of which is already too dry.

The coming heat and dryness may impact eastern South Dakota corn regions. Meantime, a heat wave over much of Europe is baking crops there, especially in France. The grain market is becoming increasingly concerned regarding the weather/grain situation in Europe.

Domestic demand for corn remains robust, driven by ethanol and livestock feed, while South American competition — particularly advancing safrinha harvests in Brazil — has pressured U.S. corn exports.

China Finally Stepping up and Buying U.S. Soybeans

The soybean complex futures rallied last week on confirmation of China purchases of U.S. soybeans. The USDA Friday morning reported daily sales of 264,000 MT of U.S. soybeans to China during 2026-27. Earlier last week, China also booked hefty quantities of U.S. soybeans, major news outlets reported.

The USDA in its supply and demand report Friday reported just a slight rise in its U.S. soybean production estimate from last month. The agency put its old-crop U.S. soybean carryover estimate down 10 million bu. from June (at 330 million) and that is 7 million bu. below the average pre-report trade estimate. USDA made no change to the old-crop supply. The agency put the 2025-26 national average on-farm cash bean price at $10.40, steady from last month.

Renewed Middle East tensions and global weather concerns have also boosted soyoil demand, reinforcing biofuel importance and supporting the soybean futures complex.

August is arguably the most important growing month for most of the U.S. soybean crop. That means there is still time for a weather-market scare to pop up in soybeans. Focus will also be on the annual Pro Farmer crop tour that occurs in late August.

Wheat Gets a Double-Barrel Shot of Bullish News

The winter wheat futures markets last week rallied on escalating tensions between Russia and Ukraine that have prompted talk of shipping disruptions in the Sea of Azov. Ukraine reportedly struck several Russian tankers in that sea, which is connected to the Black Sea.

Friday’s monthly USDA report also leaned price-friendly for wheat. The agency’s first U.S. all-wheat production estimate fell 7 million bu. from the June projection but was 1 million bu. higher than analysts expected. USDA estimated the other U.S. spring wheat yield at 52.3 bu. per acre, which would be the second highest yield on record. USDA put the national average on-farm cash wheat price for 2026-27 at $5.06, up a penny from last month.

Scattered showers and thunderstorms in the U.S. Midwest recently and those expected in the near term will slow winter wheat crop maturation and harvest progress, although some fieldwork will advance. Drier weather is likely this next week.

Export demand for U.S. SRW wheat will remain a market focus, with abundant global supplies and harvest progress in key growing regions. HRW sees its tight domestic balance sheet and renewed geopolitical tensions providing a bullish undertone.

Let me know what you think. I enjoy hearing from my valued Barchart readers all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)