With a market cap of $109.5 billion, Howmet Aerospace Inc. (HWM) is a global leader in advanced engineered solutions for the aerospace, defense, gas turbine, and commercial transportation industries. The company specializes in mission-critical engine components, fastening systems, structural airframe components, and forged aluminum wheels, leveraging its extensive patent portfolio to deliver lighter, more fuel-efficient, and lower-carbon technologies.

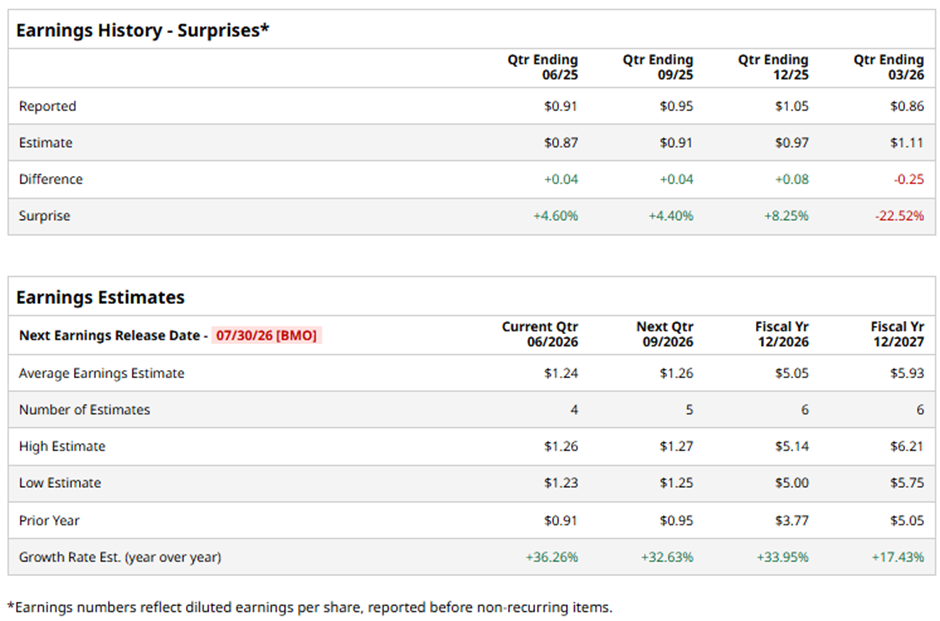

The Pittsburgh, Pennsylvania-based company is expected to release its fiscal Q2 2026 results before the market opens on Thursday, Jul. 30. Ahead of this event, analysts project HWM to report an EPS of $1.24, a 36.3% growth from $0.91 in the year-ago quarter. The company has exceeded Wall Street's bottom-line estimates in three of the last four quarters while missing on another occasion.

For fiscal 2026, analysts forecast the maker of engineered products to post EPS of $5.05, up nearly 34% from $3.77 in fiscal 2025.

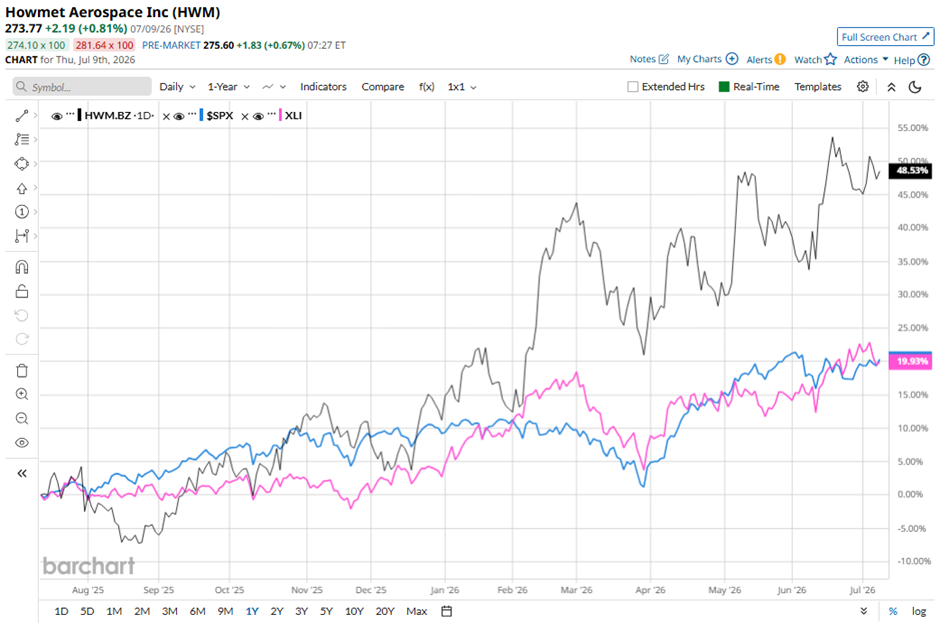

HWM stock has climbed 50.9% over the past 52 weeks, significantly outperforming the broader S&P 500 Index's ($SPX) 20.4% return and the State Street Industrial Select Sector SPDR ETF's (XLI) 20.8% gain over the same period.

Shares of Howmet Aerospace rose 6.3% on May 7 after the company reported stronger-than-expected Q1 2026 results, with revenue increasing 19% year-over-year to $2.31 billion and adjusted EPS of $1.22, both exceeding analyst estimates. Strong demand in commercial aerospace and gas turbines drove profitability higher, with operating income surging 52% to $753 million, adjusted EBITDA rising 32% to $740 million, and EBITDA margin expanding 320 basis points to 32%, while free cash flow more than doubled to $359 million.

Investors were further encouraged by management’s raised outlook, including full-year revenue guidance of $9.65 billion and adjusted EPS of $4.94, both above Wall Street expectations, reflecting confidence in sustained aerospace demand and production growth.

Analysts' consensus view on HWM stock is bullish, with an overall "Strong Buy" rating. Among 23 analysts covering the stock, 18 suggest a "Strong Buy," one gives a "Moderate Buy," and four provide a "Hold" rating. The average analyst price target is $307.90, suggesting a potential upside of 12.5% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)