/Bolts%20washers%20and%20nuts%20industrial%20hardware%20by%20Alpar%20via%20Adobe%20Stock.jpeg)

Based in Northbrook, Illinois, IDEX Corporation (IEX) is a diversified industrial manufacturer. Backed by a market cap of nearly $16.4 billion, the company develops, manufactures, and distributes precision fluidics, pumps, valves, sealing solutions, medical devices, optical components, laboratory equipment, and firefighting and rescue systems.

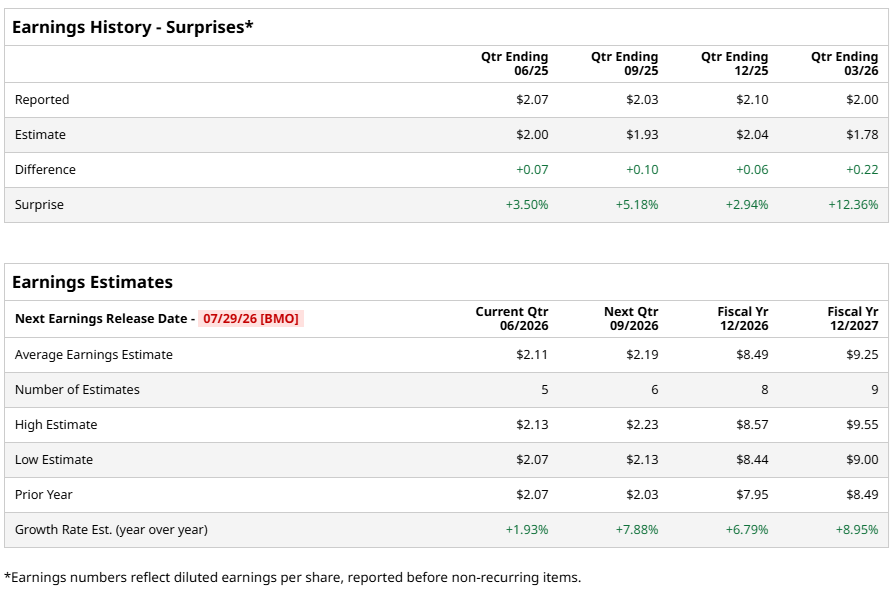

IDEX Corporation is scheduled to release its second quarter FY2026 results on Wednesday, July 29, before the market opens. Wall Street expects the company to deliver diluted EPS of $2.11, marking a 1.93% increase from $2.07 in the same quarter last year. The target hardly looks like a mountain to climb because IDEX has comfortably cleared analysts' earnings estimates in each of the past four quarters.

Analysts expect the company to keep the ball rolling well beyond the upcoming quarter. They forecast FY2026 diluted EPS of $8.49, reflecting 6.8% year-over-year growth. They also expect FY2027 diluted EPS to reach $9.25, representing another 9% increase from the previous year.

On the share price front, IEX stock has gained 19.7% over the past 52 weeks, falling just short of the broader S&P 500 Index ($SPX), which advanced 20.2% during the same period. This year tells a different story. IEX stock has climbed 22.7% in 2026, leaving the benchmark index's 9.3% year-to-date (YTD) gain in the rearview mirror.

The comparison with its own sector paints a similar picture. IEX stock trailed the State Street Industrial Select Sector SPDR ETF (XLI), which returned 21.2% over the past 52 weeks. However, IEX stock has turned the tables in 2026, comfortably ahead of XLI's 16.3% YTD advance.

On Wednesday, April 29, IDEX gave investors another reason to cheer as its stock climbed 5.8% intraday following its Q1 FY2026 earnings release. Revenue increased 8.9% year over year to $886.9 million, beating analysts' estimate of $847.4 million. Adjusted EPS rose 14.3% from the year-ago value to $2, ahead of Street’s estimates of $1.77.

Management said the quarter exceeded its own expectations, driven by strong execution across all segments. Orders also came in stronger than anticipated, rising 10% organically year over year. Health and Science Technologies led the charge as steady demand fueled high-value applications across data center, semiconductor, space, and defense markets throughout.

The strong performance has prompted management to raise its full-year outlook. It now expects organic sales growth of 3% to 4%, up from 1% to 2%, and adjusted diluted EPS of $8.35 to $8.55, up from $8.15 to $8.35. Q2 guidance calls for 3% to 4% organic sales growth and adjusted diluted EPS of $2.07 to $2.12.

Wall Street currently gives the stock an overall “Moderate Buy” rating. Among 14 analysts covering IDEX, seven recommend “Strong Buy,” one assigns a “Moderate Buy,” while six continue to recommend “Hold.”

Analysts also believe the rally has more room to run. The average price target of $240.36 points to a potential upside of 10.1%. Meanwhile, the Street-High target of $260 suggests a gain of 19.1% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)