/Microsoft%20logo%20on%20building%20by%20trazika%20via%20Pixabay.jpg)

Microsoft (MSFT) has had a rough time so far in 2026. Down 20% year-to-date (YTD), MSFT stock has been on the receiving end of the “AI replacing software” debate. Despite being the second-largest cloud services provider behind Amazon (AMZN) and investing heavily in AI, the company just hasn't gotten its fair share of recognition. While this apparent disparity in treatment has left many investors stumped, others have been slowly accumulating shares — and they may soon be rewarded for their patience.

Gil Luria, head of tech research at D.A. Davidson, recently called out the extreme valuation gaps among tech companies. Luria pointed out that stocks like Micron (MU) and Nvidia (NVDA) — trading at forward price-to-earnings (P/E) multiples of 13 times and 22 times, respectively — are priced as if the cycle has peaked and their earnings are set to normalize. Yet CPU stocks, which are one reason why memory stocks keep going up, are trading at forward P/E ratios many times higher.

The dynamic between two hyperscalers, Microsoft and Alphabet (GOOGL), is even more interesting. Just a year ago, Microsoft was trading at a trailing 12-month earnings multiple of 30 times while Alphabet was lingering at just 18 times. Today, Microsoft is closing in on a 23 times multiple, which Luria thinks is an overcorrection. Luria believes that Microsoft’s product portfolio is not only strong but is likely to stay relevant in the AI era, especially when the company itself is one of the biggest investors in artificial intelligence.

Currently, Microsoft is trading like a software company when it is investing to become an AI company. Sooner or later, this could change as the market realizes the software part isn’t going anywhere.

About Microsoft Stock

Microsoft is a multinational tech company that develops software, cloud computing services, devices, and AI solutions. Its product portfolio includes Windows, Microsoft 365, Xbox, LinkedIn, GitHub, Copilot, Dynamics, and Azure. Founded in 1975, the company is headquartered in Redmond, Washington, and is currently led by CEO Satya Nadella.

Over the last 12 months, MSFT stock has fallen 22%, significantly underperforming the S&P 500’s ($SPX) roughly 20% gain during the same period. In the past month alone, the stock has seen a 7% fall driven by a securities fraud class-action lawsuit, Xbox price hikes, and quantum computing credibility concerns. MSFT stock has seen a small recovery in the past five days following a bullish note from Morgan Stanley but remains well below its 52-week high of $555.45.

Microsoft’s declining stock price has created a valuation that's difficult to ignore. The forward P/E of 20.2 times is more than 30% cheaper than the company’s own five-year average, while the forward price-to-sales (P/S) ratio of 9 times is also cheaper. Both metrics suggest Microsoft is trading at a considerable discount to its historic norms.

The EPS growth trajectory makes that discount look even more attractive, with analysts expecting growth of 23% in fiscal 2026 followed by 15% growth in fiscal 2027. Net debt of $47.2 billion may feel significant, but for a company with a $2.9 trillion market capitalization and $627 billion in committed revenue, this doesn’t seem worrisome, either. Concerns for investors come from Microsoft's $190 billion in capital expenditures for 2026 and the ongoing class-action lawsuit. However, with MSFT stock trading at a discount despite the consistent earnings growth, most analysts believe the market may be overreacting to capex concerns.

Microsoft Reports Earnings

Microsoft reported its third-quarter fiscal 2026 earnings on April 29, beating analyst estimates on both key metrics. Revenue increased 18% year-over-year (YOY) to $82.9 billion compared to the $81.4 billion consensus. Diluted EPS also saw a healthy 23% YOY increase to $4.27 versus the $4.06 consensus estimate. CFO Amy Hood credited growing demand for Microsoft Cloud as a key driver, with revenue, EPS, and operating income exceeding management’s own expectations. Microsoft Cloud revenue grew 29% to $54.5 billion, primarily due to Azure. The company’s commercial remaining performance obligation increased 99% to a colossal $627 billion. Additionally, CEO Satya Nadella highlighted annual AI revenue increasing 123% to $37 billion.

For Q4, Microsoft guided revenue of $86.7 billion to $87.8 billion, representing 13% to 15% YOY growth. The company expects Azure cloud momentum to continue. Microsoft is also planning heavy investments, with Hood confirming capital expenditures will reach approximately $190 billion in 2026. The CFO also acknowledged that supply constraints are expected to last through at least the end of 2026.

Despite beating estimates across key metrics, MSFT stock fell 4% after the earnings report.

What Are Analysts Saying About Microsoft Stock?

Following the report, Citi analyst Tyler Radke maintained a “Buy” rating for MSFT stock with a price target of $620. The analyst cited Microsoft’s growing AI independence beyond OpenAI and rising demand from large enterprises using AI on its platforms as reasons for the positive outlook. Wells Fargo and Bernstein analysts also have bullish views, maintaining positive ratings with price targets of $650 and $646, respectively.

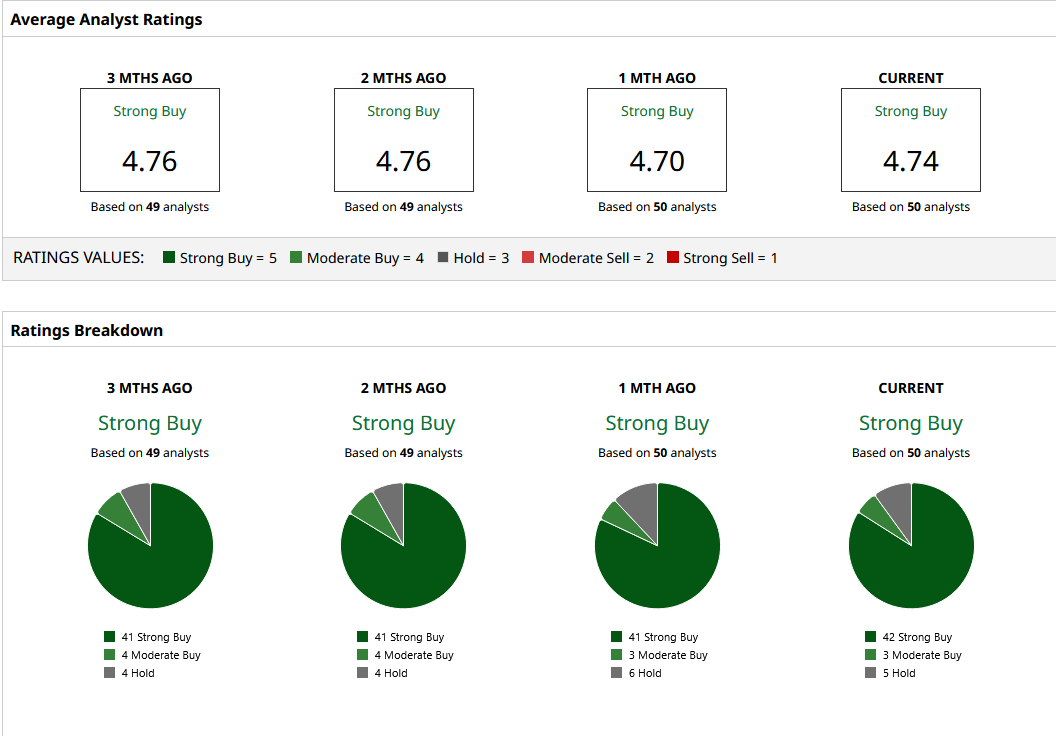

Based on 50 Wall Street analysts, Microsoft holds a consensus “Strong Buy” rating. The mean price target of $552.27 indicates potential upside of 43% from here. Out of the 50 analysts with coverage, no one has a “Sell” rating, with even the lowest target of $400 pointing to 4% potential upside from current levels. The estimates suggest that Microsoft's fall in the past year has made it undervalued, making now an attractive entry point for investors.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)