/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

Microsoft (MSFT) reported a strong third quarter, driven by growth in its cloud and AI businesses. By all measures, MSFT's Q3 results should have pushed the stock higher. Instead, shares dipped about 1.8% in pre-market trading after the earnings release and are down about 5% in afternoon trading today.

The lukewarm market reaction stems from higher spending. Microsoft is investing heavily in AI infrastructure to capture future growth, and those costs are putting pressure on margins in the near term. At the same time, management expects only a modest pickup in Azure (its cloud computing platform) growth, even with this increased investment.

The company plans to spend $190 billion on capital expenditures in 2026, including $25 billion related to higher component costs. MSFT’s management remains confident these investments will pay off, citing strong demand, rising product usage, and ongoing efficiency improvements across its platform. However, despite accelerating efforts to expand capacity, Microsoft expects supply constraints to persist through at least 2026, which could restrict Azure’s growth rate.

Despite the market’s muted reaction, Microsoft’s core businesses remain strong. Its cloud and AI segments are positioned for meaningful expansion over time. Moreover, MSFT expects Azure’s growth to show modest acceleration in the second half of 2026 compared to the first half. This is due to current supply constraints, which are temporary and expected to ease over time, boosting Azure’s growth rate.

Cloud and AI to Power MSFT Stock Higher

Microsoft is positioned to deliver strong growth in the coming quarters, driven by the sustained strong demand for its cloud infrastructure and AI offerings. In the most recent quarter, the company reported revenue of $82.9 billion, up 18% year-over-year (YoY). The top line was driven by Microsoft Cloud, which generated $54.5 billion in revenue, up 29%.

Microsoft’s commercial remaining performance obligation (RPO) increased 99% to $627 billion, signaling solid growth ahead. Notably, about one-quarter of this backlog is expected to convert into revenue over the next 12 months, growing 39% YoY. Meanwhile, longer-dated commitments surged 138%, supporting multi-year growth.

Microsoft’s AI business reached an annual revenue run rate exceeding $37 billion, expanding 123% YoY. The Intelligent Cloud segment delivered $34.7 billion in revenue, up 30%. Within this segment, Azure and related cloud services grew 40%, driven by broad-based demand across industries and geographies. Importantly, management highlighted that demand continues to outstrip available capacity, suggesting a durable growth runway as infrastructure scales.

The company’s generative AI offerings, primarily Copilot, are gaining traction at an exceptional pace. Paid Copilot seats surpassed 20 million, with YoY growth of 250%. Enterprise adoption is deepening as well, with the number of customers deploying more than 50,000 seats quadrupling over the past year.

Looking ahead, Microsoft is expected to benefit from continued strength across its businesses. Microsoft anticipates sequential increases in net paid Copilot seat additions, which should further enhance average revenue per user.

In the Intelligent Cloud segment, revenue is expected to reach between $37.95 billion and $38.25 billion in Q4, implying growth of 27% to 28%. Azure growth is forecasted at 39% to 40% in constant currency.

While Microsoft’s top line will likely sustain solid growth momentum, cloud gross margin could come under pressure from continued investments in AI.

Despite potential margin compression, MSFT’s earnings growth is expected to remain solid. Analysts expect Microsoft to post earnings of $16.54 per share in fiscal 2026, up over 21% YoY. Moreover, its bottom line is projected to grow by 13.7% in fiscal 2027.

Overall, Microsoft’s Q3 performance and outlook reflect significant demand tailwinds, particularly in AI and cloud. While capacity constraints may temper near-term upside, the strong cloud backlog growth, solid momentum in the AI business, and growing enterprise adoption position the company for solid growth, likely pushing its stock price higher.

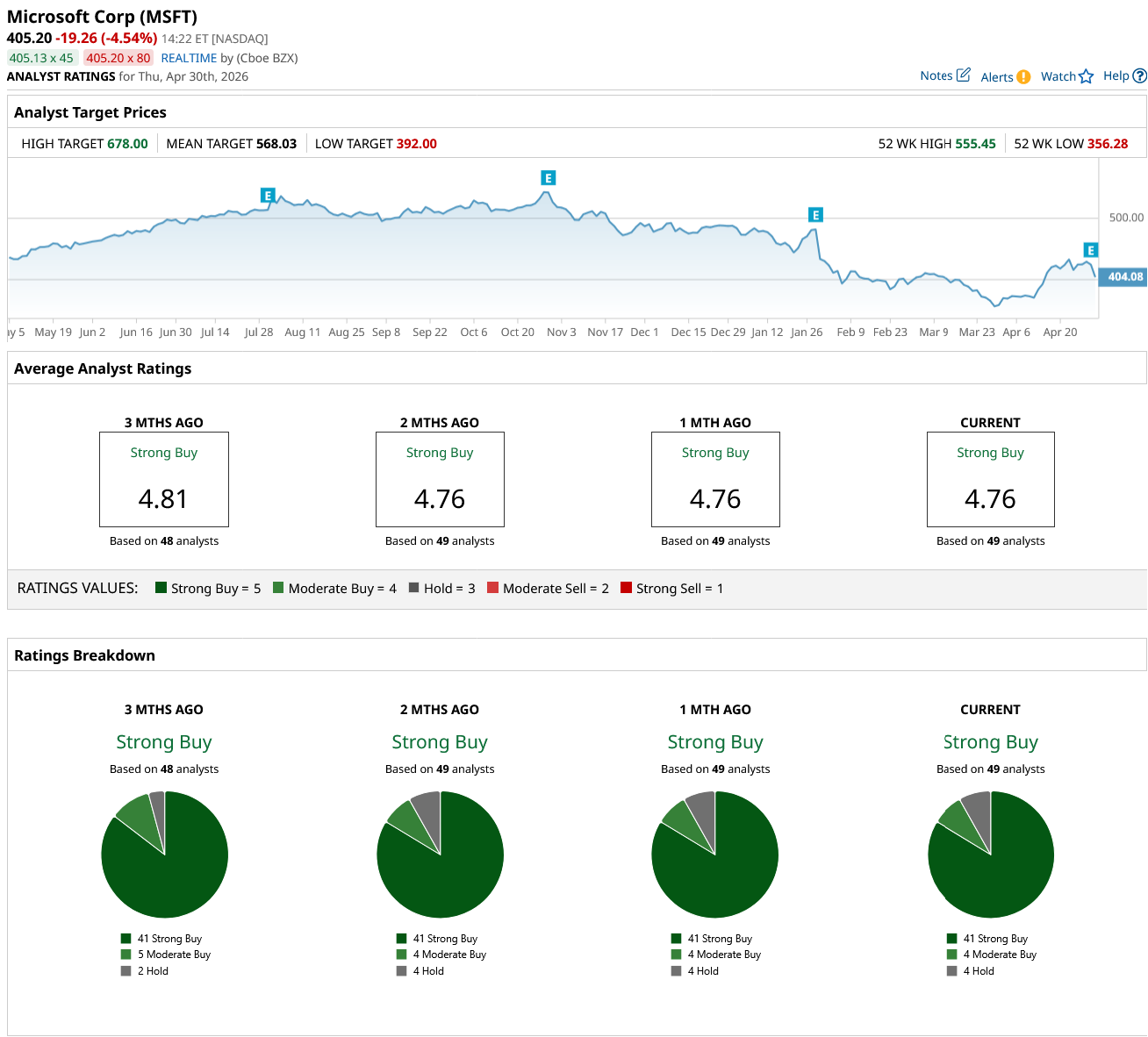

Analysts See 33% Upside for MSFT Stock

Wall Street sentiment toward Microsoft remains positive following its third-quarter earnings release, with analysts maintaining a “Strong Buy” consensus rating. This optimism reflects sustained operational momentum across the company’s core segments, particularly in cloud computing, AI, and enterprise software.

Analysts have an average 12-month price target of $568.03 for MSFT stock, implying approximately 33% upside from its April 29 closing price of $424.46.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.