/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

South Korean memory giant SK Hynix is expected to list its American Depositary Receipts (ADRs) in the U.S. under the ticker SKHY. Its debut is tentatively scheduled for Friday, July 10.

If all goes according to plan, the company will raise a staggering $29 billion. That would make it the largest ADR listing in recorded market history, comfortably eclipsing Alibaba’s (BABA) $21.8 billion New York debut back in 2014.

For investors who have been chasing memory makers like Micron (MU) to constant new all-time highs, easier U.S. exposure to SK Hynix sounds like a golden ticket.

I, however, have a conspiracy theory.

Market debuts are a sign that companies recognize that the window to raise tons of capital is closing. In fact, it is closing very quickly.

That would explain in part OpenAI’s likely decision to delay its IPO until sometime in 2027. OpenAI saw SpaceX (SPCX) debut into a market frenzy but then quickly falter.

That brings me to SK Hynix.

It appears to me that as with SpaceX, it has been the target of a feeding frenzy by ETF issuers to offer some sort of backdoor access to the stock as part of the memory trade. I’m starting to wonder if the word “memory” might soon be preceded by the word “distant” when it comes to what happened to this group of DRAM and NAND providers.

SK Hynix is one of the top holdings in the Roundhill Memory ETF (DRAM), which has been on a tear since its April 2, 2026 inception. Its current asset base is a whopping $21 billion!

SK Hynix’s own entrance into the U.S. market as an ADR, which is a vehicle which allows non-U.S. stocks to trade on U.S. exchanges via a share conversion mechanism, seems highly promotional. It is framed as an opportunity for U.S. capital to finally gain direct exposure to the crown jewel of high-bandwidth memory (HBM). After all, the company reportedly has a dominant 56% global revenue share in the specialized chips powering Nvidia’s (NVDA) AI accelerators.

Historically, U.S.-listed Micron has traded at a valuation premium relative to SK Hynix. This wasn’t because MU had superior margins. After all, SK Hynix reported a jaw-dropping 72% operating margin in Q1 2026. But simply put, MU was easier to access, and was part of U.S. indexes.

While this listing could narrow that valuation gap, the broader risk lies in the massive capital influx itself. SK Hynix explicitly stated that the $29.4 billion in proceeds will be deployed to aggressively expand production capacity and construct massive new fabrication facilities in South Korea.

The memory industry is very cyclical and commoditized, as traders found out last week when some of the industry leaders shed a notable chunk off of their stock prices. While the market is tightly undersupplied right now, funding a massive supply expansion at what could be the peak of a cycle is how market “accidents” happen. To be clear, this issuance means insiders who know their businesses best are aggressively selling new equity to an enthusiastic public, which is a classic signal that the cyclical peak may be much closer than the late-stage crowd believes.

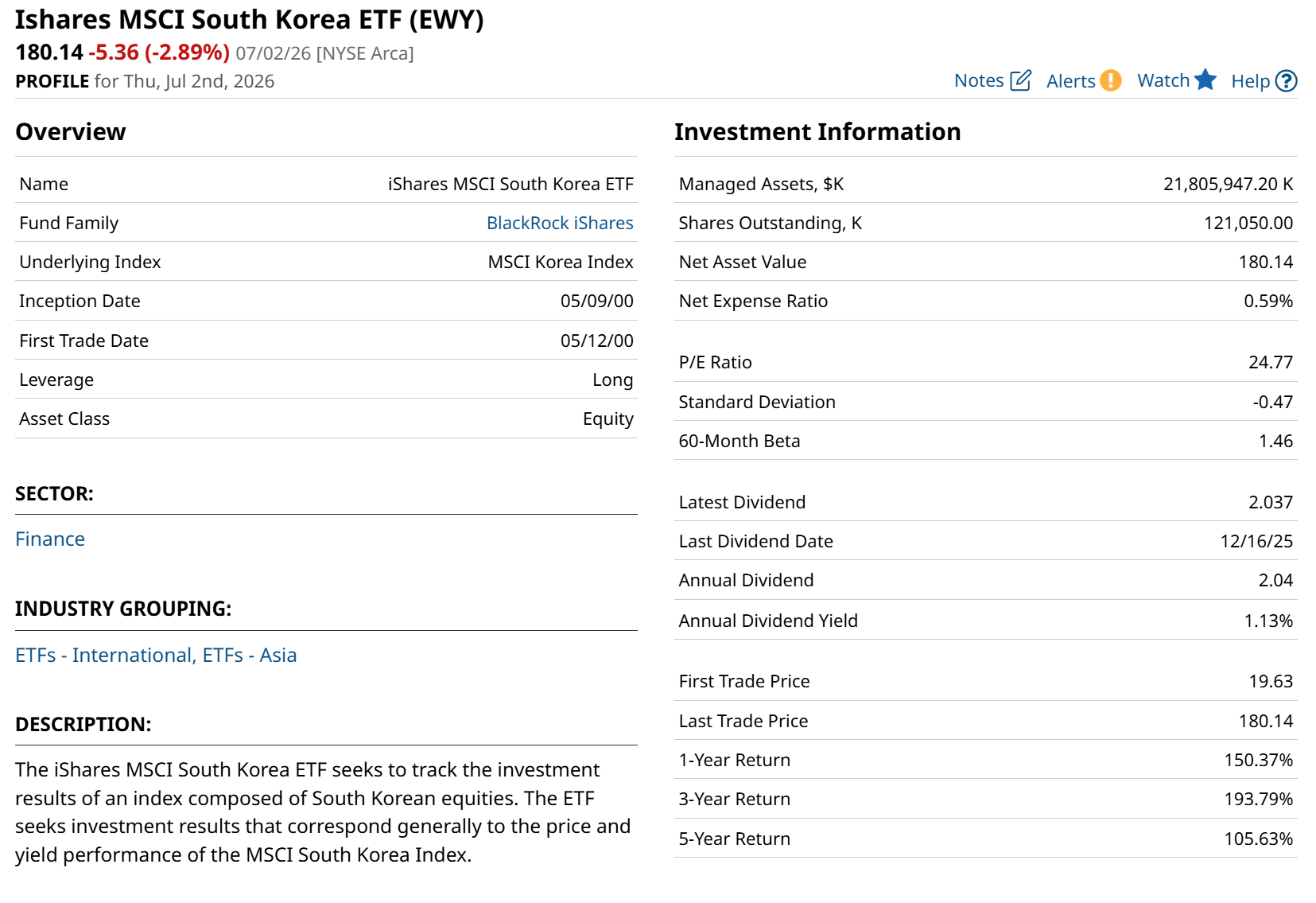

The way I’ve tracked SK Hynix has been through an ETF that invests not in memory specifically, but in companies based in South Korea. The iShares MSCI South Korea ETF (EWY) is, coincidentally, around the same size in assets as DRAM.

But EWY has been around for more than three months. How long? It debuted at the START of the dot-com bubble bust. Oh, the irony!

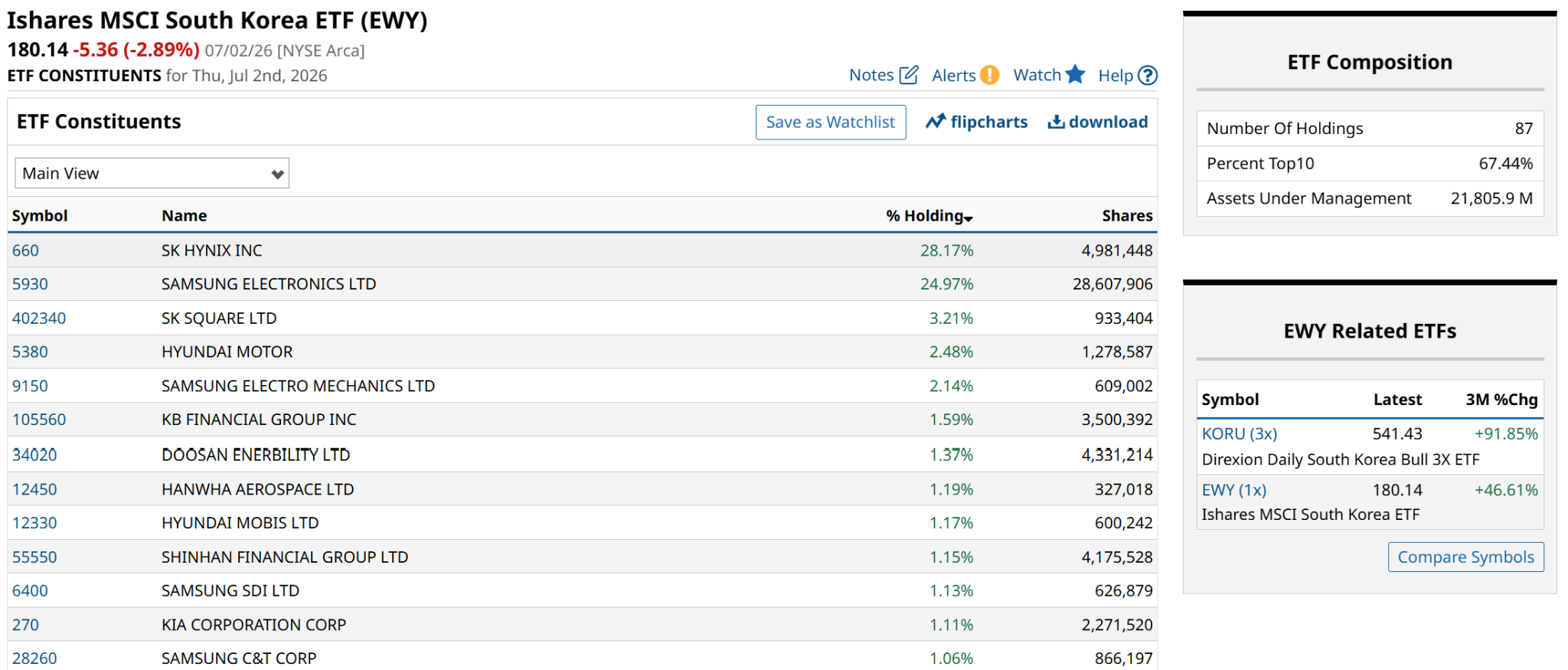

A quick look at EWY’s top holdings reveals our big guy, SK Hynix, with its market cap twin, the globally-known Samsung, at the top of the weightings. Those two stocks comprise a whopping 53% of EWY, and are thus about $1 out of every $2 invested in the South Korean stock market. At least as far as U.S. ETF investors are concerned.

This is naturally a big move for SK Hynix. The biggest stock market in the world, the one most companies prioritize getting listed on, is about to provide a 4-letter ticker symbol to a company better known as “660,” since the South Korean stock market assigns numerical codes instead of ticker symbols. What remains to be seen is if SKHY becomes a “four-letter word.”

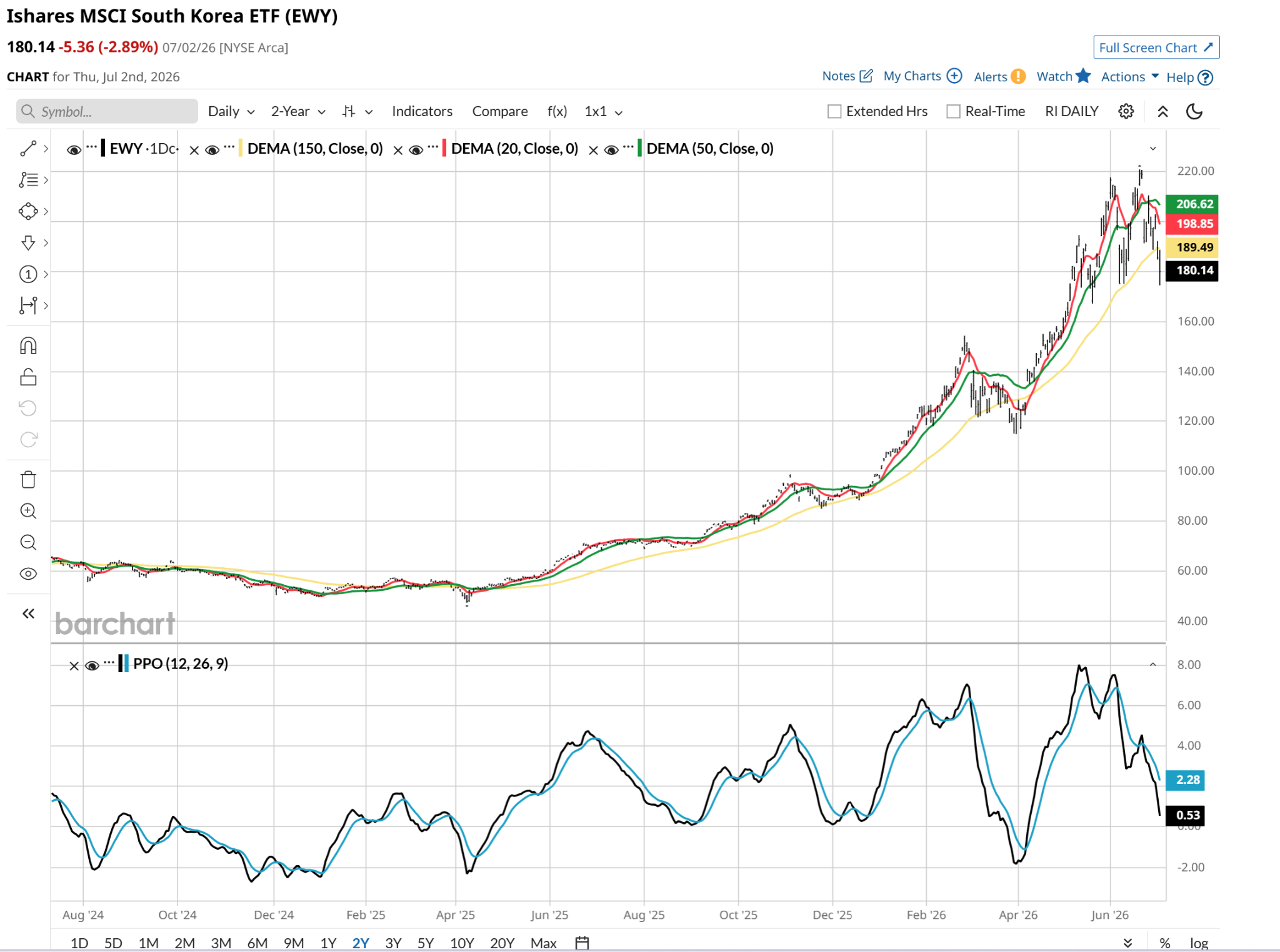

Since it is such a big driver of EWY, my path of least resistance to answer my own question is to chart it. And when I do, it appears to be arriving in the U.S. with the same type of “baggage” that has suddenly beset its U.S. memory industry peers.

That chart of EWY looks terrible. Never say never, but never have we seen a move like this in semis. Except, that is, for the top of the bubble in 2000.

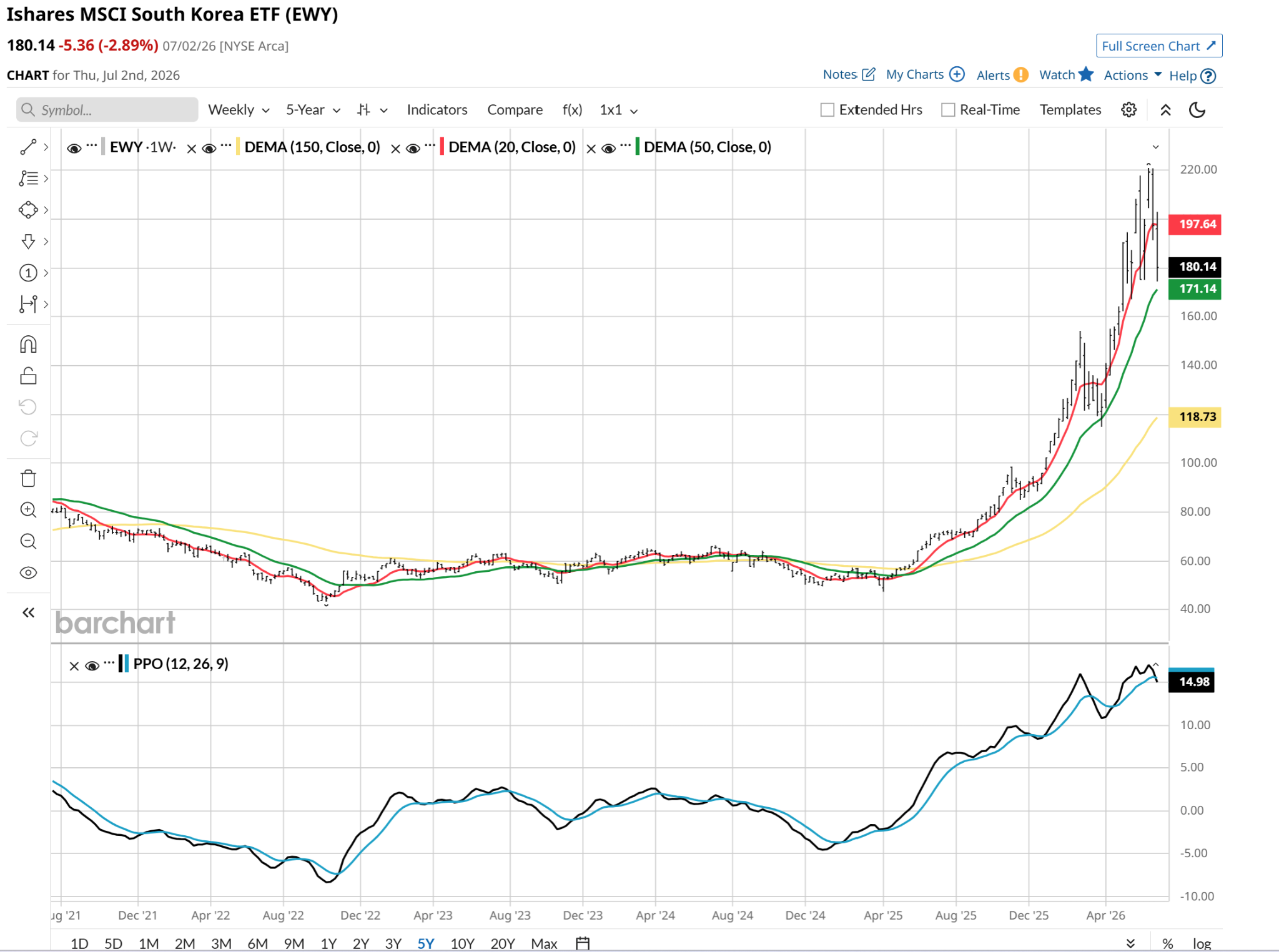

The weekly chart doesn’t offer investors any more hope. It is still not rolled over, but the percentage price oscillator (PPO) in the lower part of the chart is hinting at a more significant top.

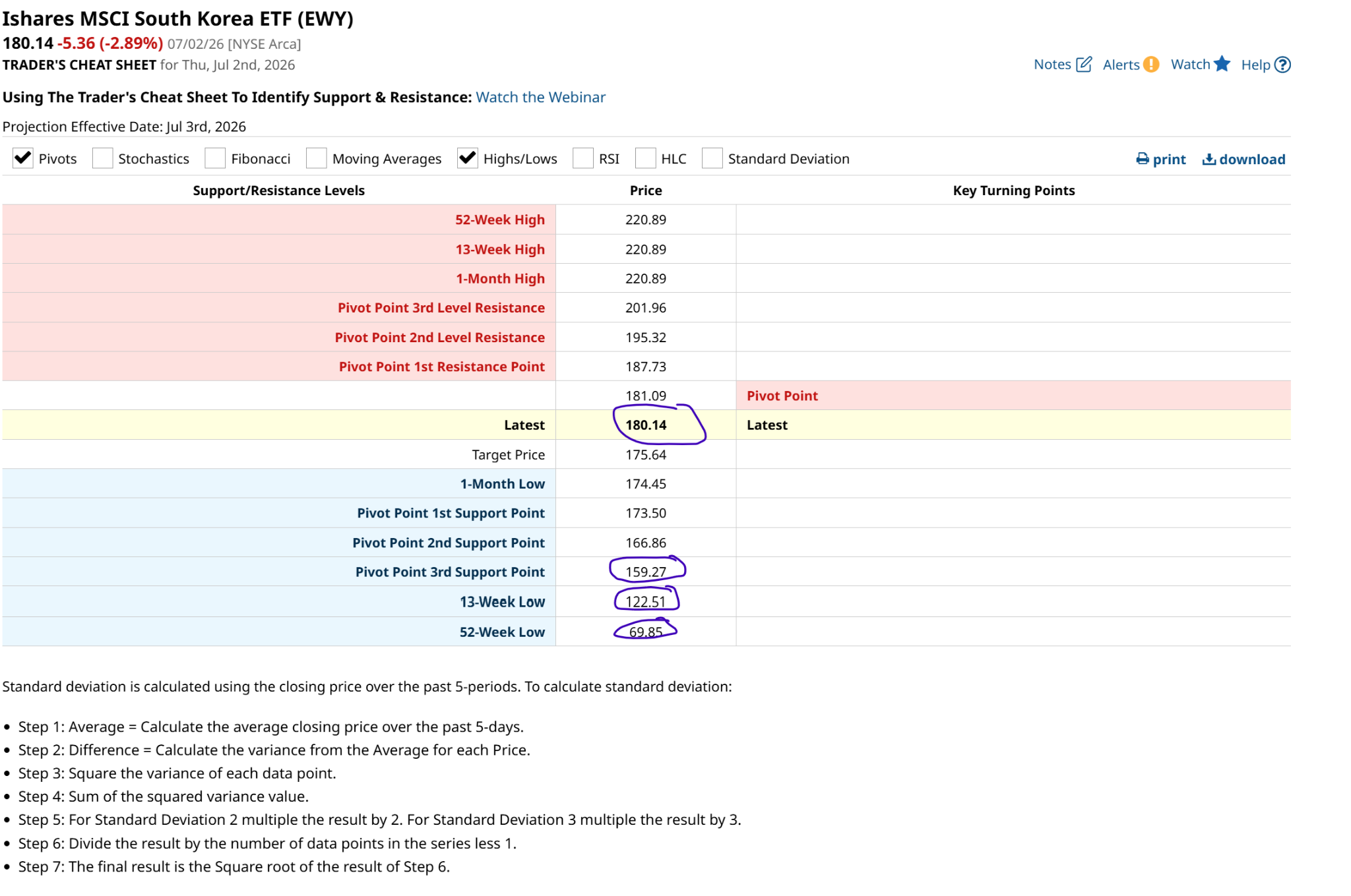

Look no further than the summary above, using Barchart’s Trader’s Cheat Sheet, which is designed to help us map out support and resistance levels. In this case, my sole focus is on support. And as you can see from what I circled above, there’s not much of it because the financial bleeding for EWY doesn’t stop very soon.

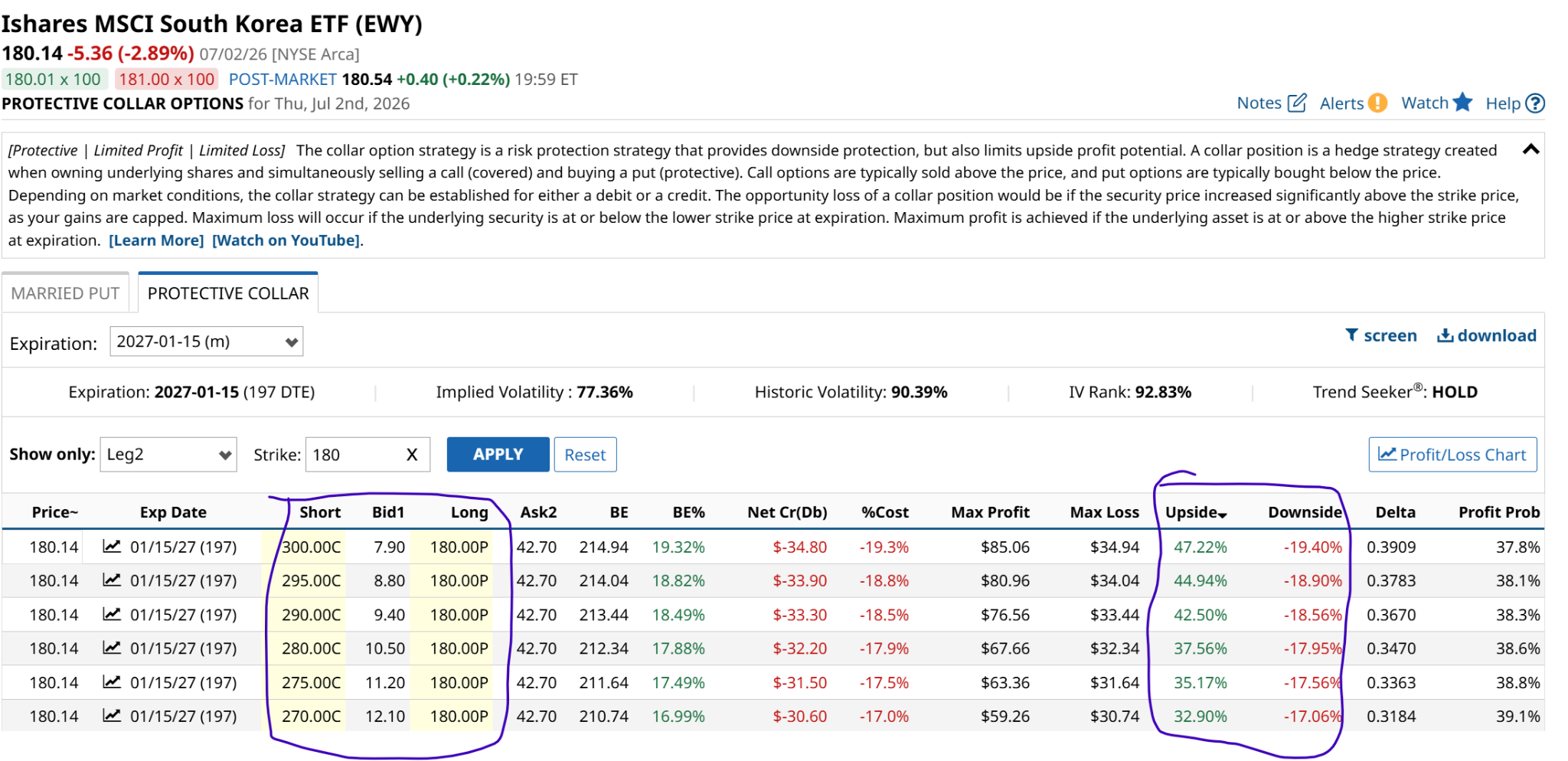

There are several ETFs you can use to profit from a decline in the memory industry, as well as emerging market inverse ETFs like the ProShares Short MSCI Emerging Markets ETF (EUM). But since EWY is also quite liquid, an option collar is another consideration. Here I show what it looks like out to the start of 2027, with the put strike fixed at $180. As we see, there’s 2:1 upside/downside potential across several call strikes. That’s not the best pricing I’ll ever see, but it at least reminds us that even a situation like this can be approached in hedged fashion.

Conspiracy theory, or valid theory? That’s not really the matter here. What is? A grossly overvalued stock, in a grossly overvalued, over-hyped stock market. That translates to a high emphasis on managing risk.

Rob Isbitts is a semi-retired CIO, former fiduciary investment advisor, and Barchart columnist. Check out his other work at ETFYourself.com (featuring the Fresh Charts weekly trading post), and ROAR.PiTrade.com, helping investors to better-manage their own portfolios.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)