/Abstract%20big%20data%20center%20storage%20with%20rack%20servers%20network%20by%20jamesteoh_art%20via%20Adobe%20Stock.jpeg)

OpenAI filed a confidential draft IPO with the U.S. Securities and Exchange Commission earlier this month, hired a financial team, and had Q3 or Q4 of this year firmly in its sights. That plan hit a wall fast.

A sharp pullback in Space Exploration Technologies (SPCX) share values, combined with growing investor skepticism over whether artificial intelligence (AI) companies can actually back up their lofty promises, forced OpenAI back to the drawing board, and Microsoft Corporation (MSFT) stock felt every bit of that turbulence.

The New York Times reports that OpenAI is now seriously considering a delay until 2027, largely because its advisors refuse to take the company public unless it walks in with a valuation above $1 trillion.

At $852 billion currently, OpenAI is close enough to smell it, but not close enough to bank on it, and even at the time of the original filing, the company made no promises about an imminent listing.

What makes this particularly uncomfortable for Microsoft is that Anthropic, OpenAI's chief rival, is already sitting at $965 billion and gearing up for its own IPO. Microsoft holds a significant stake in OpenAI and has woven its models into the very fabric of Azure, Copilot, and its enterprise software stack. So however OpenAI moves, Microsoft moves with it.

A shaky IPO at a deflated valuation could invite exactly the kind of shareholder noise that turns a strong partnership into a complicated one. Even so, MSFT stock gained 5.7% intraday on Friday, June 26, despite bleeding ground over the last month, making its path ahead worth examining much more carefully.

About Microsoft Stock

Headquartered in Redmond, Washington, Microsoft is one of the largest technology companies on the planet, running operations across cloud computing, workplace software, AI, gaming, search, and professional networking.

The company has a market cap of $2.77 trillion and owns some of the most recognizable franchises in tech, including Windows, Azure, Microsoft 365, Xbox, LinkedIn, GitHub, and Copilot, all of which serve millions of consumers and businesses worldwide every day.

But size has not kept the storm clouds away. Microsoft’s shares have fallen 25.68% over the past 52 weeks and dropped another 23.79% so far in 2026, with investors chewing their nails over AI spending levels and signs of slowing cloud growth.

On the valuation front, MSFT stock is currently trading at 22.18 times forward adjusted price-to-earnings Non-GAAP, which is a discount to both the industry benchmark and the company's own five-year average multiple. That discount takes a little sting out of the drawdown.

Furthermore, Microsoft has raised its dividend for 21 consecutive years and now pays $3.64 per share annually, translating to a yield of 0.98%. The next payment of $0.91 per share is scheduled to go out on Sept. 10 to shareholders of record as of Aug. 20.

Microsoft Surpasses Q3 Earnings

Microsoft dropped its Q3 FY2026 results on April 29 and cleared Wall Street's bar with room to spare. Revenue climbed 18.3% year-over-year (YOY) to $82.89 billion, beating analyst estimates of $81.39 billion. EPS jumped 23.4% from the year-ago figure to $4.27, topping the Street's $4.06 forecast.

Delving deeper, Microsoft Cloud crossed $54 billion in revenue, up 29% YOY. The company's AI business flexed even harder, with its annual revenue run rate surging past $37 billion, up 123% YOY.

The headline numbers came with a real bill attached. Gross margin slipped to 68% as Microsoft poured cash into AI infrastructure, and heavier AI product usage further squeezed margins. Efficiency gains across Azure and Microsoft 365 Commercial cloud picked up some of the slack.

Capital expenditures, together with finance leases, totaled a staggering $31.9 billion for the quarter. On the balance sheet, cash and cash equivalents stood at $32.1 billion as of March 31, up from $30.2 billion as of June 30, 2025.

Looking forward, management has guided Q4 FY2026 revenue to $86.7 billion to $87.8 billion, indicating growth of 13% to 15%, and has flagged plans to push capital spending above $40 billion as the company races to bring more capacity online.

Capital expenditures for the full CY2026 are expected to hit roughly $190 billion, with soaring memory costs doing a fair bit of the damage. Nearly $25 billion of that figure ties directly to higher component pricing.

On the earnings side, analysts expect Q4 FY2026 EPS to rise 15.3% YOY to $4.21. The full-year FY2026 bottom line could jump 22.9% from the prior year to $16.76, and FY2027 might deliver another 15% climb to $19.28.

What Do Analysts Expect for Microsoft Stock?

Despite the volatile stock performance and the potential postponement of the OpenAI IPO, Wall Street is not losing its nerve on Microsoft.

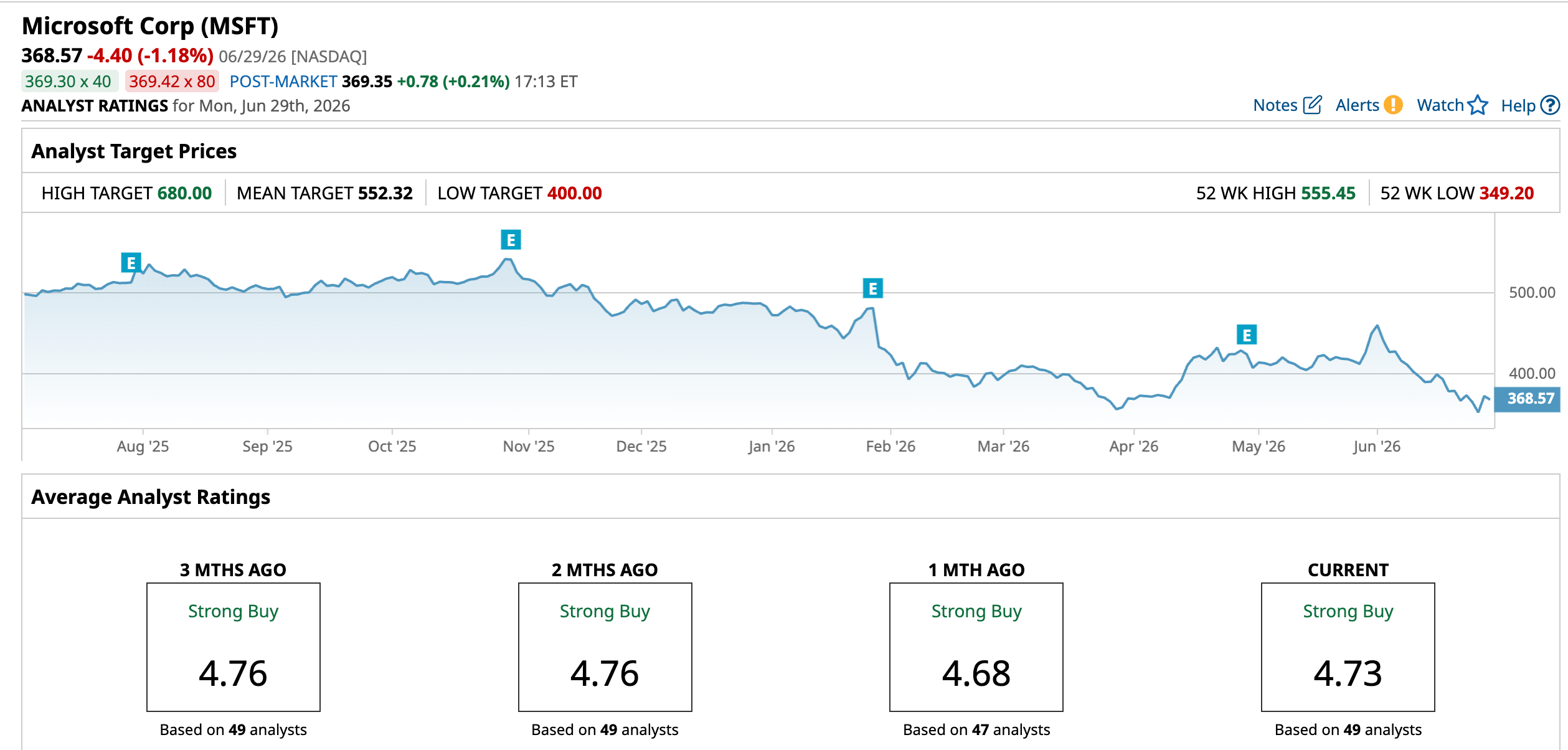

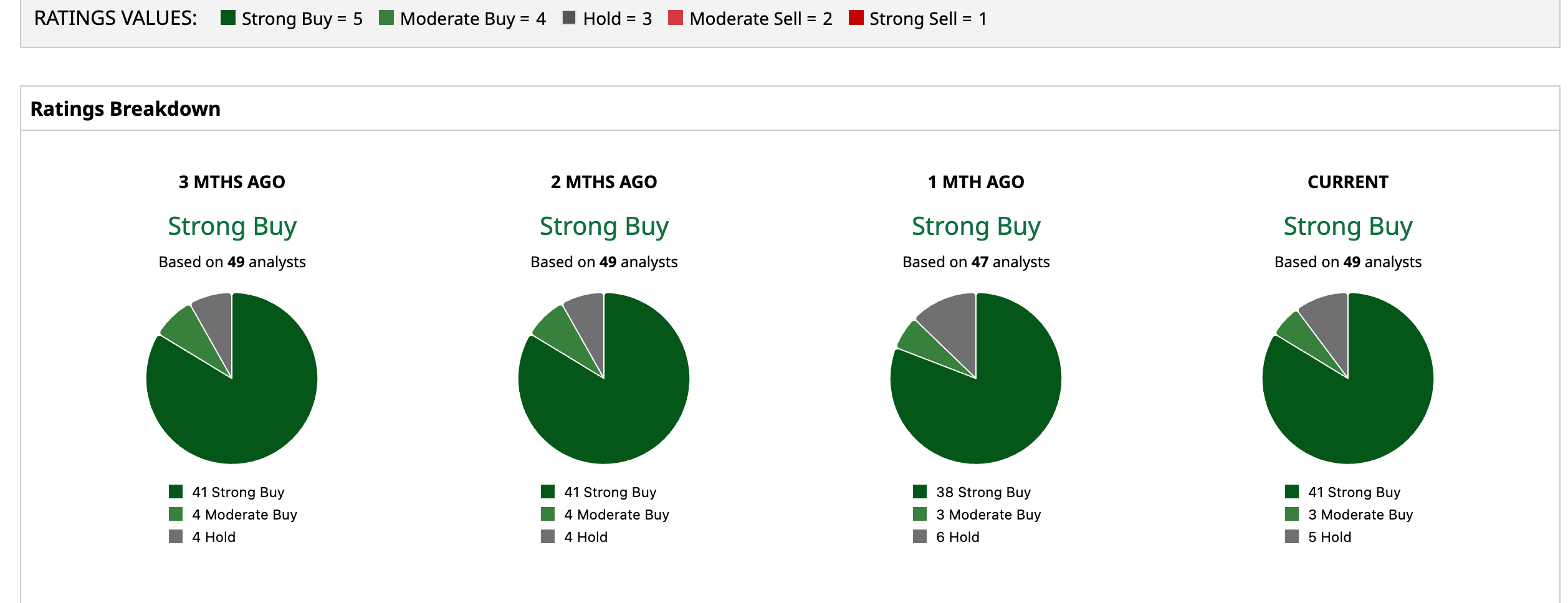

Its stock carries an overall rating of "Strong Buy" from the 49 analysts covering it. Among those, 41 rate it a "Strong Buy," three call it a "Moderate Buy," and five prefer to sit with a "Hold."

The average price target of $552.32 represents potential upside of 49.9%. Meanwhile, the Street-High target of $680 implies an 84.5% gain from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)