/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)

Headquartered in Marlborough, Massachusetts, Boston Scientific Corporation (BSX) is a global medical technology company that develops and sells devices used in minimally invasive procedures to diagnose and treat a wide range of health conditions.

With a market cap of approximately $63.4 billion, the company's products include devices for heart care, such as pacemakers and monitoring systems, as well as tools for treating digestive, urinary, neurological, and vascular disorders, as well as certain cancer-related treatments.

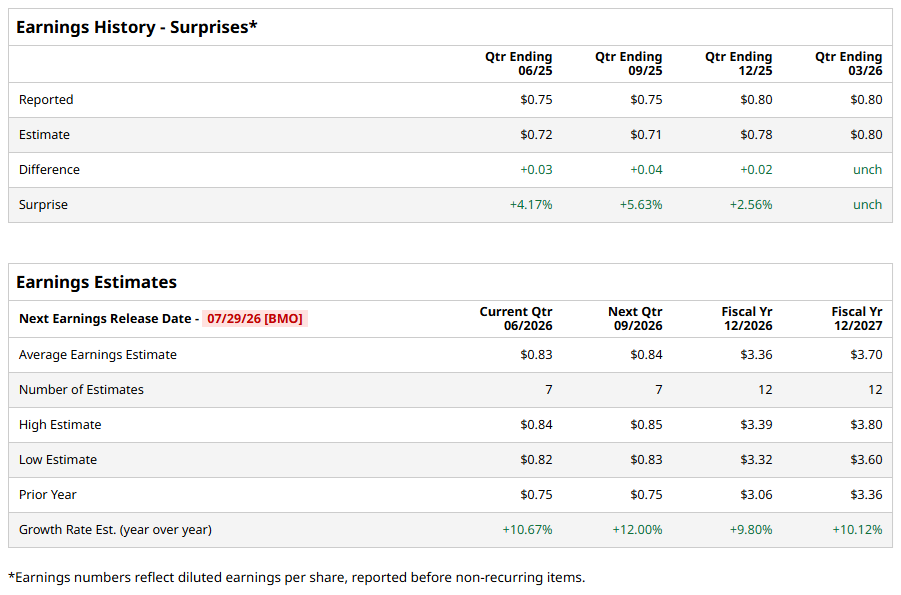

The company is now approaching its fiscal 2026 second-quarter earnings report, set to land on Wednesday, July 29, before the opening bell. Wall Street expects Boston Scientific to post diluted EPS of $0.83, marking a 10.7% gain from the $0.75 the company posted in the same quarter last year. The company also cleared the bar on EPS estimates in each of the last four quarters, which is impressive.

Analysts are keeping their eyes further down the runway, too. They forecast full fiscal 2026 diluted EPS of $3.36, which reflects a 9.8% year-over-year gain. The outlook only brightens from there, with full-year 2027 diluted EPS projected to climb to $3.70, representing a 10.1% increase from the prior year.

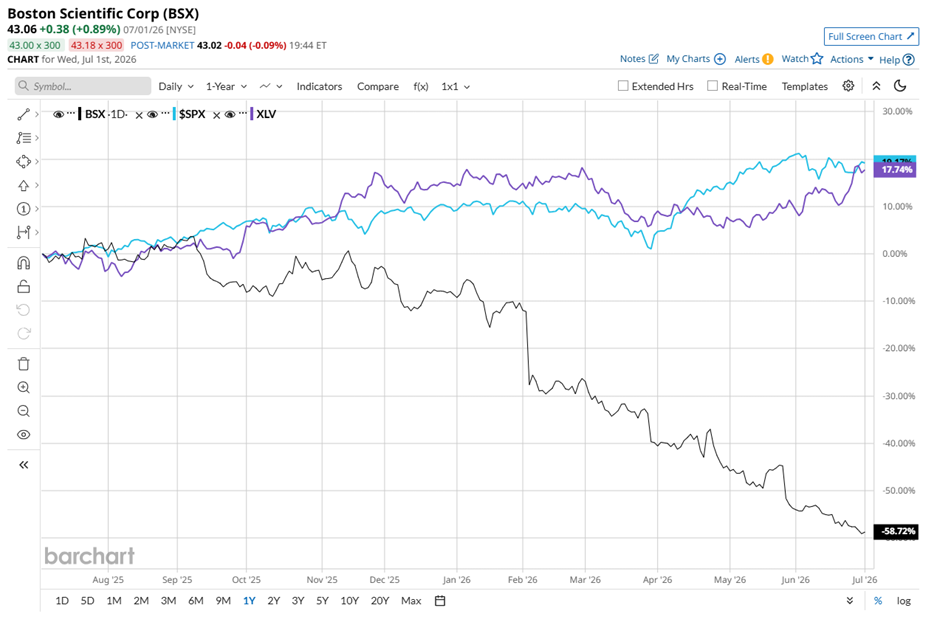

However, the stock chart tells a much bumpier story. Over the last 52 weeks, Boston Scientific’s shares declined 58.9%, falling well behind the broader S&P 500 Index ($SPX), which gained 20.7% over the same stretch. The pain has carried straight into 2026, with BSX stock plummeting nearly 54.8% on a year-to-date (YTD) basis while the benchmark index notched a 9.3% gain.

Sector peers tell the same tale. The State Street Health Care Select Sector SPDR ETF (XLV) returned 16.7% over the past 52 weeks and gained 3.1% in 2026, once again leaving Boston Scientific trailing the pack.

Still, the stock found a rare bright spot on Wednesday, April 22, when shares surged nearly 9% after the company reported Q1 FY2026 earnings. Revenue climbed 11.6% year over year to $5.20 billion, sailing past analyst estimates of $5.18 billion. Adjusted EPS rose 6.7% from the year-ago figure to land at $0.80, edging out analyst estimates of $0.79.

Broad-based demand across Boston Scientific's core franchises fueled that growth, with Cardiovascular and MedSurg leading the charge and electrophysiology, Watchman, neuromodulation, and interventional oncology all pulling their weight. New product launches, steady progress in clinical trials, and the Valencia acquisition each added fuel to the fire.

Looking ahead, for Q2 FY2026, Boston Scientific estimates net sales growth versus the prior-year period to be between 5.5% and 7.5% on a reported basis and between 5% and 7% on an organic basis. The company also estimates adjusted EPS, excluding certain charges and credits, to fall between $0.82 and $0.84.

Wall Street, for its part, is singing a largely positive tune about the stock. Boston Scientific currently holds a "Strong Buy" overall rating, with 21 out of 29 analysts calling it a "Strong Buy," four tagging it a "Moderate Buy," three sitting on the fence with a "Hold," and one lone holdout labeling it a "Strong Sell."

To that end, the average price target of $74 represents potential upside of 71.9%. Meanwhile, the Street-High target of $106 suggests a gain of 146.2% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)