/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

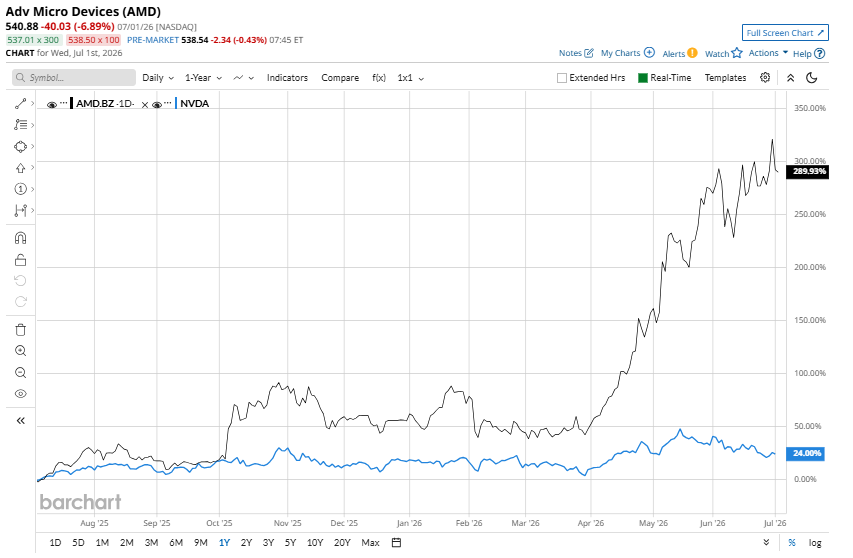

Advanced Micro Devices (AMD) has been one of the top performers in the S&P 500 ($SPX) during the first half of 2026. Specifically, AMD stock has surged 142% year-to-date (YTD), outperforming Nvidia (NVDA) stock's gain of just over 4% over the same period.

The rally has been driven by AMD's solid financial performance over the past several quarters, led by its growing share in the artificial intelligence (AI) infrastructure space. Demand for its Instinct GPU accelerators remains solid, driven by a diversified customer base and ongoing AI infrastructure spending.

AMD is also likely to benefit from strong demand for its high-performance EPYC processors as AI workloads evolve from model training to inference and emerging agentic AI applications. These workloads require greater compute capacity, positioning AMD to capitalize on growth across both GPUs and CPUs.

While these tailwinds indicate strong growth ahead, AMD stock is not cheap. Following its sharp run-up, AMD now trades at 87.9 times forward earnings, a substantial premium to Nvidia's forward price-to-earnings (P/E) ratio of about 22.7 times.

With this backdrop, here’s what investors can expect next for AMD stock.

AMD’s Growth Isn’t Slowing Down

AMD's valuation appears high, but the company's solid execution over the past several quarters and long-term growth prospects suggest that the higher multiple is warranted. The company continues to gain share in AI accelerators while its CPU business has significant room to expand. On top of that, AMD projects robust growth over the next three to five years, which could drive earnings high enough to support its current valuation.

AMD’s latest quarterly results were solid, with revenue climbing 38% year-over-year (YOY) to $10.3 billion. At the same time, AMD’s earnings increased by more than 40% YOY. Strong profitability also translated into a sharp improvement in cash generation, with free cash flow more than tripling from the prior year.

AMD’s data-center business is growing rapidly, with revenue rising 57% in Q1 2026. The segment's growth reflects robust demand from enterprise customers and hyperscale cloud providers, both of which are investing aggressively in next-generation computing infrastructure. As AI adoption expands across industries, the need for high-performance processors and accelerators is rising, creating a favorable environment for AMD's product portfolio.

AMD's server CPU business has significant room to run. Sales jumped by more than 50% in Q1. Importantly, the company is seeing demand not only for its latest fifth-generation EPYC Turin chips but also for earlier generations.

Looking ahead, emerging workloads such as agentic AI and increasingly sophisticated AI models require substantially more computing power, expanding the addressable market for server processors. AMD projects server CPU revenue to grow more than 70% YOY in Q2 and believes demand will remain strong through 2027.

In the AI accelerators market, AMD’s Instinct GPUs are gaining traction as customers expand deployments for both AI training and inference workloads, while new customers increasingly view AMD as a credible alternative in a market still dominated by larger competitors. Although its AI business remains significantly smaller than Nvidia's, AMD is growing through higher adoption and new product launches.

AMD’s medium- to long-term growth targets support the investment case. The company foresees annual revenue growth above 35%, adjusted operating margins exceeding 35%, and adjusted EPS surpassing $20 within the next three to five years. That would represent a nearly fivefold increase from its adjusted EPS of $4.17 reported in fiscal 2025, reflecting a solid growth trajectory.

AMD Stock to Sustain Upward Trajectory

AMD stock has risen significantly. However, it still benefits from multiple growth drivers, including accelerating adoption of Instinct GPUs, rising demand for EPYC server CPUs, and the emergence of inference and agentic AI workloads, which provide a solid base for sustained earnings growth.

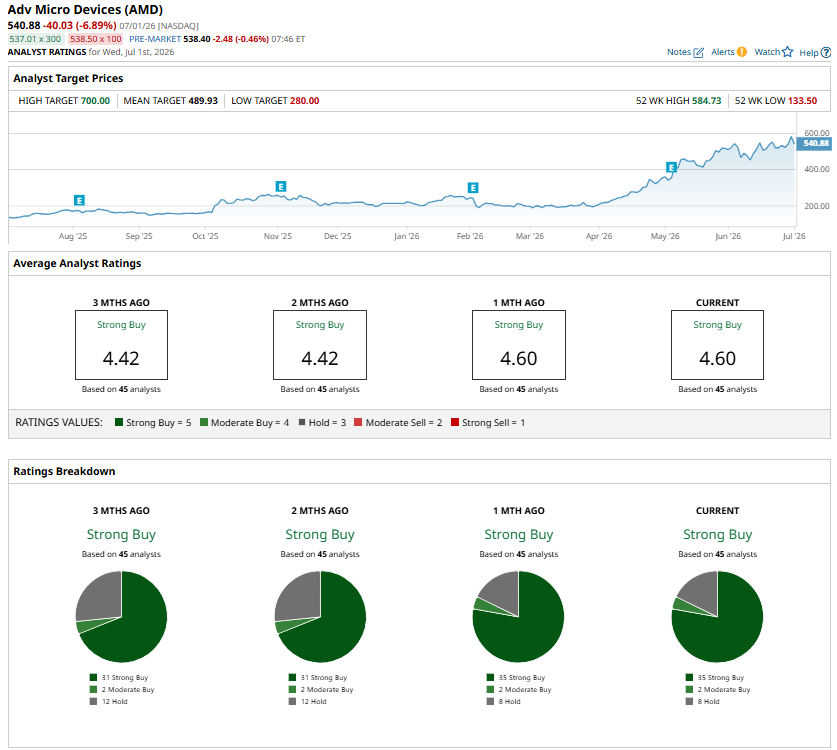

While the stock trades at a high forward earnings multiple, analysts are bullish and recommend a consensus “Strong Buy” rating for AMD.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)