While Ford (F) gained nearly 6% in the first half of the year, it was quite volatile during the period. The stock rose to a four-year high in May amid optimism over its energy storage business, which is a play on artificial intelligence (AI). However, as I noted in an article then, even though the energy storage business would help buoy Ford’s earnings once it reaches scale, the “Tesla-like rally” (TSLA) had run ahead of itself.

F stock has fallen almost 20% over the last month, and in absolute terms, it trades slightly below $14. In my previous article, I had noted that while Ford’s risk-reward has improved, it's not favorable enough to trigger a purchase. With the stock coming off those levels, let’s explore if Ford can rebound in the back half of the year.

Why Did Ford Stock Fall in June?

To begin with, let’s examine why Ford shares crashed in June. The stock was always ripe for a correction, given stretched valuations, as the AI euphoria took F a bit too far. To make matters worse, Ford reported a double-digit decline in May sales, further dampening sentiment.

The company’s persistent recall woes came to the forefront again after it recently recalled over 740,000 vehicles over a transmission defect. While the Blue Oval topped the 2026 US JD Power Initial Quality Study among mainstream automakers, its recall and warranty issues continue to be an overhang even though the management sees them more as a “legacy issue.” On a related note, Ford recently rehired engineers, including for quality checks, after its pivot to AI failed to have the desired results.

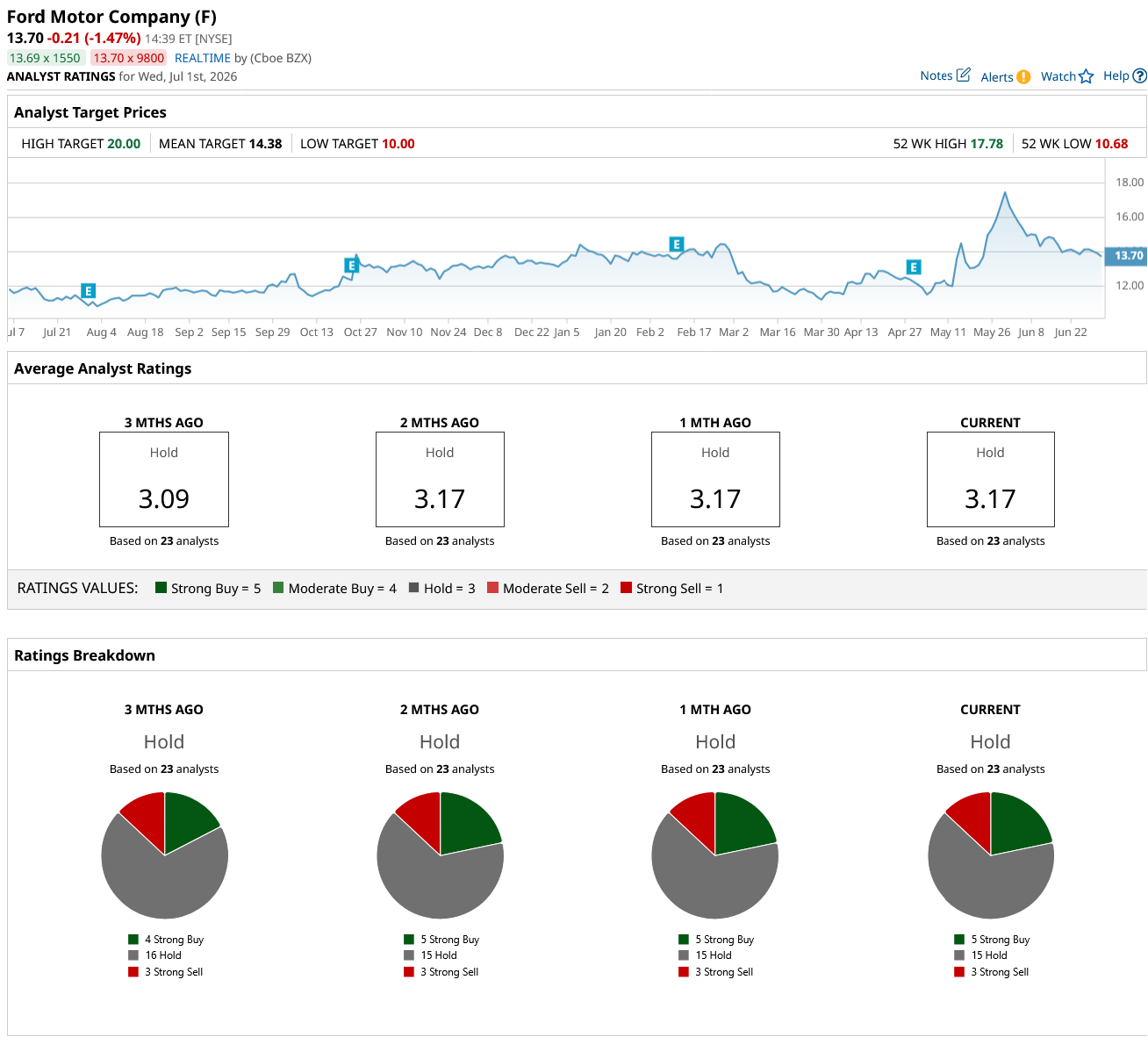

F Stock Forecast

Meanwhile, analyst action was positive towards Ford last month, and Wells Fargo, Goldman Sachs, UBS, and Citi raised F stock’s target price. Previously, towards the end of May, Bank of America raised the stock’s target price to a Street-high of $20. Overall, F stock has a consensus rating of “Hold” from the 23 analysts polled by Barchart, while its mean target price of $14.38 represents low single-digit upside over the next 12 months.

Ford’s energy storage business is among the key factors behind sell-side analysts' warming up to the stock over the last month. The energy business could be a long-term earnings driver, and Morgan Stanley analyst Andrew Percoco expects Ford's energy storage business to generate pre-tax profits of $588 million at 20 GWh annual production, at which point it predicts it would have a $10 billion enterprise value based on its assumption of a pre-tax earnings multiple of 17.5 times. However, the business won’t contribute much to the carmaker's earnings in the short term.

Moreover, the AI trade itself has transitioned, and let alone energy storage companies, even the Magnificent 7 are no longer the go-to names to play the theme. The trade currently rests with companies in the chip ecosystem (with the notable exception of early winner Nvidia (NVDA)) and memory companies.

Can Ford Stock Bounce Back in the Back Half of 2026?

The dip in gas prices should lead to higher disposable incomes and help improve sentiments and is at least theoretically positive for the automotive industry. Aluminum prices (ALU26) have also come off, which is a tailwind for automakers like Ford, as it would help lower their raw material costs. During the Q1 call, the company raised its annual pre-tax guidance by $500 million at both ends to $8.5 billion to $10.5 billion. I wouldn’t be surprised if Ford raises its 2026 guidance during the upcoming Q2 2026 earnings call.

Ford’s valuations have corrected after the crash in June, and the stock now trades at a forward price-to-earnings (P/E) multiple of 8.63x. While not mouthwateringly cheap yet, the valuations appear much more grounded now. All said, while I do expect some bounce back in F stock in the back half of the year, I don’t see it revisiting its 2026 highs.

On the date of publication, Mohit Oberoi had a position in: F, TSLA, NVDA. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)