The following is a recent report in The Spread Trader newsletter, published by Klarenbach Research.

My colleague, Brent Futz, a former WCE floor trader with 40 years of experience trading commodities, leads that publication.

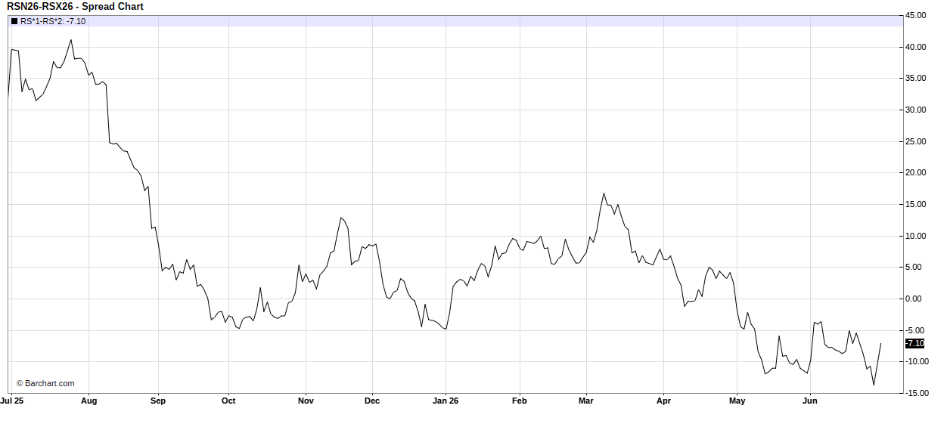

A Review of the July/Nov Canola Spread

With the July canola futures contract entering the delivery period, it is an appropriate time to analyze the July/Nov spread and the implications it has had for those participants with exposure to futures prices.

Firstly, during the life of the July/Nov spread, the spread traded in both a backwardation and a contango orientation.

The July/Nov spread peaked at a $42 inverse in July 2025 before trading to $13 under in June 2026.

The $55 range has had a very significant impact on the perpetual long and short in terms of a transfer of wealth.

For canola producers, a $55 range represents a significant effect on margins.

Chart 1: July2026/Nov 2026 Canola Futures Spread

The crucial part of the above chart starts with the spread moving from a $18 inverse in March 2026 to a carry or contango orientation through May and June.

It was during the March/June period that perpetual longs and shorts rolled their positions from old crop months into the November contract.

Given that the majority of the roll occurred under a contango orientation, it can be concluded that there was a significant transfer of wealth from the long to the short.

From the perspective of the producer, the contango orientation that existed through May and June gave producers very attractive new crop prices.

Given the commercial support for the July, it inadvertently lent support to the Nov as long as the spread maintained the contango orientation.

Simply put, the contango spread gave producers the opportunity to sell $800 new-crop canola.

If the July/Nov spread had maintained a backwardation orientation that existed in March, or even moved to a larger backwardation orientation, producers wouldn’t have been presented with the opportunity to sell $800 November futures.

The point is this: the orientation of the July/Nov was the sole reason producers were able to lock in very attractive new-crop prices.

Experienced spread traders with a well-defined set of criteria were able to anticipate the shift towards a contango orientation starting in March and the implications it would have on new crop prices.

The above analysis is meant to emphasize the role spreads play for all participants and how spreads affect all participants.

In conclusion, understanding spreads should be used to complement any trading strategy.

Happy Trading

Brent Futz (b.futz@hotmail.com)

Brent covers this technical setup and specific price targets in depth in the The Spread Trader

Join 3,500+ farmers getting sell signals and technical roadmaps here:

Trent Klarenbach, BSA AgEc, PAg, publishes the Klarenbach Grain Report, Klarenbach Special Crops Report and The Spread Trader newsletters.

Klarenbach Research

Sign up below for a FREE trial of our newsletters

Wheat Canola Corn Soybeans Soybean Oil Spring Wheat Soybean Meal Hard Red Winter Oil Oats

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)