/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

Innodata (INOD), an emerging artificial intelligence (AI) infrastructure company, is quickly grabbing the market’s attention. The stock has climbed 43% year-to-date (YTD), outperforming even the trillion-dollar tech giants like Apple (AAPL) and Tesla (TSLA). Innodata is an AI data infrastructure company that helps leading tech companies build, train, and deploy AI models. The company doesn’t make critical AI infrastructure such as servers, GPUs, or networking hardware. Instead, it provides the training data, testing, and evaluation services that allow AI models to perform effectively.

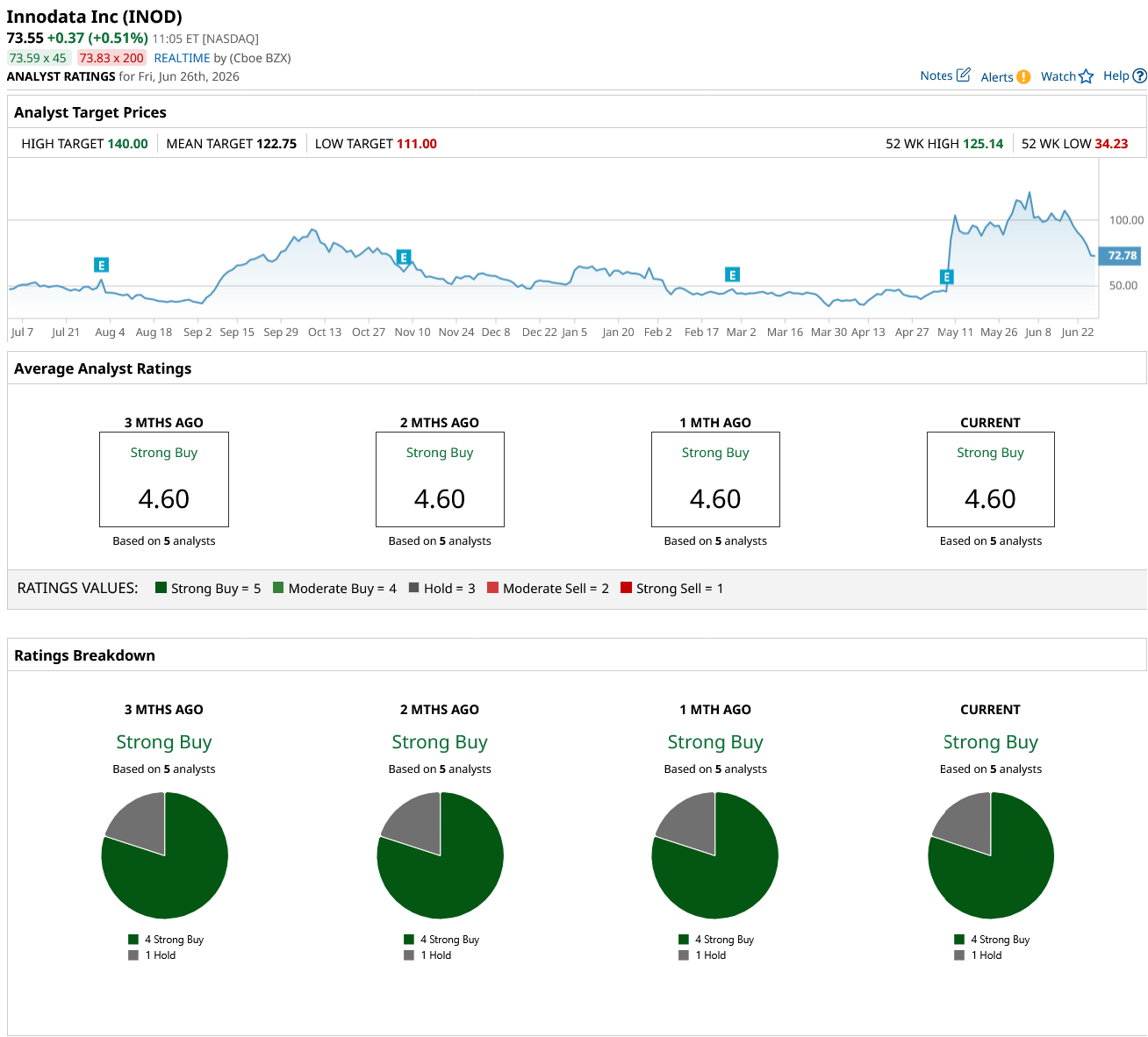

Despite its rally this year, Wall Street believes INOD stock has over 93% upside over the next 12 months if it hits its high price estimate. I believe so too.

Let’s dig in to find out why.

The Business Is Growing Faster Than Anticipated Earlier

Innodata doesn't build AI models. It provides services that AI developers need for the models to work reliably. These services include training data, reasoning datasets, model evaluation, and AI agent monitoring, among others. The company has been working on extending its customer base, deepening ties with customers, increasing margins, and creating new products that could make growth more sustainable. These efforts were reflected in its first quarter, where revenue climbed 54% year-over-year (YoY) and 24% sequentially to $90.1 million. Even more impressive was that revenue beat consensus estimates by $13.6 million. The bottom line grew as rapidly as the top line, with net income up 90% YoY to $0.42 per share.

For a small company of $2.5 billion market cap, these numbers are definitely impressive. Management even emphasized that the revenue generated in Q1 exceeded the revenue generated in a complete year just three years earlier. The company now expects roughly 40% growth in revenue in 2026 to around $357 million. Interestingly, this forecast doesn’t yet include several potentially large programs that the company has yet to finalize. This implies that demand is still building faster than the company originally planned.

This confidence stems from a recently announced deal with one of the “world’s leading big tech companies.” Management expects this single customer to help generate $51 million of revenue in 2026, making it its second-largest account. While Innodata didn’t reveal the customer’s name, it is believed to be one of the "Magnificent Seven" stocks. The Mag 7 group includes Apple, Amazon (AMZN), Alphabet's (GOOG) (GOOGL) Google, Tesla, Microsoft (MSFT), Nvidia (NVDA), and Meta Platforms (META).

The company also highlighted that its core market spans roughly across 20 organizations globally that are developing the most advanced AI foundation models. Analysts forecast Innodata’s earnings to increase by 24% to $1.14 in 2026, followed by 61.4% in 2027.

Why Innodata Could Become a Long-Term Winner

Based on the expected double-digit growth in the next two years, analysts believe INOD stock could surge over 69% from current levels to reach $122.75. Plus, analysts have set a high price target of $140, implying that the stock could rise 93% over the next 12 months. While Innodata cannot be expected to grow as rapidly as the top infrastructure players like Micron, Lam Research (LRCX), or SK Hynix. Even so, the company still operates in one of the rapidly evolving areas of AI. As AI models evolve, the services Innodata provides will become even more important. Additionally, the company is developing higher-value offerings such as expert-generated reasoning datasets and proprietary software platforms, which could command even better margins.

On the downside, investors have priced in years of growth, which is why the stock now trades at a premium of 71 times forward earnings. If revenue or earnings growth slows, share price may react strongly. There is also customer concentration risk, as a few large tech companies account for a chunk of the company’s total revenue. That said, Innodata has the potential to be a long-term AI winner if it could expand into a more recurring, software-driven revenue model while maintaining strong customer relationships and diversifying its revenue base.

Overall, analysts also see INOD stock as a long-term AI winner and have rated it a consensus “Strong Buy.” Of the five analysts covering the stock, four rate it a “Strong Buy,” and one says it is a “Hold.”

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)