/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

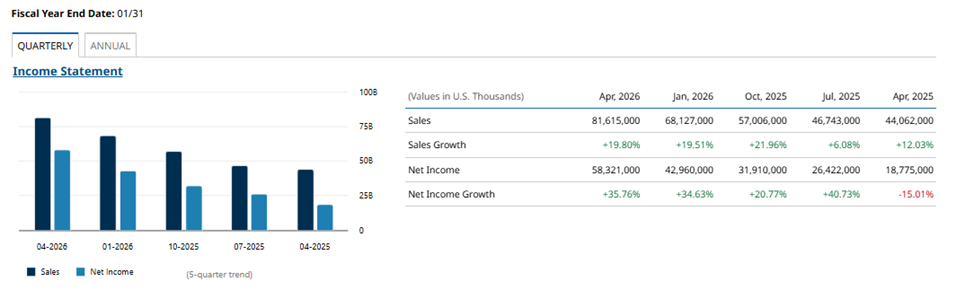

Today, Nvidia (NVDA) comes across as an unshakable dominator and primary beneficiary of the AI paradigm shift. Its trillion-dollar valuation and phenomenal quarterly filings paint an illusion of an endless, smooth runway for investors, with the trading floor pricing shares as if its geometric ascent will never crash into a concrete barrier.

Yet the reality is noticeably harsher. The runway is ending. The severe physical constraints of the semiconductor space and fundamental laws of economics relentlessly dictate their own terms. Nvidia is being dragged into a grueling two-front strategic war that will inevitably slice through its anomalous excess profits.

Nvidia is hitting a ceiling. To comprehend why the era of "easy multiples" in equities like NVDA is coming to a close, one must look away from current revenues and dissect the mechanics of the snare in which the company finds itself. Let's take a closer look.

How Nvidia Attempts to Sell the Entire Data Center

Historically, Nvidia has operated as a pure-play manufacturer of graphics processing units (GPUs). This monolithic foundation generated virtually 100% of the firm's top line. However, today the business architecture is fracturing. Nvidia is attempting to shed its label as a supplier of a single — albeit ingenious — component.

Observing its maneuvers, one might presume that Nvidia's playbook is an aggressive metamorphosis into mastering data-center infrastructure entirely. Nvidia is encroaching on new markets, rolling out its own Grace central processors and Vera architecture, attempting to squeeze the customary Intel (INTC) and AMD (AMD) chips out of servers. Concurrently, an assault on the multi-billion-dollar networking equipment arena is underway. Leveraging NVLink and Spectrum-X technologies, Nvidia is capturing switches and Ethernet networks, where Cisco (CSCO) and Arista Networks (ANET) have reigned supreme for decades. Completing the picture is its intrusion into heavy physical infrastructure via the sale of turnkey racks like the NVL72, with Nvidia imposing its own power distribution and highly complex liquid cooling standards on the market.

For investors, the process can be explained by a straightforward analogy. Imagine a plant producing unique, unparalleled engines for racing cars. Realizing that rivals are on the verge of copying the tech, the manufacturer decides to assemble vehicles in their entirety — from the seats to the brake pads. Nvidia is frantically digging an infrastructural moat around its operations, forcing clientele to purchase not a solitary die but a closed ecosystem.

Yet this expansion is not being dictated by ambition. Instead, it is a forced line of defense, as a full-scale offensive has commenced against Nvidia's primary business.

The Assault on Nvidia's Gold Mine

As Nvidia attempts to bite off pieces of other people's pies, the foundation of its own castle — the AI accelerator arena — is being aggressively undermined from two directions simultaneously. The software barrier that protected the monopoly for years has collapsed, and its notorious "hardware moat" is now proving critically vulnerable.

For many years, coders had the tight leash of the CUDA platform, since writing scripts for third-party silicon was unbearably difficult. But the emergence of open compilers like OpenAI Triton and the deep integration of rivals with the PyTorch ecosystem have shattered this wall. It is no longer a matter of principle for top-level developers exactly which hardware their models spin on.

However, the primary menace stems not even from direct adversaries like AMD, whose fresh chips boasting colossal memory capacity are already aggressively biting off share in the inference space. The overriding threat is Nvidia's own largest patrons. Cloud behemoths — Alphabet (GOOGL), Amazon (AMZN), Meta Platforms (META), and Microsoft (MSFT) — categorically refuse to endlessly subsidize someone else's super-margins. Accordingly, they are now throwing their weight into forging their own custom silicon (ASICs), like the Google TPU or Amazon Trainium. In contrast to Nvidia accelerators, which resemble an insanely expensive universal Swiss Army knife, the custom solutions of Big Tech are surgical scalpels. They are tailored for a single specific task, cost less in manufacturing, draw less power, and hit right on target. Armed with protected top-line streams from cloud services, these corporations are squeezing out Nvidia's universal solutions with their own silicon.

The Profitability Snare

Here unfolds the main financial drama of this two-front war. Nvidia's ongoing business framework represents a textbook margin dilution trap. In my view, this process is easiest to conceptualize through the metaphor of pasture.

The GPU arena for AI is unique, ultra-fertile land. Gross profitability here reaches 75%, generating colossal net earnings. It is precisely this elite soil that rivals and Big Tech ASIC chips are trampling right now. The forfeiture of even a 15% to 20% slice of this field would wash away operating income by the billions. Competitors are tearing away the juiciest, most cash-rich segment of the space.

Where does Nvidia flee for compensation? It advances into CPUs, networking cables, and cooling setups. But the issue is that, compared to GPUs, these are more ordinary pastures. The profit margins of the historically established server networking market rarely top 60% to 65%, and the CPU arena generally hovers around the 50% mark. Furthermore, the assembly of heavy racks forces the procurement of copper, pumps, and power supply units, turning margins from a light "silicon" variety into a heavy "manufacturing" one.

The math here operates against the company. By attempting to cover loss of share in a space with 75% margins via an aggressive push into segments featuring 50% to 60% profitability and lower, Nvidia is losing out in financial quality. Revenues might swell from selling expensive server complexes, but the efficiency of every earned cent will drop. This strategically disadvantageous trade-off is currently being successfully masked by the market's frenzy for any compute capacity.

The Demise of ‘Nanometer Magic’

To comprehend how challengers even obtained a shot at catching up to Nvidia, one has to peer inside the chips themselves. For years, technological supremacy was defined by a straightforward transition to a new, finer fabrication node. A smaller transistor meant more horsepower and less power consumed.

Today, this express train has hit the brakes. Physics has bumped against its boundary. Take for example Nvidia's Blackwell architecture. For the first time in a long stretch, these new dies are being manufactured on the exact same 4-nanometer Taiwan Semiconductor (TSM) node as their Hopper predecessors. Physical shrinkage of the transistors did not occur; engineers achieved performance gains purely via extensive "brute force." They took two massive silicon dies and bound them together with an immensely complex bus, spawning a monster featuring 208 billion transistors. As a consequence, the power draw of a single unit soars past an insane 1000 watts, while the complexity of gluing the dies together has sharply escalated the defect rate and pushed up the cost of goods sold.

When the nanometer runway narrows, technological superiority finds itself under threat. Previously, Nvidia ran ahead of the crowd because it could roll out fresh products on a new tech foundation. Now, TSMC foundries — much like the facilities of Intel or Samsung — are open to everyone. Nvidia, AMD, and Big Tech developers alike are crowding in the exact same queue for the very same 3-nanometer wafers. When everyone has identical transistor density under the hood, winning purely on silicon becomes unfeasible. Time begins to work for the chasers. While the frontrunner gets stuck on a plateau, the pursuers are managing to level up their software and architecture.

The Financial Verdict

The demolition of the software wall, the assault of custom chips, the forced migration into lower-margin networking, and the halt of physical advancement all merges into a unified financial verdict for Nvidia's ongoing valuation. For now, the dam of demand is rescuing the balance sheet, with tech behemoths sweeping up everything in sight for the sake of AI supremacy. Liquidity is sufficient for everyone at the moment. But equities live in the future, and in that future, this demand will inescapably decelerate.

The infrastructural budgets (capex) of corporations are immense, but not bottomless. Sooner or later, Big Tech shareholders will demand to see genuine returns on investment (ROI) from these frantic expenditures. Once the foundation for training models is fully built out, the focus will shift toward optimization, and demand momentum will moderate or even level off.

A halt in progress equates to commoditization. A unique engineering marvel transforms into a mundane mass-market commodity like RAM, where pricing alone dictates the rules. The stock exchange does not forgive such transformations. Today, Nvidia trades as an unconditional growth play. But as soon as financiers realize that super-profits are being diluted by rivals and escalating production costs, the pricing mechanisms will shift.

Nvidia will start to be valued like a classic manufacturer of cyclical hardware. Even if sustainably high net earnings are maintained, a routine downward compression of trading multiples due to risk repricing will mechanically slash the company's equity value.

Conclusion

Nvidia will neither collapse nor vanish. It will remain one of the greatest engineering entities of our time, backed by brilliant management. Its top-tier status is not going anywhere.

The problem lies entirely elsewhere. Nvidia's status as a god-like dominator has already been exhausted. To survive at the peak, the firm will likely have to swap its triumphant march for a bloody trench war, defending its share while sacrificing profit margins. For investors, this means the runway for an explosive rally has already ended. Ahead lies the harsh gravity of economic cycles, where Nvidia will morph simply into the first among equals, and the era of easy excess profits will conclude.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.