/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

When it comes to hardware for artificial intelligence, the majority of investors instinctively look at Nvidia (NVDA).

At the same time, a much less public race to develop custom chips (ASICs) is unfolding. These are specialized processors that cloud giants develop using their own algorithms. Two companies currently dominate this niche: the giant Broadcom (AVGO) and the relatively small Marvell Technology (MRVL). At first glance it may seem that Marvell is simply a lagging player in the shadow of its big competitor.

But if you dig deeper, it becomes clear that competition here is not what it seems. This is not a competition between two manufacturers, this is a proxy-war of gigantic technological coalitions.

The Battle of Ecosystems, Not Companies

To understand the potential of Marvell, investors must know one fact. ASICs customers do not buy ready-made chips. They co-develop and co-design them. Today, the market of custom AI accelerators is divided into two powerful camps. Firstly, there exists the coalition of Broadcom, Google (GOOG) (GOOGL), and Meta (META). Secondly, we have the coalition of Marvell with Microsoft (MSFT) and Amazon (AMZN).

It turns out that Marvell does not compete with Broadcom in a vacuum. Marvell acts as the technological and engineering partner for Microsoft and Amazon. The success of Marvell on this market directly depends on how successful the Azure and AWS cloud segments are. Behind the back of Marvell stand the budgets and infrastructure of the richest corporations of the world, which makes the positions of the company seemingly very solid.

The ‘Vendor Lock-In’ Effect and High Switching Costs

The business model of custom chips forms a colossal attachment of the client to the vendor.

The development of such processors is the merging of intellectual property. Microsoft, for instance, brings its architecture, and Marvell provides the fundamental blocks: super-speed interfaces of data transfer, technologies of packaging of chiplets, and network solutions. This process takes years.

If a cloud giant wants to change its partner (for example, to switch from Marvell to Broadcom), it would be necessary to rewrite low-level software and begin engineering practically from zero. In the world of ASICs, a “divorce” costs billions of dollars and years of lost time. This creates for Marvell the widest economic moat and guarantees, possibly, the stability of long-term contracts.

Financial Portrait: Transformation into Stability

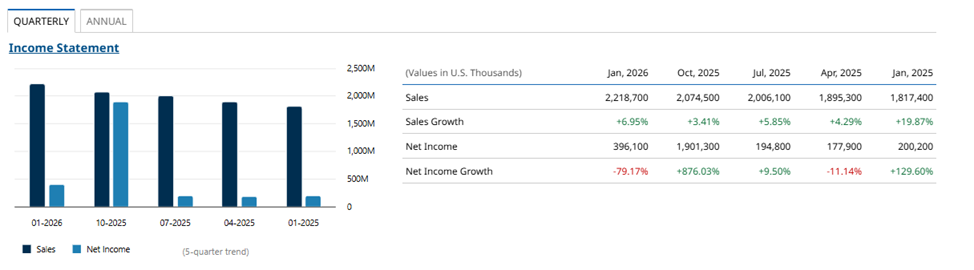

For a long time investors were frightened away by Marvell’s high research and development expenses. However the last data show that the aggressive investment phase began to bear fruit. As is visible from the financial indicators, the revenue of the company is in a stable growth phase. In the quarter that ended January 2026, sales reached $2.21 billion, up almost 7% compared to the previous quarter and by 22% year-over-year (YoY).

What is still more important is that the company stably generates net profit, having overcome the phase of unprofitability. Excluding the one-time anomalous spike in net profit in October 2025 (connected with accounting/tax corrections), the base operational activity of Marvell shows a healthy trend: from ~$200 million of profit in the beginning of 2025 to almost $400 million in the beginning of 2026. Operating leverage has kicked in.

The Upside Ceiling: Why Marvell Is Not Nvidia

Despite the positive trend, it is necessary for investors to clearly understand the limitations of this business model. Marvell, most likely, will not become a “second Nvidia” by the level of margin. Nvidia sells universal solutions with a huge markup, since it controls the whole product. In the case with ASICs, Marvell and Broadcom, in essence, provide engineering services. The main goal of Amazon or Microsoft during the creation of custom chips is lowering their own capital expenses.

The tech giants invest in joint development exactly for that reason, to economize. Therefore they rarely allow their engineering partners to take away super-profit. Margins in the segment of custom chips, seemingly, will have a harsh “ceiling.” An investment into Marvell is a bet on huge volumes and not on a sky-high markup.

The Downside Floor: The Effect of the Low Base

Exactly here hides the main potential of the company. The capitalization of the giant Broadcom exceeds $1.5 trillion. Marvell, with a capitalization around $100 billion, therefore looks tiny.

At the same time in the technological race, their coalitions are comparable. If the market of custom chips will grow as analysts forecast, the influence of this growth on the valuation of the companies will be radically different. For Broadcom, this will be only a pleasant addition to its diversified business. But for Marvell, thanks to the effect of the low base, this, possibly, will mean a multiple growth of fundamental indicators.

Outcome

Marvell Technology is a unique asset in the AI infrastructure market. On the one hand, the expectations of investors must be restrained due to the features of the business model. On the other hand, the status as an exclusive engineering partner in the coalition with Microsoft and Amazon, high barriers for client exit, and the effect of the low base by comparison with the main competitor, create for the company a significant potential.

This is not a story about a phenomenal markup, this is, perhaps, a story about fundamental, mathematically justified growth together with the leaders of cloud technologies.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)