Meta Platforms (META) has taken a major step beyond the digital realm, sealing a deal that signals its serious ambitions in real-world robotics and humanoid automation. On May 1, the social media behemoth completed its acquisition of Assured Robot Intelligence, a startup that allows robots to function alongside actual human beings in real environments.

Co-founders Lerrel Pinto, Xiaolong Wang, and Xuxin Cheng will carry their entire team into Meta's artificial intelligence (AI) research division, bringing serious horsepower in model design, frontier robot control capabilities, self-learning systems, and whole-body humanoid control straight through the door.

Meta described the startup's core work as teaching robots to read and respond to human behavior across chaotic, unpredictable, real-world conditions, calling that exact territory the frontier of robotic intelligence.

The timing of this deal fits hand in glove with Meta's broader financial posture. Last month, the company announced it was hiking its capital spending forecast for the year between $125 billion and $145 billion, and the acquisition slots right into that expanded war chest.

Meta's robotics engineers are currently covering everything from sensors to software, building humanoid hardware from the ground up with full plans to open those tools across the wider industry. With all of this now on the table, the question becomes whether META stock can earn a spot in your portfolio right now.

About Meta Stock

What began in a Harvard dorm room has grown into the structural foundation of connecting the world online, with Facebook sitting at the center of an empire that now includes Instagram, WhatsApp, and Messenger serving billions of people on a daily basis.

The Menlo Park, California-headquartered Meta now commands a market cap sitting at roughly $1.54 trillion and is throwing serious capital at AI, smart glasses, and virtual reality, with the ambition of turning computing into something ambient, immersive, and impossible to escape.

META stock has been anything but a straight line over the past year. The stock managed a 0.80% gain across the last 52 weeks, but the year started on a rough note with the stock shedding 8.5% year-to-date (YTD). The selling pressure has not had the last word though, as the stock has clawed back 5.16% over the past month.

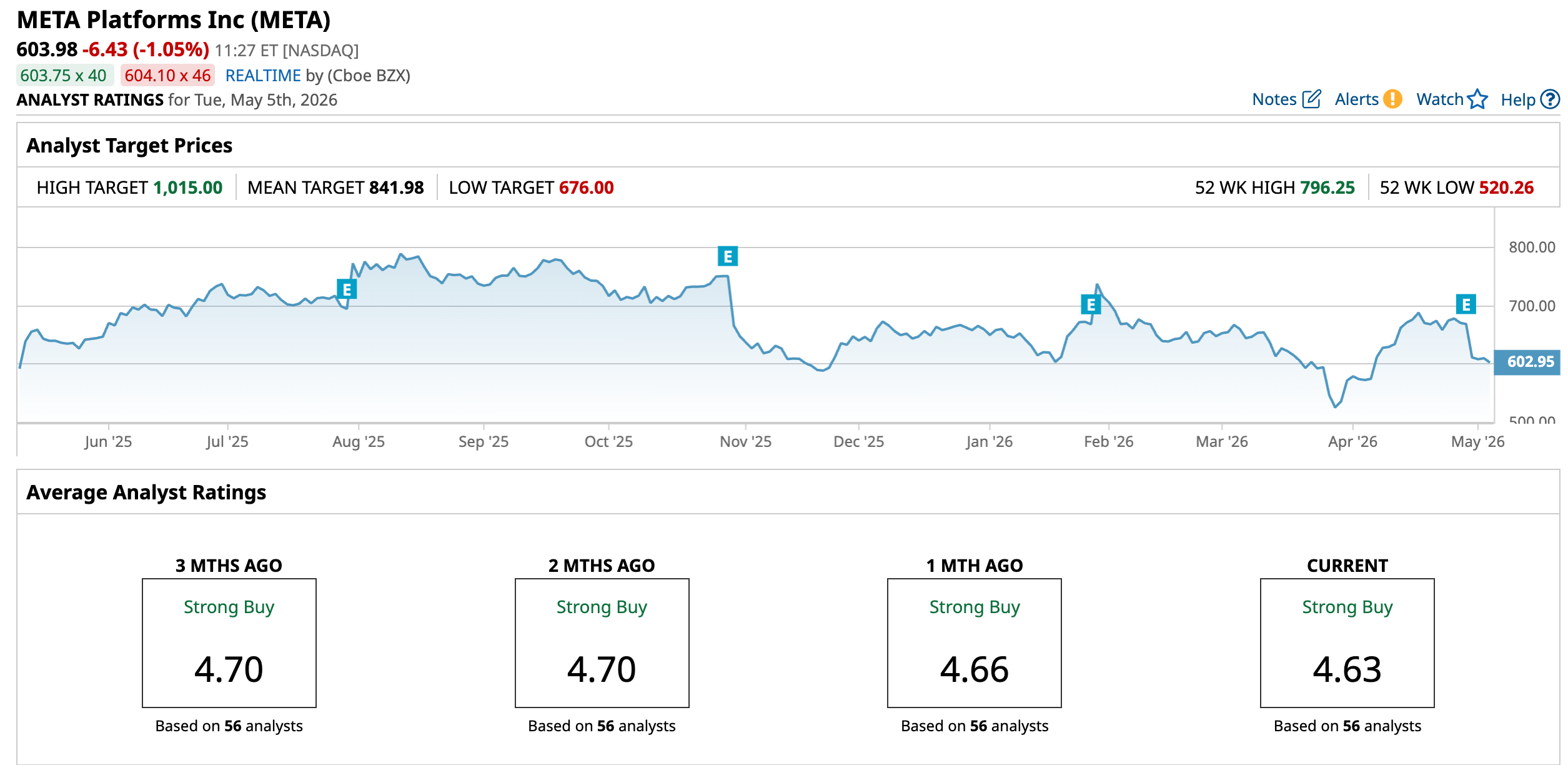

On the valuation front, META stock is currently trading at 19.75 times forward adjusted earnings and 6.12 times sales, numbers that look stretched relative to peers at first glance but actually sit below Meta's own five-year average multiples. This hands long term investors a reasonably comfortable entry point without feeling like they are buying at the very top of the mountain.

Also, Meta pays shareholders an annual dividend of $2.10 per share, translating to a yield of 0.34%. The most recent quarterly installment of $0.53 per share landed in investor accounts on March 26 for everyone who was on the books as a shareholder of record by March 16.

Meta Surpasses Q1 Earnings

Meta Platforms dropped its Q1 fiscal year 2026 earnings on April 29 and promptly cleared the bar that Wall Street had set. Revenue climbed 33.1% year-over-year (YOY) to $56.31 billion, clearing the analyst estimate of $55.56 billion. EPS grew 62.4% from the prior year’s quarter to $10.44 and left the Street's expectation of $6.67 looking rather conservative in hindsight.

Family daily active people averaged 3.56 billion for March, reflecting a 4% YOY increase, though a modest sequential dip crept in due to internet disruptions in Iran and a restriction on WhatsApp access across Russia.

Ad impressions across Meta's family of apps surged 19% YOY and the average price per ad moved up 12% over the same period. Headcount stood at 77,986 as of March 31, nudging up 1% from the prior year.

Despite the strong print, the stock tumbled 8.6% the very next trading session after Meta revealed it was lifting its AI capital expenditure outlook for the year between $125 billion and $145 billion, up from the earlier forecast of $115 billion to $135 billion. The elevated spending figure swallowed all the good news from the quarter whole.

On the guidance front, Meta’s management has pointed to Q2 fiscal year 2026 revenue landing somewhere between $58 billion and $61 billion, while full year 2026 total expenses are expected to hold steady in the $162 billion to $169 billion range, unchanged from the prior outlook.

On the other hand, analysts are penciling in Q2 fiscal year 2026 EPS of $7.19, a marginal YOY improvement, and project full year fiscal 2026 earnings growth of -0.34% to $29.59 per share, followed by a more robust 17.71% jump to $34.83 in fiscal year 2027.

What Do Analysts Expect for Meta Stock?

A handful of analysts have trimmed their price targets on META stock. However, they did not lose any conviction on the stock. Stifel's Mark Kelley pulled his price target down to $780 from $805 while holding firmly onto his “Buy” rating.

Bernstein made a similar move, cutting its price target to $850 from $900 while keeping an “Outperform” rating in place. UBS analyst Stephen Ju brought his target down to $865 from $908 and also stuck with his “Buy” call on the shares.

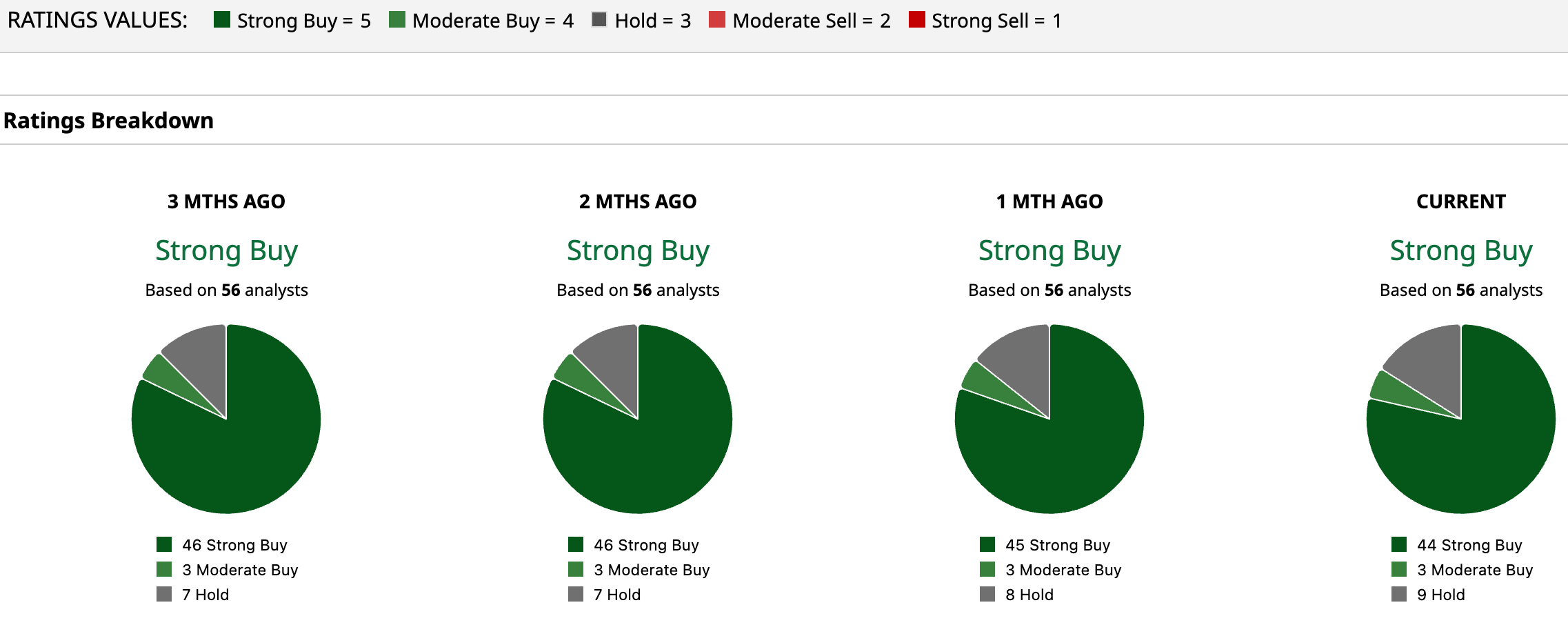

Even so, the broader Wall Street has assigned the stock an overall rating of “Strong Buy.” Across 56 analysts covering META stock, 44 have stamped it a “Strong Buy,” three are sitting at “Moderate Buy,” and nine are holding at “Hold.”

The average price target of $841.98 points to a potential upside of 39.4% from current levels, and for those with a higher risk appetite, the Street-High target of $1,015 suggests the stock could run as much as 68.1% from where it trades now.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)