/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20and%20cabinets%20full%20of%20hard%20drives%20inside%20large%20data%20center%20by%20IM%20Imagery%20via%20Shutterstock.jpg)

It is no secret that we live in a period of elevated geopolitical risk. Continuing military conflicts, the rebuilding of global supply chains, and the constant threat of unpredictable oil price spikes — all this creates an extremely complex environment for macroeconomic forecasting.

This is why I believe investors must search for companies whose businesses rely on fundamental, long-term technological shifts. One such idea, in my view, is Advanced Micro Devices (AMD). I believe that this company possesses such a powerful structural potential in the computing market that it is capable of ignoring macroeconomic noise. This company has its own, very strong internal story, which will turn out stronger than the unfavorable surrounding environment.

AMD Finally Exits the Shadows

For a long time, the market of high-performance AI accelerators was perceived by the investment community as a winner-take-all race. Investors saw Nvidia (NVDA) as unshakable, its ecosystem impregnable, and all the remaining players, including AMD, as doomed to be content only with the scraps of niche contracts.

Historically, AMD has been stuck with the image of a sort of “eternally catching up” discounter. But, as I think, the events of the last year and a half, and especially the results of 2025, are finally starting to change this established narrative. We are becoming witnesses to a tectonic shift: AMD should no longer be viewed simply as some kind of “backup option.” The company is transforming into a real heavyweight and, what is the most important, an independent competitor in the GPU market.

What we are observing right now is not a one-time anomaly, caused by a temporary deficit of chips on the market, but evidently marks the beginning of a long-term paradigm shift, where hyperscalers no longer want to depend on one dominant supplier.

Proof of Growth: Numbers, Margin and Contracts

In financial analysis, words must always be supported by numbers, and in the case with AMD, the reporting speaks for itself.

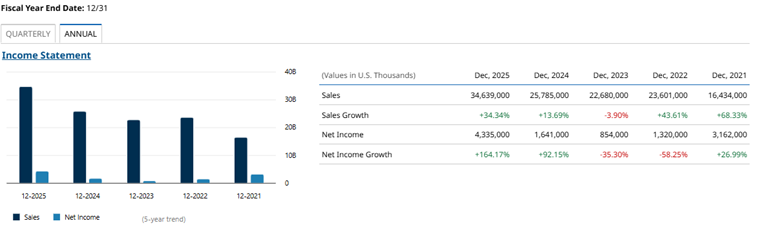

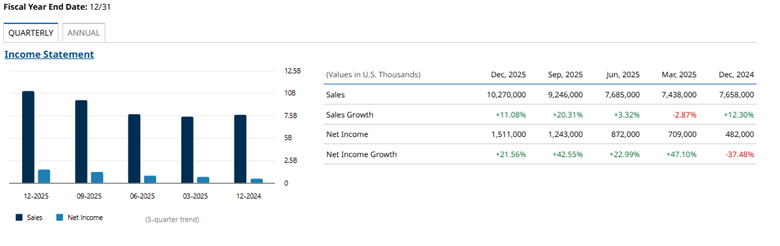

Based on 2025 results, the dynamic looks not simply positive, but qualitatively different in comparison with previous periods. Let’s start from the main growth driver — the Data Center segment. For the full year 2025, the revenue of this subdivision reached an impressive $16.6 billion. At the same time, it is important to note the quarterly acceleration: the fourth quarter alone accounted for about $5.4 billion of revenue in this segment. If we look at the company as a whole, total annual revenue confidently stepped over the mark of $34.6 billion, having shown an impressive growth of approximately 34% in comparison with $25.7 billion in 2024. But for me, as for an analyst, the most telling metric is not the revenue, but how it converts into profit. The net income of the company for 2025 surged to $4.3 billion (against $1.6 billion a year earlier). This almost three-fold growth points to a powerful operating leverage: the company learned to effectively scale the production of AI chips.

Besides dry numbers, the qualitative composition of the revenue is extremely important. We see clear signs of the fact that the giants of the industry — Meta (META), Microsoft (Azure) (MSFT), Google (GOOG) (GOOGL), and Oracle (ORCL) — are gradually transitioning from the stage of cautious testing to the full-scale implementation of solutions based on AMD chips, in particular, the flagship lines MI300X and the newest MI350. The deepening partnership with OpenAI deserves special attention. Similar large-scale contracts are evidence that the industry made a conscious bet on diversification. Big budgets (like the “smart money” of the technological sector) already began to flow in the direction of AMD, forming a reliable base for future periods.

Breaking Through the Software Barrier

Many investors, comparing the positions of AMD and Nvidia, mistakenly focus their attention exclusively on the technical characteristics of the processors — teraflops, memory bandwidth, or process technologies.

However, in my view, the secret of the total domination of Nvidia consisted in something completely different. The main economic moat was not at all the architecture of the “hardware” (in the end, both companies produce their flagship chips at the exact same Taiwan Semi factories in Asia, and the production capabilities for them are conceptually similar). The real barrier was the closed software ecosystem CUDA. To understand the scale of the current shift, I propose we delve a little into the mechanics of how it was formed and why it was so difficult to destroy it earlier. CUDA became for AI developers the same thing that Windows became for personal computers in the 90s — a de facto industry standard with no alternatives. Practically all libraries, frameworks, and models historically were written exclusively for CUDA.

For years, the situation for any competitor, including AMD, looked like a classic chicken-and-egg dilemma. For clients to start massively buying your graphical accelerators, you need a developed, convenient and working “out of the box” software ecosystem that is on par with CUDA. But to create and maintain such an ecosystem — to write thousands of libraries, optimize drivers, ensure the support of all new neural networks — colossal, regular investments are required, calculated in billions of dollars. And where do you get these billions, if the market is relatively small, and the sales of your chips are minimal? In the past, prior to the beginning of the global AI boom, the volume of the market simply did not allow AMD to form that critical mass of capital. To develop a full-fledged competitor to CUDA for an alternative supplier was simply financially unviable. The barrier seemed insurmountable, because the entrance ticket to this club cost too much.

But right now we, evidently, are observing a historical turning point, and it hides exactly in the new sales volumes.

Having exited to the level of revenue from data centers of $16.6 billion for the year, AMD finally received what it so acutely lacked all these years — a sufficient concentration of capital for the full-scale development of software. The market became so huge and cash-rich that the creation and support of an “alternative operating system” for AI computations for the first time became financially justified.

Judging by the reports, the company directs unprecedented resources to this front: expenses on R&D just in the fourth quarter of 2025 exceeded $2.3 billion. Now AMD can afford itself to maintain an army of programmers capable of bringing the ROCm ecosystem up to industrial standards.

Moreover, the motivation of the buyers themselves changed — and this is, perhaps, the key factor. When technological giants begin to purchase AMD accelerators not in test batches, but for billions of dollars, they automatically have a vested interest in the fact that the software for these chips works flawlessly. Buying this hardware, partners will be forced to adapt their software products for it.

In essence, the industry right now with joint efforts finances and creates this alternative software environment to get rid of the necessity to pay a scarcity premium to the market leader. The strategic bet on open compilers, such as Triton from OpenAI, serves here as a catalyst. Triton works like a universal translator: the developer writes the code once, and the compiler itself adapts it both for Nvidia and for AMD. Developers are now ready to spend time on this adaptation simply because the colossal volume of money in the sector makes such efforts highly profitable. In my view, this makes AMD not simply a manufacturer of good microcircuits. This makes the company the core of a forming alternative ecosystem, capable of systematically and long-term winning back its lawful share on the market.

The Valuation Thesis: Why the Current Valuation Opens a Window of Opportunities

Transitioning from qualitative changes in software to hard numbers and valuation multiples, we must ask ourselves the main question: to what extent does the current share price reflect this fundamental breakthrough? As a rule, markets are inclined to overestimate short-term events and underestimate long-term structural shifts. And it appears to me that right now we are observing exactly such a picture.

Let's look at the current valuation of the company. As of this writing, the capitalization of AMD constitutes approximately $415 billion, with the share price trading around the $255 mark. At first glance, this seems huge. However, in investments, everything is relative. If we compare this figure with the colossal volume of the target market of equipment for artificial intelligence and with the multitrillion-dollar capitalization of its main competitor, the valuation of AMD no longer looks overheated. Rather, it looks like the valuation of a company located only at the beginning of a lengthy path of scaling.

Let’s turn to the valuation multiples. The shares of the company have recently demonstrated a powerful upward dynamic, approaching their all-time highs. In my view, this surge indicates that the market has begun to aggressively price in the fundamental thesis of the software breakthrough. For a technological company that in just one year was able to increase its net profit practically three times (from $1.6 billion to $4.3 billion), such a level of valuation can still be called highly conservative. The market, by all appearances, is finally believing in the fact that AMD will be able to hold the gathered pace.

But if my thesis about the destruction of the CUDA dominance is true, then the mathematics of the potential becomes obvious. Revenue of $16.6 billion from the data center segment is a grandiose success for AMD, but in the scales of the entire global AI computing market, this is still a relatively modest share. The company has room to grow. The market became so huge and capital-intensive that it is physically capable of “feeding” two giants.

AMD no longer needs to destroy the business of Nvidia to grow in multiples; it is enough for it simply to systematically take its share of new contracts, and with the current revenue, this will mean an exponential growth in earnings per share (EPS) in the coming years.

Modeling of Value: A Conservative Scenario for the Investor

I consider it important to shift our qualitative thesis into the language of dry numbers. Let’s build a basic financial model for AMD for the horizon of 2027-2028. To avoid excessive optimism, which “bullish” forecasts are often prone to, I propose we conduct a conservative calculation in the format of a classic text, but with the mandatory accounting of the change in the structure of the revenue of the company itself.

The management of AMD and the majority of industry analysts forecast that the total volume of the target market of AI accelerators by this time can reach an unbelievable $400 billion. We, however, will be more cautious and assume that the real volume of the market will comprise about $300 billion. Since the software barrier is punched through, clients will inevitably diversify suppliers. If AMD takes for itself a modest 15% of this market, this will provide the company with about $45 billion of revenue only in the high-margin data center segment. Let’s add to this the traditional business of the company, including processors for PCs and consoles, which, as I suppose, will stably generate $25 billion. In total, my conservative valuation of the aggregate annual revenue of AMD constitutes around $70 billion by 2027-2028.

Here lies the most important detail of our modeling. As the share of the data center segment in total revenue will grow, the overall profitability of the company will inevitably go upwards. However, I will not assume a cosmic net margin at the level of 40%-50%, like for the current market leader. Two strong players remain on the market, and AMD will have to use price dumping to capture share. Therefore, I assume realistic parameters of net margin: the historical 10% for the base business and 25% for the data center segment. This figure for AI chips takes into account both their high added value and the harsh pressure of upcoming price wars.

Relying on these inputs, we can calculate the forecast net profit. The base business will bring $2.5 billion, and the AI segment will add another $11.25 billion. The aggregate net profit in our model will constitute $13.75 billion, which more than three times exceeds the excellent results of 2025. Taking into account that there are approximately 1.62 billion shares outstanding, this yields a forecast earnings per share at the level of $8.48. For a confident valuation of a mature technological company, I prefer to use a conservative forward P/E multiple, equal to 30x. Multiplying our indicator of earnings per share by this multiple, we arrive at an implied valuation in the neighborhood of $254 per share.

The fact that current quotes have already reached this $254-$255 level is highly indicative. It visually demonstrates that the market has completely recognized and priced in this baseline, conservative scenario of a 15% market share. However, it is crucial to understand that this model acts as a fundamental floor, not a ceiling. Considering the ongoing evolution of AMD’s software ecosystem, the company is fully capable of capturing a significantly larger portion of the market than just 15%. If the business continues to scale its software capabilities and systematically grab further market share, the intrinsic value will push much higher.

Furthermore, as we perfectly know from the history of the stock market, market sentiment often plays a massive role. Investors at the peak of optimism or during structural shifts can easily factor in even better expectations and higher multiples, leaving substantial potential for further upside beyond this fundamental baseline.

Risks: The Illusion of Eternal Growth and the ‘Digestion Cycle’

Of course, not a single, even the most convincing investment thesis, happens to be full without a careful dismantling of hidden pitfalls. As an analyst, I am obliged to look not only at the growth potential, but also at what can go wrong. Setting aside general macroeconomic threats, such as a recession or geopolitical shocks, then the specific risks for AMD hide in the very structure of the AI market.

In my view, the main threat is the risk of a sharp slowdown of investments in the construction of new data centers by hyperscalers. Right now the market lives in a paradigm of extrapolation: investors believe that capital expenditures (CapEx) of technological giants will grow endlessly. However, the history of technologies teaches us that periods of unrestrained construction inevitably alternate with the so-called “digestion periods” (digestion cycles).

We can face a situation when corporations, having spent hundreds of billions of dollars on AI infrastructure, suddenly realize that their current capacities are fully sufficient to satisfy real demand. Boards of directors may demand from management to focus on the payback (ROI) of already purchased equipment, and not on new constructions. If this happens, capital expenditures will sharply slow down. And in the conditions of such a shrinking market or

“oversaturation” with capacities, companies often prefer to preserve budgets only for the main, historically verified supplier, cutting contracts with alternative vendors.

The second important risk, about which one must not forget, is pressure on margin. To aggressively win back market share from the incumbent, AMD, most likely, will have to use price levers. It is fully probable that the company will have to roll out its products with a certain discount in relation to analogs from the competitor. This means that although the revenue of AMD can grow at impressive rates, its gross margin can turn out to be under pressure. If a full-scale price war begins, this will inevitably tell on the growth rates of net profit, which can disappoint investors accustomed to the current high dynamic.

Conclusion: A Foundation for a Long-Term Portfolio

Summing up the results, I am inclined to consider that the current situation around AMD presents itself as a unique combination of factors for a thoughtful investor. We see a company which successfully overcame its main historical barrier — software isolation. We see real financial flows, billions of dollars of net profit, and the most powerful investments in R&D, which guarantee the support of its ecosystem.

Yes, the risks of oversaturation of the data center market exist, and they cannot be ignored. A sheer rally cannot last forever. However, returning to the thought with which I began this article: in the conditions of geopolitical turbulence and unpredictability of raw material markets, the shares of companies that are riding the wave of fundamental technological shifts look like the most reliable haven.

AMD today is no longer a risky bet on an outsider. I believe that this is the purchase of a share in a company that becomes a full-fledged, systemic element of the infrastructure of tomorrow. At the current valuation, the shares of AMD, in my view, may present a compelling case for further due diligence by long-term investors, whose planning horizon goes beyond the limits of one-two quarters.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.