/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

Fresh off a blockbuster IPO, SpaceX (SPCX) is already lining up its next big move. That’s not unusual. Companies that make splashy market debuts often head back to investors soon after, using debt sales to refinance short-term loans and raise fresh capital for their next growth phase. And when that growth story involves artificial intelligence (AI), the need for funding can get pretty big, pretty fast.

After SpaceX’s record-setting $75 billion IPO vaulted the company into the ranks of the world’s most valuable public corporations and underscored investors’ appetite for AI-related businesses, Elon Musk’s rocket, satellite, and AI giant is reportedly preparing a bond offering that could exceed $20 billion. It launched its first investment-grade bond offering, announcing an inaugural offering of senior unsecured notes in an SEC filing.

The proceeds are expected to refinance a bridge loan tied to SpaceX’s xAI acquisition. That facility, which comes due in September 2027, accounts for the bulk of the company’s $29.1 billion in long-term debt as of March 31, 2026. Any additional funds would provide more firepower for SpaceX’s ambitious expansion across rockets, Starlink, and AI infrastructure. Bank of America (BAC), Citigroup (C), JPMorgan (JPM), Goldman Sachs (GS), and Morgan Stanley (MS) are arranging investor calls.

So, what does this massive debt raise mean for SPCX investors? Let’s get into the details.

About SpaceX Stock

Founded in 2002, SpaceX has evolved from an ambitious rocket startup into one of the world’s most influential technology companies. Headquartered in Starbase, Texas, the company operates across several fast-growing industries, including space transportation, satellite connectivity, and AI. SpaceX is best known for its reusable Falcon rockets, Dragon spacecraft, and the next-generation Starship program, which are reshaping access to space.

Its Starlink unit provides high-speed satellite internet to consumers, businesses, and governments around the globe. Following its acquisition of xAI, SpaceX has also expanded deeper into AI, combining AI software with large-scale computing infrastructure. Together, these businesses have positioned SpaceX as a major player at the intersection of space, communications, and AI.

SPCX stock came out of the gate like a rocket after its blockbuster June 12 IPO. Shares opened at $150, well above the $135 offering price, and the excitement only grew from there. The stock jumped 19.6% on its first day and added 4.8% last Tuesday, eventually peaking at $225.64. For a few days, it seemed like the sky was the limit.

But what goes up fast can hit some turbulence. The rally began losing steam last Wednesday, with shares dropping about 5%, and the selling pressure only intensified. On June 22, the stock tumbled another 16.4%, bringing its three-day slide to roughly 25%. Even so, SpaceX still sports a market capitalization of about $2.02 trillion, making it one of the 10 most valuable public companies in America.

Several factors appear to be weighing on sentiment recently. For one, investors are starting to separate the sizzle from the steak. With annual revenue of $18.7 billion in 2025 and the company still losing money, some market veterans argue the stock got ahead of itself. Investors started looking beyond the excitement and asking whether the fundamentals could catch up with the lofty valuation.

Then came the sticker shock surrounding SpaceX's $60 billion all-stock acquisition of Anysphere, the company behind coding assistant Cursor. While the deal strengthens SpaceX’s AI ambitions, some felt the price tag was tough to swallow. Meanwhile, there are rumors brewing that SpaceX could eventually pursue Tesla (TSLA) .

Plus, with the Space’s first-ever investment-grade bond offering, uncertainty has increased. Debt deals can sometimes spook investors worried about rising interest costs.

Another cloud hanging over the stock is the lock-up expiration. According to 22V Research strategist Jeff Jacobson, insiders could potentially unload up to 44% of shares by early September, expanding the public float by roughly 900%. Current float is around 4%.

A Look at SpaceX’s Q1 Numbers and Outlook

SpaceX is not pinching pennies these days. Instead, the company is keeping its foot on the gas, pouring billions into businesses that management believes could pay off in a big way down the road. In the first quarter of 2026, SpaceX generated $4.7 billion in revenue, up 15.4% from a year ago. Much of that growth came from a growing base of Starlink subscribers and rising demand for AI products tied to X and Grok. The Space segment hit a few speed bumps, however, as launch timing and government contract schedules slowed growth.

SpaceX posted an operating loss of $1.94 billion and a net loss of $4.3 billion. But that does not tell the whole story. Adjusted EBITDA came in at $1.1 billion, showing the underlying business still has plenty of horsepower.

AI remains the company’s biggest bet. SpaceX spent a hefty $7.7 billion on its AI segment during the quarter, dwarfing the $1.33 billion invested in Connectivity and the $1.05 billion allocated to its Space business. As of March 31, 2026, long-term debt stood at $29.1 billion, while cash and equivalents totaled roughly $15.9 billion.

Looking ahead, Elon Musk is not thinking small. He believes SpaceX could generate an eye-popping $1 trillion in annual revenue by 2030. That’s a moonshot by any measure, and getting there won’t be a walk in the park. But Musk has made it clear that he is willing to sacrifice near-term profits and swing for the fences, betting that today’s spending spree could lay the groundwork for much bigger businesses tomorrow.

Analysts covering SpaceX anticipate the company’s fiscal 2026 revenue to be somewhere around $36.9 billion and rise to $68.3 billion in the next fiscal year. Fiscal 2026 losses are anticipated to be $0.89 per share and then shrink by 73% year-over-year (YOY) to $0.24 per share loss in fiscal 2027.

What’s Wall Street’s Take on SpaceX Now?

Elon Musk has set the bar sky-high for SpaceX, but Wall Street is keeping its feet on the ground. Morgan Stanley expects the company to generate about $330 billion in revenue by 2030, while Goldman Sachs is even more upbeat, forecasting $474 billion in annual sales by the end of the decade. Goldman also sees SpaceX’s AI business gaining steam, with revenue rising from $15.6 billion in 2026 to $34.5 billion in 2027 before really hitting its stride and reaching $322 billion by 2030.

Those are eye-popping numbers by any measure, but they still fall well short of Musk’s trillion-dollar revenue goal. To pull that off, SpaceX would need to expand revenue at a blistering 122% CAGR over the next five years.

That’s a tall order. The company will have to launch more rockets, expand Starlink’s reach, and carve out a bigger piece of the fiercely competitive AI market. In short, SpaceX has plenty on its plate. Whether Musk’s moonshot target becomes reality remains anyone’s guess, but the company will need to keep the pedal to the metal.

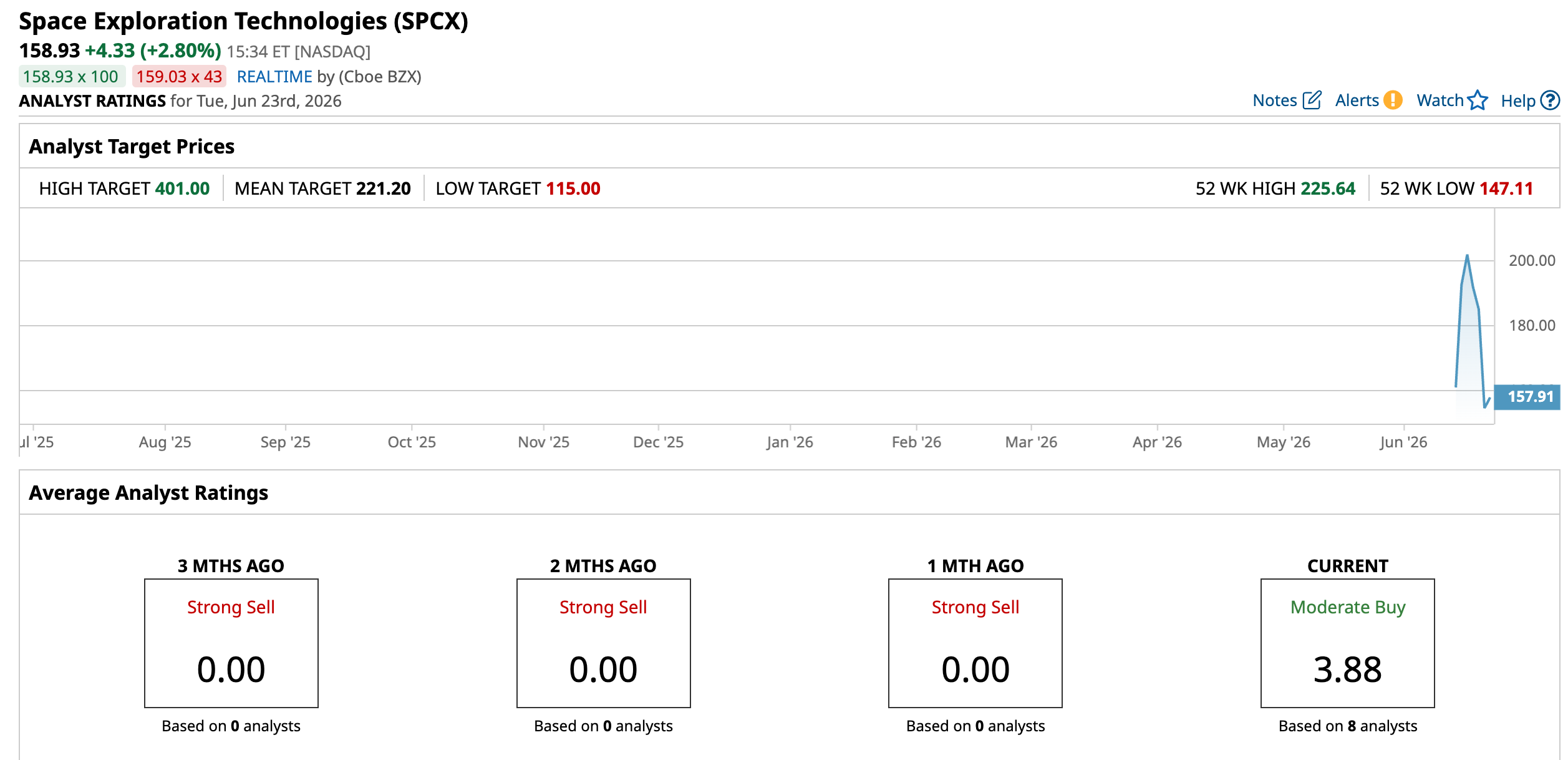

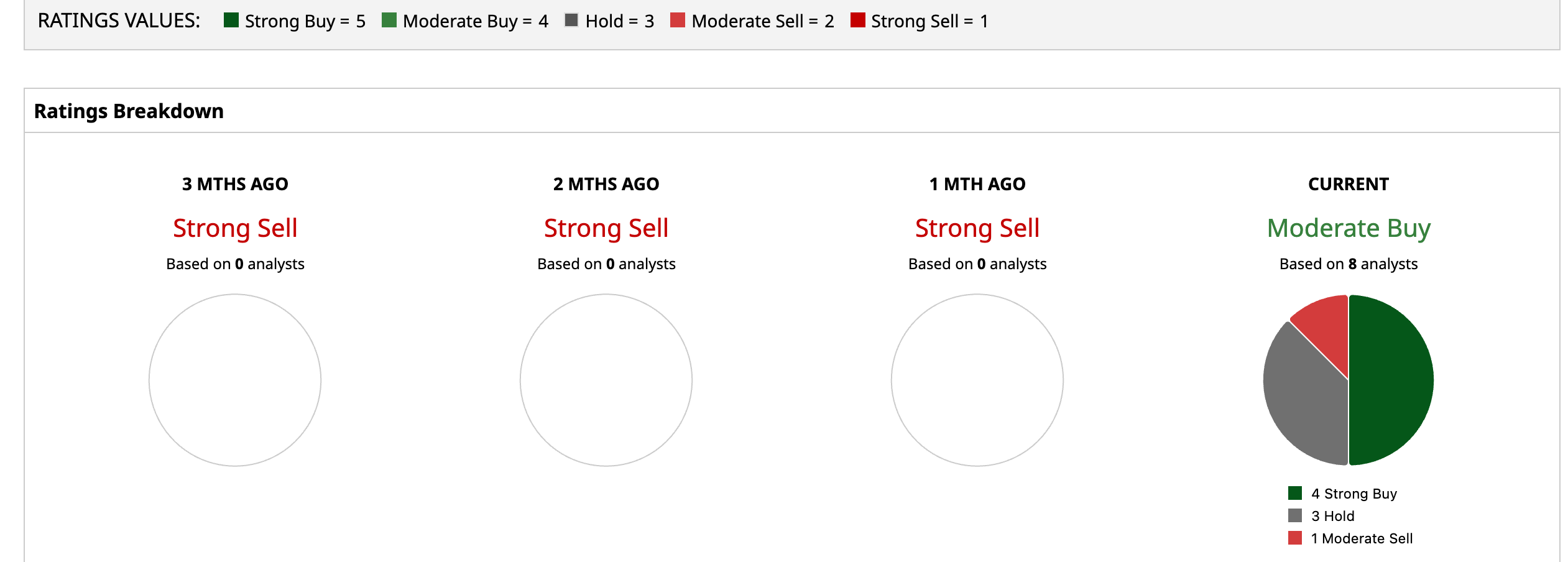

Overall, SPCX stock carries a “Moderate Buy” rating. Of the eight analysts covering the stock, four are pounding the table on a “Strong Buy,” three are playing it safe with a “Hold,” and the remaining one is waving a cautious flag with a “Moderate Sell.”

The stock was flying high last week after its debut, trading above both the average analyst target and even Wall Street’s most bullish forecast set last week. Since then, the dust has settled a bit. At current levels, SPCX has come back down to earth, and now the average price target of $221.20 suggests that the stock has rebound potential of 39.2%. Meanwhile, the Street’s highest price target of $401, set by Arete Research analyst Andrew Beale, implies SPCX could rally as much as 152.3%.

Final Thoughts on SPCX Stock

SpaceX’s planned bond sale looks less like a distress signal and more like a company loading up the fuel tanks for its next mission. Refinancing the bridge loan should ease near-term pressure on the balance sheet, while fresh capital could help SpaceX double down on AI, grow Starlink, and continue ramping up its launch operations.

Even so, investors should not expect a smooth ride. More debt means higher interest costs, and with the stock already coming off its post-IPO highs, investors are shifting their attention from big promises to real results. As the saying goes, the proof is in the pudding.

For long-term believers, the bond offering could be a sign that SpaceX is thinking several moves ahead and doubling down on its biggest growth bets. But in the near term, between valuation concerns, insider share unlocks, and a growing debt load, SPCX investors may need to buckle up. The company still has the wind at its back, but now it has to show how the bold plans translate into results.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)