For years, Silicon Valley’s default answer to rising costs was to send more work offshore. That playbook is now being torn up in real time. Opendoor Technologies (OPEN) is shrinking its global footprint just as its technological ambitions get bigger.

Last week, the U.S. home‑buying company said that it will shut down its India operations and let go of nearly 250 employees. That decision comes less than two years after it called India a key hub for engineering and operations.

The company is now being reshaped by CEO Kaz Nejatian, who joined from Shopify (SHOP) last year. He has laid out a push to rebuild Opendoor around software and automation, saying the business is being remade as a software and AI company.

As Opendoor pulls back from India to double down on automation at home, is this the moment to lean into OPEN stock? Or should investors treat the new AI narrative as one more opportunity to sell into strength? Let’s take a closer look.

Opendoor's Financial Pulse

Opendoor runs a digital “iBuying” platform that buys and sells homes using data‑driven pricing and instant offers. It aims to make real estate deals simpler and faster. The company is headquartered in Tempe, Arizona, with a corporate hub in San Francisco, California, operating across major U.S. housing markets.

At around $4.30 per share as of June 22, OPEN stock is down 26% year-to-date (YTD) but still up more than 700% over the past 52 weeks.

Opendoor is valued at about $4.3 billon by market capitalization and trades at roughly 0.98 times sales versus a real estate sector median of about 5 times. Its price‑to‑book ratio of 4.5 times also compares to a sector median of 1.6 times, which shows the stock sits close to its revenue base but at a richer multiple to its equity.

The latest numbers help explain why the India layoffs and shift in focus matter so much right now. In its most recent quarter, which ended in March 2026, Opendoor reported a GAAP loss per share of $0.18 against an estimate of -$0.07, a negative surprise of 157%. Q1 revenue came in at $720 million versus analyst expectations of $664.5 million, an almost 38% drop from a year earlier but still a more than 8% beat versus the consensus estimate.

The company reported adjusted EBITDA of -$31 million, which works out to a -4.3% margin and marked a 3% year-over-year (YOY) slide. Operating margin was -22.1% compared with -4.9% in the same quarter last year, showing that costs are still eating into each sale.

Operating cash flow was -$246 million in March 2026 while net cash flow came in at -$234 million. Free cash flow was -$250 million, a slight improvement from -$283 million a year earlier but still firmly in negative territory.

The Driving Force for Opendoor

Opendoor recently got a meaningful boost with its inclusion in the Russell 3000 Index as part of the 2026 annual reconstitution. This change takes effect after the U.S. market closes on June 26. The listing should bring wider visibility and likely new passive buying from index funds and exchange-traded funds (ETFs) that track the index, along with potential placement in either the Russell 1000 or Russell 2000 and related growth and value style indices.

There is also a big potential policy tailwind building in the background. A planned $200 billion government push to support housing would see President Donald Trump direct federal money into mortgage bonds. That move is expected to lower mortgage rates, cut monthly payments, and make homes more affordable across the United States. The result would be more deals and better liquidity in the housing market.

Taken together, these developments point to growing support behind OPEN stock, both from market structure and from a possible boost to its core business.

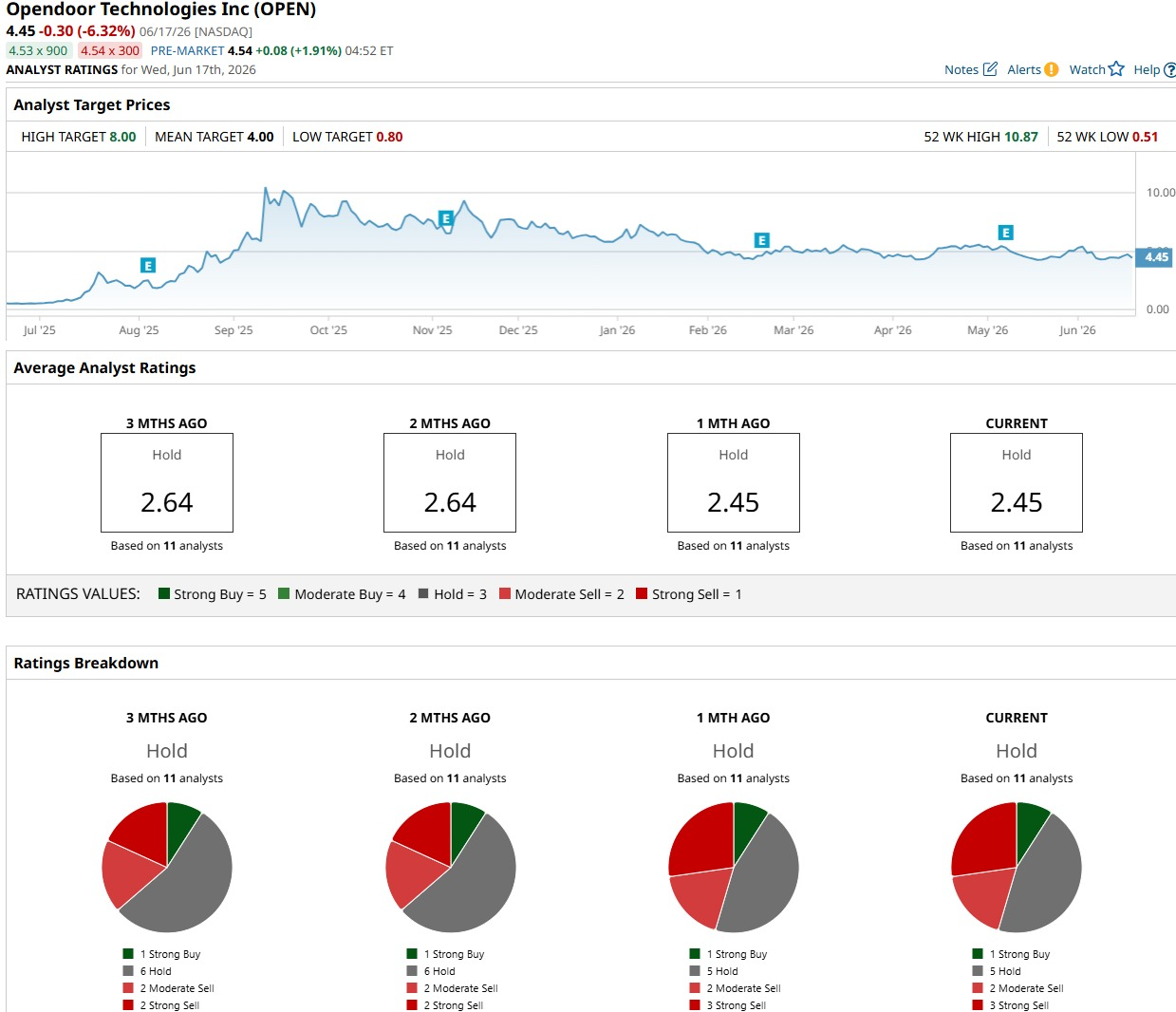

What Does Wall Street Think of OPEN Stock?

Analysts watching Opendoor’s restructuring still see losses ahead. The next earnings release is set for Aug. 4, and the current consensus for the June quarter is EPS of -$0.05. That compares with -$0.03 a year earlier and points to a YOY decline of about 67%.

Rating changes over the past year show that doubt about the company's model did not start with the India layoffs. In 2025, Keefe, Bruyette & Woods cut OPEN stock to “Underperform,” while Citigroup moved shares to a “Sell” rating. Those decisions were driven by worries about ongoing losses, the strategy, and how Opendoor handles housing‑cycle swings and a capital‑heavy business.

Across the wider analyst group, the stance has settled into a cautious middle. The latest read from 11 analysts comes out to a consensus “Hold” rating. The average price target sits at $3.95 per share, which implies about 8% potential downside from current levels.

Conclusion

Opendoor’s job cuts in India and shift toward a new model in the U.S. leave OPEN stock looking like a speculative turnaround play rather than a straightforward buy. With losses still expected and a consensus “Hold” rating, the stock is more likely to chop around news and headlines than launch into a strong uptrend. The near‑term outlook points to sideways or slightly weaker trading unless the company starts executing better and housing numbers come in stronger than expected.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)