In general, the semiconductor space has had a rough 2026. The year started strong with AI hype pushing chip stocks higher, but things began to slip in early June after Broadcom (AVGO) gave a weaker-than-expected outlook for chip sales, triggering a sector-wide rout. That sell-off dragged the S&P 500 Index ($SPX) and Nasdaq 100 ($IUXX) to multi-week lows as investors started questioning the true sustainability of the AI rally. The pressure didn’t ease either. By June 23, another sharp drop in chip stocks pulled the Nasdaq 100 down as much as 3.29% in a single session, with concerns building around valuations and AI spending.

While all that was happening, dividend stocks quietly went the other way. Names that are usually overlooked in fast-moving markets started putting up strong gains, even as the broader indexes struggled. Texas Instruments (TXN) stands out here. The stock is up 79.6% year-to-date (YTD) as of late June 2026, far from its $174.91 low back on January 2, and now ranks among the best-performing dividend stocks this year. At the same time, it’s still paying investors, with a forward annual dividend of $5.68 and a yield of 1.87%.

So what’s really driving a long-established analog chipmaker like Texas Instruments to outperform so many of its semiconductor peers this year?

Financials Behind the Surge

Texas Instruments makes analog and embedded chips that go into everyday systems like cars, industrial machines, and electronics, areas where demand tends to be steady over time.

Shares are up 51.71% over the past 52 weeks, well ahead of the broader market S&P 500 which has 20.9% gains over the past year.

The stock trades at a forward price-to-earnings Non-GAAP ratio of 38.97 times, compared to the sector average of 23.78 times, showing investors are willing to pay up for its consistency.

It also still works as an income play. The stock yields about 1.85%, above the tech sector average of 1.37%, with a quarterly dividend of $1.42 and a 22-year streak of increases. Even so, the forward payout ratio is high at 94.15%, meaning most of its earnings are going back to shareholders.

The latest results back up the rally. First-quarter revenue amounted to $4.83 billion, up 18.6% year-over-year (YOY) and ahead of estimates. EPS was $1.68, beating expectations by more than 23%. Margins improved too, with operating margin at 37.5% and adjusted EBITDA hitting $2.46 billion, a 50.9% margin. Free cash flow jumped to $1.40 billion from negative levels a year ago, while inventory levels came down, a sign demand is stabilizing. Looking ahead, the company expects $5.2 billion in Q2 revenue and $1.91 in EPS, both above what analysts were expecting.

Core Drivers of Long-Term Growth

Texas Instruments is pushing growth through a steady stream of new products. In battery tech, it rolled out the BQ79826Z-Q1, a new monitor designed for electric vehicles and energy storage systems. It can track 44% more channels than older versions, which means fewer components are needed, and overall system costs come down. It also spots early signs of thermal runaway inside battery cells, which is a big deal for safety. The company showed this off at PCIM 2026 in Nuremberg.

It’s also updating its education lineup with the TI-84 Evo Graphing Calculator, the most advanced version of a product that’s already widely used. It runs three times faster, has 50% more graphing space, and comes with a redesigned keypad.

Features like points of interest trace and improved graphing tools make it easier for students to work through problems. It’s built without Wi-Fi to limit distractions and is approved for major exams like the ACT, SAT, IB, and AP, so students can use it for years.

On the industrial side, Texas Instruments introduced new power modules using its IsoShield packaging. These deliver up to three times the power density of traditional designs while cutting solution size by as much as 70%. They’re aimed at data centers and electric vehicles, helping reduce both cost and design time. The company presented these at APEC 2026 in San Antonio.

What Analysts Expect Next

Texas Instruments is set to report earnings on July 28, 2026, and expectations are already strong. For the current June quarter, analysts see EPS coming in at $1.90, up from $1.41 a year ago, which is a 34.75% jump. That growth is expected to continue into the September quarter, with estimates at $2.07 compared to $1.48 last year, a 39.86% increase. For the full year, projections are at $7.66 for 2026, pointing to 40.55% growth.

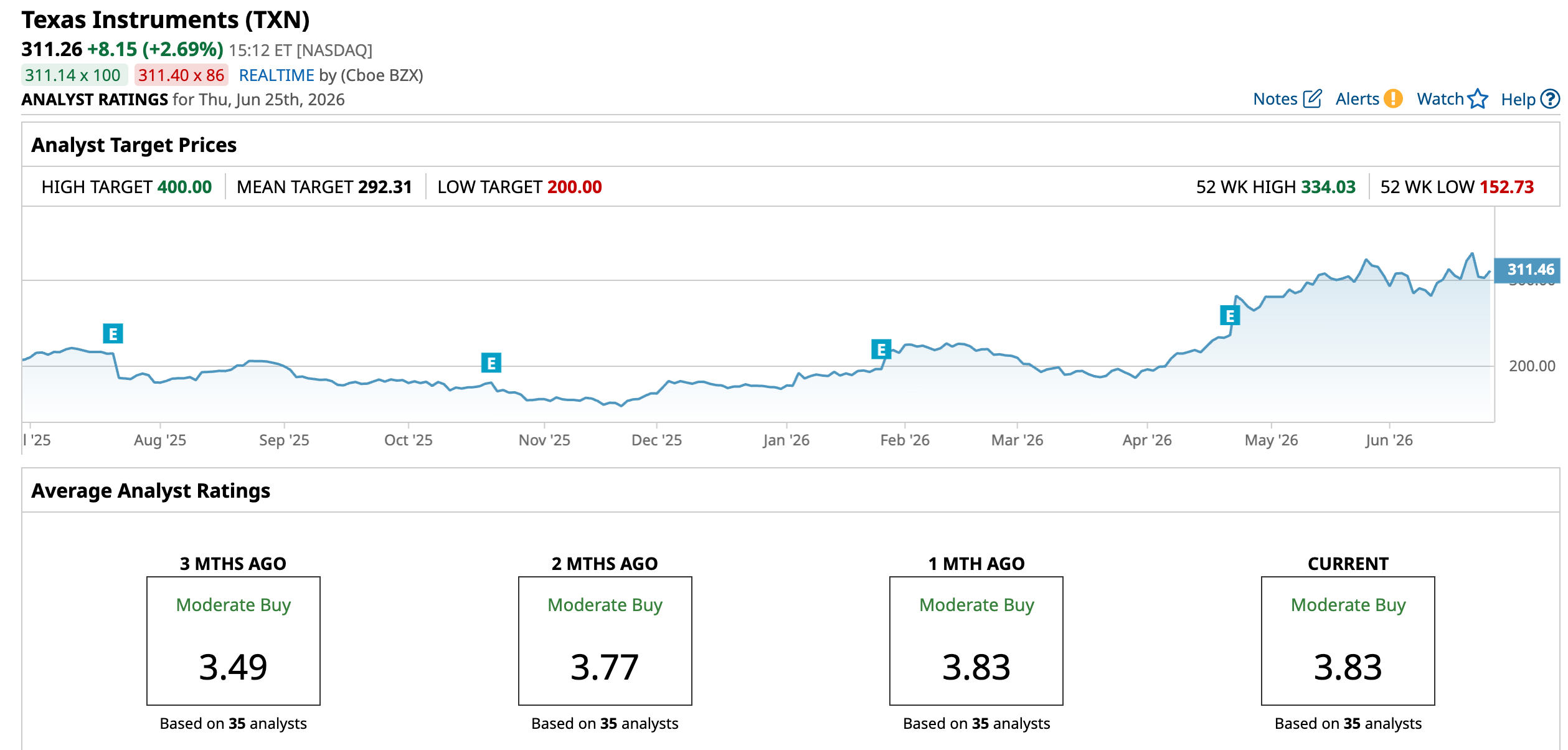

Analysts have been backing that trend. Argus Research’s Jim Kelleher kept a “Buy” rating in April with a $320 price target, pointing to steady demand. In June, Stifel’s Tore Svanberg also maintained a "Buy" rating and raised his target from $340 to $360, driven by strength in industrial and automotive markets. Bank of America and Rosenblatt followed with targets of $370 and $330 as the stock pushed higher.

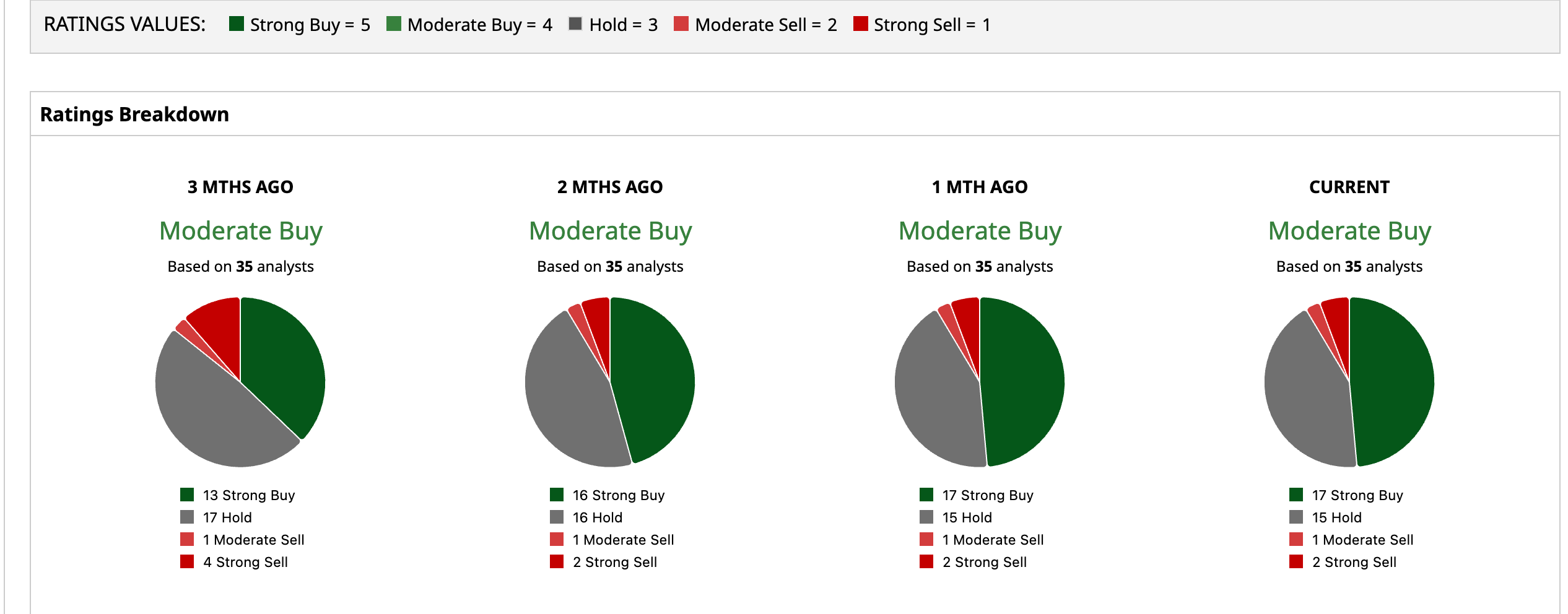

Nevertheless, of 35 analysts covering Texas Instruments, a consensus rate it a “Moderate Buy,” with an average price target of $292.31. That’s about 6.1% downside of TXN's trading price now. The Street-high target price of $400 means the stock could climb 28.5% higher from here.

Conclusion

Texas Instruments’ outperformance in 2026 comes down to a simple mix of strong earnings delivery, durable end-market demand, and a reliable dividend that continues to attract investors even in a shaky market. While the stock’s premium valuation and muted near-term upside based on consensus targets suggest it may not surge at the same pace from here, the underlying fundamentals still point to steady growth rather than a sharp reversal. The most likely path forward looks like more measured gains, supported by earnings momentum and income appeal, especially if broader market volatility persists.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)