/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

Artificial intelligence (AI) has sparked a new gold rush across the tech industry. Even smaller infrastructure players are landing billion-dollar contracts. Among them is Applied Digital (APLD), which has grown from a relatively small data center operator to one of the market's most carefully watched AI infrastructure providers. Recently, it landed a 15-year lease worth about $5.2 billion with a U.S.-based investment-grade hyperscaler, validating its business model. In a highly competitive semiconductor industry, winning your client’s trust with long-term contracts is a competitive advantage.

APLD stock has surged a massive 88% year-to-date (YTD), outperforming most tech heavyweights and the overall market. Let’s find out if Applied Digital's stock is a good buy now.

Applied Digital Is Building the AI Infrastructure Empire That Is Being Overlooked

Valued at $13.02 billion, Applied Digital is an AI infrastructure provider. It builds and operates large, power-intensive data centers that hyperscalers and AI companies use to run massive clusters of GPUs. Instead of creating AI models itself, Applied Digital provides the land, buildings, power infrastructure, cooling systems, and networking needed to support the massive AI workloads.

What has worked in Applied Digital’s favor is recognizing way early that AI workloads would require far larger and more power-dense facilities than traditional data centers. About two years ago, it broke ground on its first 100-megawatt AI-focused facility before the current AI infrastructure boom began. That gave the company a valuable first-mover advantage in liquid-cooled, high-density AI facilities. What’s even more remarkable is that this 100-megawatt facility accounts for only one-tenth of the total capacity currently under construction, highlighting the enormous scale of future expansion plans.

Adding to the list of green flags, on June 8, Applied Digital inked a 15-year lease worth approximately $5.2 billion with a U.S.-based investment-grade hyperscaler at its Delta Forge 2 AI Factory campus. The lease covers 210 megawatts of AI computing capacity under a take-or-pay structure. Additionally, if all renewal options are exercised, the total contract value could reach close to $12.7 billion over 30 years. Following the deal, the company’s committed base-term lease revenue has now climbed to $36 billion, with potential revenue rising to roughly $86 billion if all renewals are exercised. The company now has five campuses, totaling around 1.4 gigawatts of IT load and 2.15 gigawatts of grid-connected power. For Applied Digital, this means predictable long-term cash flows and validation that hyperscalers trust the company to deliver mission-critical AI infrastructure.

This new contract comes after Applied Digital reported a robust third quarter of fiscal 2026. The AI infrastructure business is contributing meaningfully to revenue, which increased by 139% year over year to $126.6 million.

A Massive AI Data Center Buildout Is Underway

Applied Digital's growth strategy revolves around building large-scale AI campuses capable of supporting hyperscale customers. Besides the recently announced Delta Forge 2 campus, during the third quarter, Applied Digital had already launched Delta Forge One, a 300-megawatt AI factory campus located in a strategic Southern U.S. market. The development covers about 600 acres, with initial operations set to commence in mid-2027.

During the Q3 earnings call, management highlighted that at Polaris Forge 1, its 400-megawatt campus leased to CoreWeave (CRWV), the first 100-megawatt building is already operational. Meanwhile, construction continues on two additional 150-megawatt facilities. Applied Digital's first 100-megawatt AI data center contributed a full quarter of recurring lease revenue during the third quarter.

The company's second major project, Polaris Forge 2, consists of a 200-megawatt investment-grade hyperscaler campus and is also progressing well. Applied Digital expects revenue to ramp significantly over the next 12 months as additional projects come online. Combined, these projects reveal how aggressively the company is expanding to meet rising AI infrastructure demand.

Over the last five years, Applied Digital has secured approximately $16 billion in contracted lease revenue. The company is also confident of exceeding its long-term goal of generating $1 billion in net operating income (NOI) within the next five years.

Is APLD Stock a Buy Now?

Applied Digital appears to be growing into a major AI data center developer with significant long-term growth potential. On the flip side, the company is not profitable yet. However, management is confident that hundreds of megawatts currently under construction will come online over the next few years, causing revenue and profits to dramatically surge. Like most growth stocks in a highly competitive industry, Applied Digital is a high-risk, high-reward investment case. For investors willing to put up with this volatility, Applied Digital's stock appears to offer substantial long-term upside and remains an attractive buy for those seeking exposure to the rapidly expanding AI data center market.

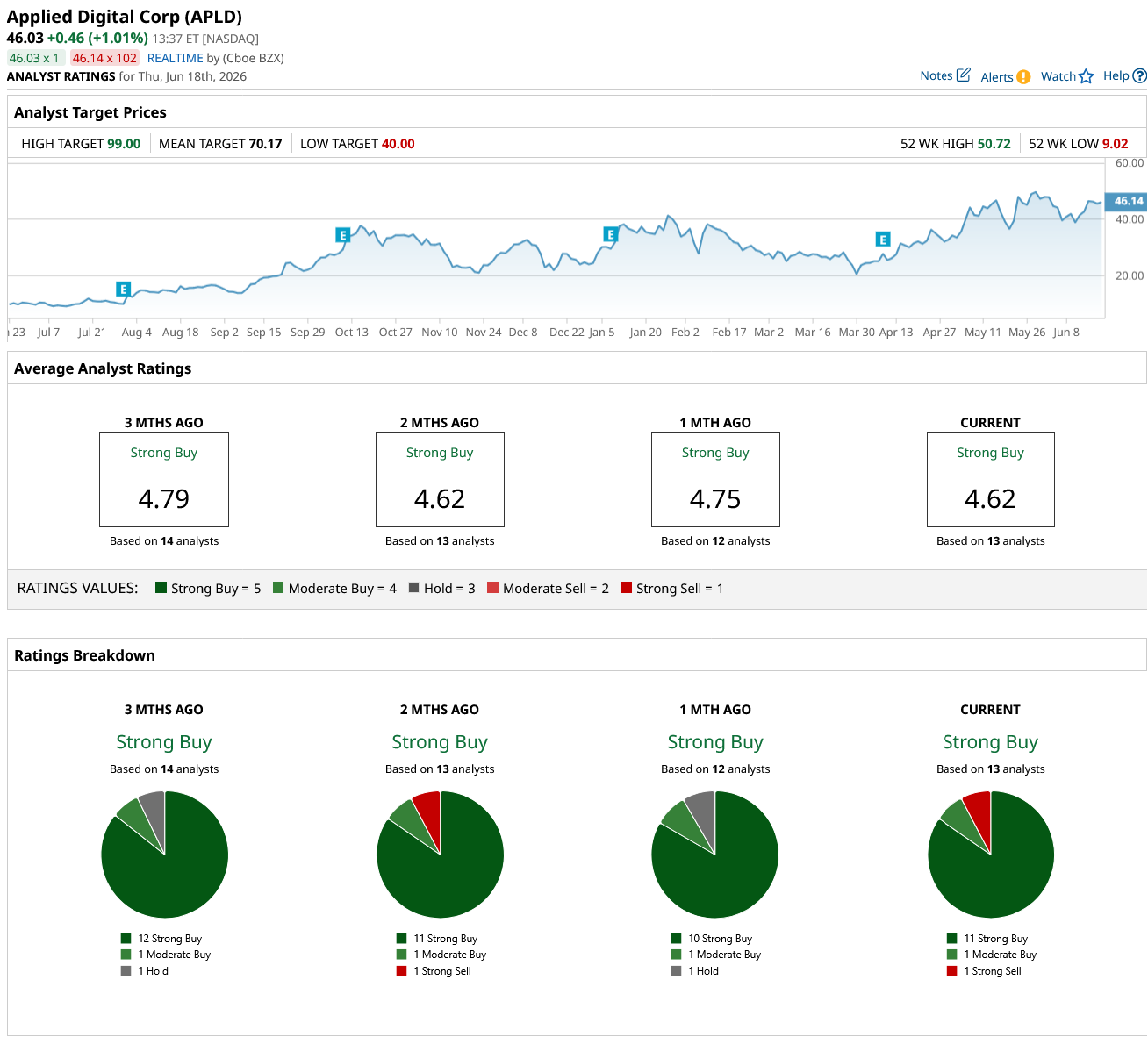

Overall, on Wall Street, APLD stock is a “Strong Buy.” Of the 13 analysts covering the stock, 11 rate it a “Strong Buy,” one says it is a “Moderate Buy,” and one rates it a “Strong Sell.” The average target price for the stock is $70.17, which implies APLD stock can climb by 52% from current levels. Plus, the high price estimate of $99 suggests the stock has an upside potential of 115% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)