/AI%20(artificial%20intelligence)/Image%20of%20Cloud%20Computer%20Engineer%20Coding%20In%20Server%20Room%20In%20Data%20Center%20by%20Andrey%20Popov%20via%20Shutterstock.jpg)

One of the greatest challenges for artificial intelligence stocks is that it’s an expensive business. Hyperscalers like Amazon (AMZN), Alphabet (GOOG) (GOOGL), Microsoft (MSFT), and Meta Platforms (META) are spending $700 billion this year on AI infrastructure to create the computing capacity needed to meet an ever-increasing demand.

That strain is also felt by companies like Super Micro Computer (SMCI), which recently announced it was seeking $7 billion in financing to support an AI server backlog of $39 billion. The announcement drew concern among both analysts and investors, and the stock is down sharply.

However, we’ve seen this kind of selloff before in the AI space—each of the aforementioned hyperscalers dipped in the first quarter on fears that their capex spending was too aggressive. And all four showed dramatic improvement in Q2.

Can Supermicro, as its often called, follow the same script?

About Super Micro Computer Stock

Super Micro Computer, which is based in San Jose, California, plays an important role in the AI space. The company creates custom server motherboards, liquid-cooling racks, and other AI infrastructure required to house bundled semiconductors that are working together to complete AI tasks. Its server solutions are used in data centers as well as for high-performance computing, high-end workstations, networks, and standalone server installations.

The company’s shares have been a disappointment, down 25% in the last year, while the S&P 500 ($SPX) rose 27%, and the S&P 1500 Information Technology sector is up more than 55%.

SMCI stock is currently trading at a low forward price-to-earnings ratio of 11.8, which is less than half of its three-year mean of 22.9, indicating that the shares are cheap right now. But the stock performance makes Supermicro a contrarian pick right now for many investors.

The most recent headwind is the company’s announcement that it was seeking up to $7 billion in funding to pay for a backlog of $39 billion in orders from more than 20 companies. The proposed offerings would include $5 billion in stock underwritten by investment banks, including $1.25 billion in new common shares and $3.75 billion from depository shares. In addition, the company is proposing a $2 billion at-the-market offering, meaning the company would sell up to that level over time.

The underwritten offer will result in 45.45 million shares of common stock at a public offering price of $27.50 per share and 75 million depositary shares, each representing a 1/20th interest in a share of newly issued 7% series A mandatory convertible preferred stock at a public offering price of $50 per share.

But the dilution in shares isn’t being received well by investors. SMCI stock, which was trading at $44.90 before the company’s announcement, fell 30.6% in just five days as the company rolled out the details of the offering in announcements on June 9 and June 11.

Supermicro Beats on Earnings

Supermicro reported solid earnings for its fiscal third quarter (ending March 31). Revenue of $10.2 billion was up from $4.6 billion a year ago, and net income was $483 million versus $109 million in the fiscal third quarter of 2025. Earnings per share were $0.72, which soundly beat analysts’ expectations for EPS of $0.55.

Notably, SCMI’s revenue dropped 19% on a sequential basis, which management attributed to component shortages and customer site readiness delays.

“Despite the industry-wide shortage of key components, including CPU, GPU, and memory, our business continues to grow and expand. Indeed, our backlog is now at another record high,” CEO Charles Liang said.

The company is also expanding its production by ramping up facilities in Taiwan and Malaysia and plans to build a new facility in Silicon Valley that will bring Supermicro’s footprint in the San Francisco to nearly 4 million square feet.

Supermicro issued fourth-quarter and full-year guidance that calls for net sales of $11 billion to $12.5 billion in Q4 and $38.9 billion and $40.4 billion for fiscal 2026.

Supermicro Addresses Legal Issues

The company also distanced itself in the earnings call from co-founder and board member Yih-Shyan “Wally” Liaw, sales manager Ruei-Tsang “Steven” Chang, and contractor Ting-Wei “Willy” Sun, who were indicted by the U.S. government in March on charges that they allegedly attempted to divert $2.5 billion in Nvidia (NVDA)-powered AI servers to China, which would be a violation of U.S. export controls.

Liang said all three were terminated, and the company is cooperating with the Justice Department. “The alleged actions of a few individuals do not define us,” he said.

Liang said the company is not under indictment and is not a target of the investigation, and he believes that the company will not need to restate its earnings. The company also retained an outside law firm and a forensic firm to conduct an independent investigation.

“We will take to heart the results of the independent investigation and look at that as an opportunity to grow and strengthen,” he said.

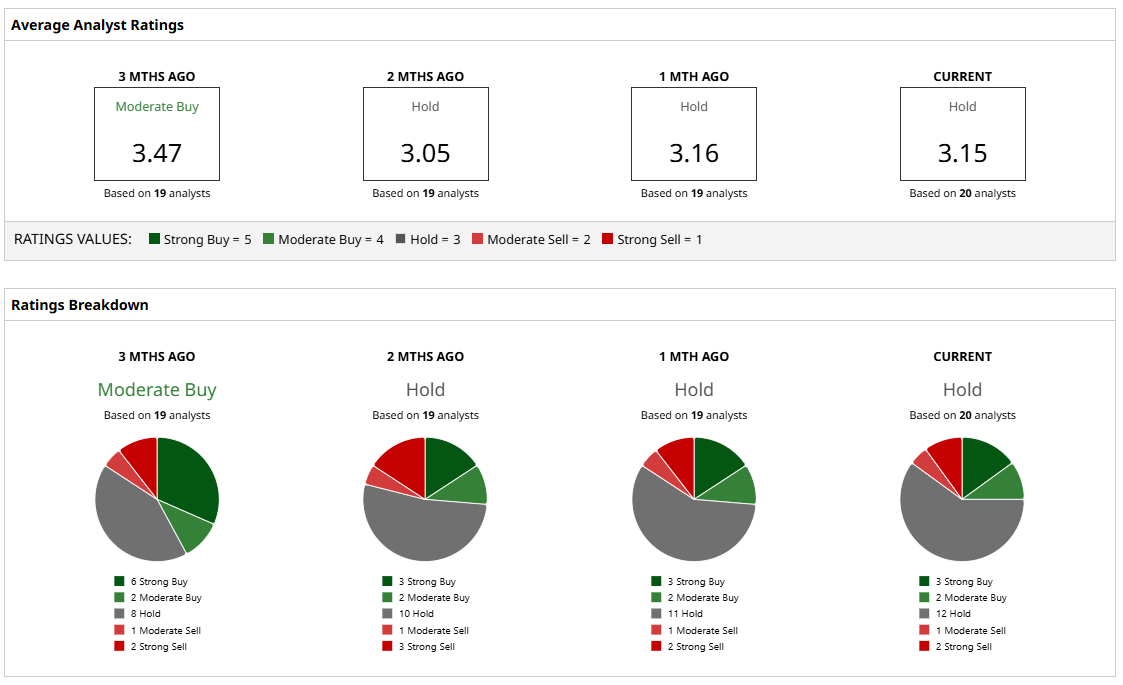

What Do Analysts Think of SMCI Stock?

Considering the legal issues and the upcoming dilution of shares, analysts are understandably reserved. Twenty analysts who cover the stock have a consensus “Hold” rating on the stock, down from “Moderate Buy” three months ago. Only five have “Buy” ratings and three have “Sell” ratings.

However, the mean price target of $38.87 represents a potential upside of nearly 25%, which plays into the idea that SMCI stock is somewhat undervalued right now.

As said before, buying Supermicro's stock today is a contrarian play. While hyperscalers like Alphabet are making similar moves to raise money—the owner of Google is selling $80 billion in shares to pay for its AI ambitions—Supermicro comes with a lot more baggage. The company was also delisted from the Nasdaq in 2018 for not filing financial reports in a timely manner and then was fined in 2020 by the Securities and Exchange Commission for accounting violations.

So, it’s no solid bet that Supermicro will be able to follow the Alphabet playbook. A measured stance by investors—and a skeptical eye—is more appropriate.

On the date of publication, Patrick Sanders had a position in: NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)