The following is a recent report in The Spread Trader newsletter, published by Klarenbach Research.

My colleague, Brent Futz, a former WCE floor trader with 40 years of experience trading commodities, leads that publication.

May The Oat Futures Contract R.I.P.

A number of years ago, I was approached by a large firm to trade oats on their behalf on the floor of the CBOT.

Since then, I have monitored the market mostly for entertainment value.

The recent trade in the contract has gone beyond entertainment and has raised red flags about its future.

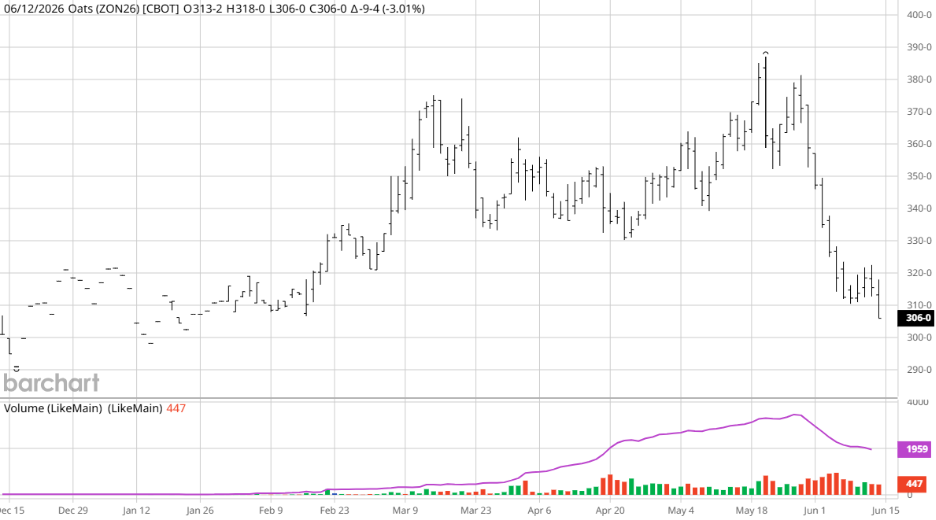

Chart 1 shows the July Oat futures contract over the past 6 months.

The recent sharp decline occurred at a time when the grains and oilseed market experienced similar losses.

After establishing a contract high of $3.85 on May 20th, the market experienced a violent sell-off to approximately $3.05.

The sell-off may be dismissed as price discovery, but what happened afterward should raise red flags.

Chart 1: July 2026 Oat Futures Contract

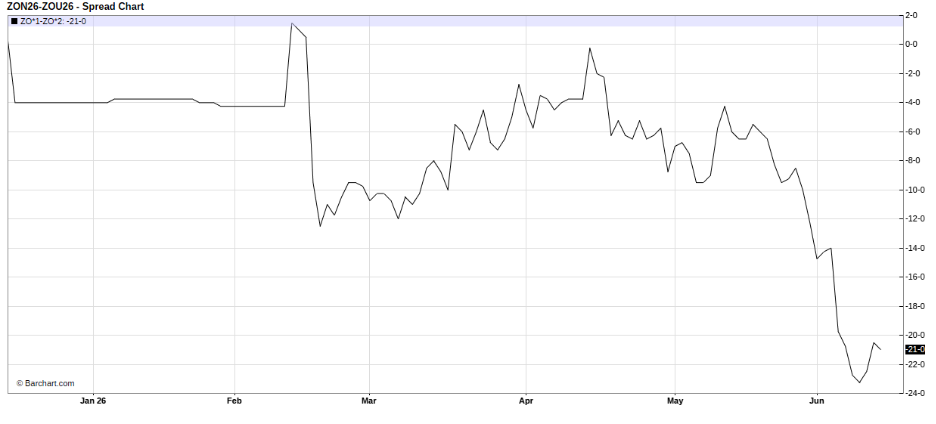

To add insult to injury, the July long is currently rolling their position forward into September at a substantial contango, the July/Sept spread now trading at $.21 under.

To put the consequences of the large contango into perspective, the long is being forced to roll its position at a contango of approximately $ 0.10 per month.

If the large contango continues over the course of a year, the long is increasing its average price by $1.20. For example, after a year, the breakeven of the long-established at $3.85 is now $5.05, an unlikely proposition.

Advantage goes to the short; a significant contango substantially shifts the playing field in favour of the short.

Chart 2: July2026/Sept 2026 Oat Futures Spread

It is difficult to determine whether the large contango will persist, but it poses a significant risk to the perpetual long.

The effects of a large contango are not conjecture; I have been involved in a contract faced with similar market dynamics.

A well-known commodity fund established a significant long position, rolled their position at full carry for two years before liquidating at the same price that the position was established.

In the end, there was a significant transfer of wealth from long to short.

The contract did not provide an effective hedge for the long or an effective strategy for the fund. \

Finally, the contract was delisted, never to return.

Time will tell if the oat futures contract suffers the same fate.

The above analysis emphasizes the role a spread should play in any trading strategy, technical or fundamental.

I have traded commodity spreads for 43 years, mostly as a local.

Please feel free to contact Brent with questions and comments at b.futz@hotmail.com

Brent covers this technical setup and specific price targets in depth in the The Spread Trader.

Join 3,500+ farmers getting sell signals and technical roadmaps here:

Trent Klarenbach, BSA AgEc, PAg, publishes the Klarenbach Grain Report, Klarenbach Special Crops Report and The Spread Trader newsletters.

Klarenbach Research

Sign up below for a FREE trial of our newsletters

Wheat Canola Corn Spring Wheat Hard Red Winter Oats

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20in%20modern%20server%20room%20data%20center%20by%20Sashkin%20via%20Shutterstock.jpg)

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)