/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

Analysts keep raising their Nvidia Inc (NVDA) FY 2027 revenue forecasts and their NVDA price targets. This implies that free cash flow (FCF) will be higher than expected. NVDA stock could be worth $330, +61% higher. This is based on conservative FCF margin and FCF yield assumptions.

NVDA closed at $204.87 on Thursday, June 11, up 2.2%. But in the last three weeks, since Nvidia released its fiscal Q1 earnings on May 20, NVDA has dropped $18.60 from $223.47 (-8.3%).

But based on its strong free cash flow (FCF) outlook and higher analyst revenue forecasts, NVDA could be worth considerably more over the next year.

Strong FCF Outlook

For example, analysts now project revenue next year will be $551.66 billion. That's up from $540.45 billion on May 25 when I wrote my last Barchart on Nvidia, “Nvidia Hikes Its Dividend and Buybacks Based on Surging FCF - Is NVDA Too Cheap?”

Nvidia's FCF margin last quarter was 59.53%, and its trailing 12-month (TTM) FCF margin was 47%. That implies that, on average, its FCF margin next year could be at least 53.3%:

$551.66b FY 27 revenue x 0.533 = $294 billion FCF

That is over 147% higher than its past year's $119.1 billion FCF. Moreover, even on a run-rate basis, its FY 27 FCF would be higher. For example, last quarter, Nvidia made $48.587 billion in FCF, so its 4-quarter run rate is $194.3 billion.

That means its FCF could rise $100 billion next year, or +51.5% (i.e., $294b /$194b -1 = 0.515 = 51.5%).

This could push its valuation significantly higher.

Higher Price Targets

One way to value NVDA is to use an FCF yield metric. For example, its TTM $119 billion represents 2.39% of its existing market value of $4,962 billion, as calculated by Yahoo! Finance.

However, that's looking backward. The market thinks forward. For example, the $194 billion in run-rate FCF from last quarter represents a FCF yield of 3.9%

$194.3b / $4,962b = .03916 = 3.92%

That is equal to a multiple of 25.5x FCF (i.e., 1/0.03915 = 25.5x).

So, over the coming 12 months, it's likely that NVDA will have a market value of almost $7.5 billion:

$294b FY 27 FCF x 25.5 = $7.497b mkt value

That is 51% higher than Nvidia's present market value of $4,952 billion. As a result, my new price target is 51% higher than today's price:

1.51 x $204.87 = $309.35 per share

Other analysts agree. For example, Yahoo! Finance shows that 62 analysts now have an average price target (PT) of $298.42. That is higher than three weeks ago, when I showed that Yahoo! Finance showed average analysts' PTs of $294.22.

In addition, Barchart's mean survey PT has risen from $296.20 to $303.71 today. Similarly, AnaChart, which tends to cover more recent analyst write-ups, now has an average of $303.64 from $274.30 three weeks ago.

So, analysts have been raising both their revenue forecasts and their price targets. That could indicate NVDA is undervalued, as I have shown.

However, there's no guarantee this will happen. After all, NVDA has been volatile. One way to play NVDA is to set a lower buy-in price by shorting out-of-the-money (OTM) puts. That way, investors can earn income while waiting to buy at a lower price.

Shorting OTM NVDA Puts

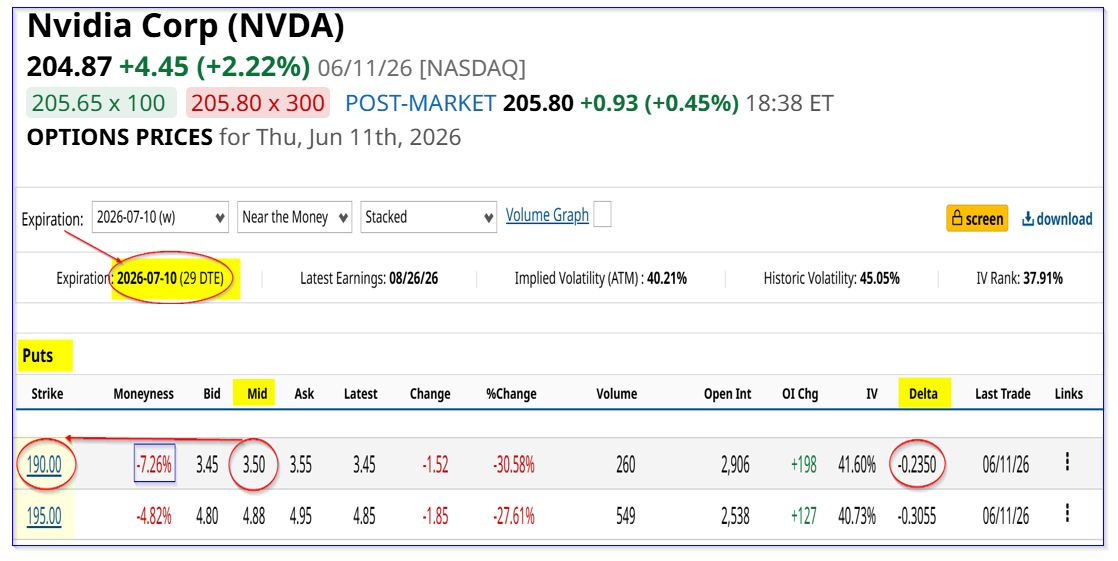

For example, the July 10 expiry $190 strike price put option has a midpoint premium of $3.50. That strike price is over 7% below Thursday's closing price of $204.87, and the delta ratio is low at just 23.5%. This implies a low probability that NVDA will drop to $190 in the next month.

Moreover, the premium received immediately represents a yield of over 1.84% to the short-seller of these puts over the next month: $3.50/$190.00 = 0.01816 = 1.842%.

That means that after an investor posts $19,000 in collateral with their brokerage firm, the account can immediately receive $350 after entering an order to “Sell to Open” these put options. Moreover, the breakeven point is almost 9% lower:

$190.00 -$3.50 = $186.50

$186.50 / $204.87 -1 = -8.97%

The point is that shorting OTM NVDA puts allows an investor to earn income even if NVDA stays flat. And if it drops by 7.3% to $190, the investor gets to buy in at $186.50, which is 9% lower than today.

The bottom line is that NVDA stock looks cheap here, and one way to play it is to sell short puts at lower prices over the next month.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)