/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

The good times keep rolling in for CoreWeave (CRWV). This time, reputed broker BNP Paribas has initiated coverage on the stock with an “Outperform” rating and a $192 price target. The price implies a sizeable upside potential of about 71% from current levels. Notably, the $61 billion market cap company's stock is already up 56% on a YTD basis.

Analyst Stefan Slowinski of the firm said, “We view CoreWeave as one of the most strategically important companies within the AI infrastructure ecosystem. As the largest ‘neo cloud’ platform, the company has established itself as a preferred infrastructure partner for many of the industry’s leading AI companies while building what we believe is a differentiated software and cloud stack optimized specifically for AI workloads. The company's combination of scale, contractual revenue visibility, differentiated software capabilities, and growing efforts to move up the AI value chain through managed inference services positions the company well longer-term.”

So, should investors heed BNP Paribas's advice and add CRWV to their portfolios? Or, are there any potential pitfalls that one must be wary of before investing? Let's find out.

BNP Paribas Is Essentially Correct

BNP Paribas' assertions about CoreWeave are not misplaced, though another analyst has gone neutral and CoreWeave has a checkered customer base.

However, what's next for the company? What is the leader of neoclouds looking to maintain its leadership?

Well, for 2026, management is guiding for $12 billion to $13 billion in 2026, implying roughly 140% growth again. The infrastructure ambition behind that revenue target is staggering. CoreWeave ended 2025 with 850 megawatts of active power across 43 data centers, has contracted more than 3.1 gigawatts of total capacity, and is planning to roughly double active power to 1.7 gigawatts by the end of 2026. CEO Michael Intrator has signaled that the company is targeting an additional 5 gigawatts of data center capacity by 2030, which would make CoreWeave's footprint a genuine rival to some hyperscaler operations.

The more strategically interesting part of the roadmap, though, is the software pivot. CoreWeave acquired Weights & Biases in May 2025 for roughly $1.7 billion, and the integration is already producing tangible products. In June 2025, at the Weights & Biases Fully Connected Conference, CoreWeave launched three new integrated software products, including Mission Control Integration, W&B Inference, and W&B Weave Online Evaluations, giving AI engineers a unified environment to train models, run inference at scale, and monitor production applications. That matters because GPU rental alone is a commoditizing business. Adding a developer platform on top of the infrastructure is CoreWeave's answer to the margin compression problem.

Then there is the federal opportunity, which is entirely new territory. CoreWeave announced in October 2025 that it is pursuing FedRAMP and other authorizations to bring its AI cloud services to US government agencies and the defense industrial base, a market where demand for secure, high-performance AI infrastructure is accelerating rapidly. For a company that built its reputation in the commercial AI training market, this is a meaningful expansion of the addressable opportunity. The risk, of course, is that CoreWeave is spending $31 billion to $35 billion in capex in 2026 alone while still running net losses, and total liabilities stood at $46 billion at year-end 2025 with interest costs exceeding $300 million per quarter, leaving little room for error.

Yet to Turn Profits

Despite all the optimism around the company, however, the current financials leave a lot to be desired.

The first quarter of 2026 delivered a mixed set of results for the company, with strong top-line performance exceeding forecasts while bottom-line figures fell short of analyst projections. The firm reported revenue of $2.08 billion, marking a substantial 111.6% rise from the year earlier period. Although this revenue momentum was encouraging, the company posted a per-share loss of $1.40, missing the expected loss of $1.20. This figure represented a modest improvement over the $1.49 loss from the same quarter last year, yet operating loss margins expanded to 7% from 3%, indicating that expenses associated with business expansion are growing at a faster pace than sales.

A bright spot in the financial report comes from the sharp rise in liquidity. Net cash provided by operating activities surged to approximately $3 billion, a significant increase from only $61 million in the prior year period. This improvement was supported by a roughly $1 billion decrease in accounts receivable, pointing to stronger collection efforts from customers. Still, the balance sheet raises some concerns. The company closed the quarter with $2.2 billion in cash, a level that looks limited when measured against short-term debt of $8.1 billion. Market participants will monitor whether the firm can sustain its rapid revenue growth and translate it into greater financial stability amid its sizable debt obligations.

Valuation indicators for the stock offer a mixed perspective. The forward P/S ratio of 5.38x stands slightly above the sector median of 3.76x, reflecting a modest premium compared with industry peers. In contrast, the forward P/CF ratio of 7.58x is well below the sector median of 21.17x, which may suggest greater cash generation efficiency than the current market price fully recognizes. This combination underscores the ongoing discussion around the company's ability to manage heavy infrastructure investments while proving sustainable profitability in the competitive cloud computing space.

Analyst Opinions

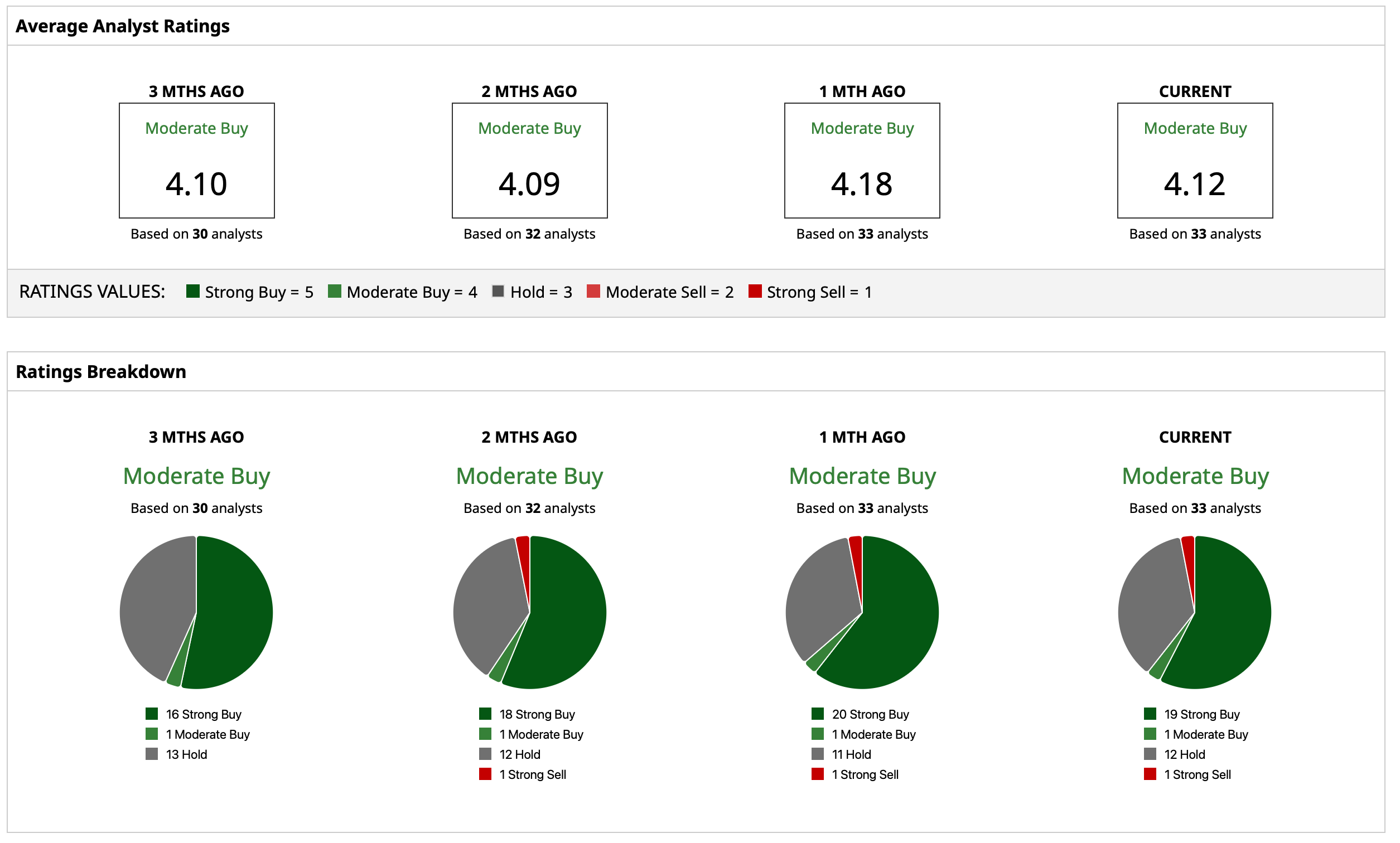

Considering this, analysts have attributed an overall rating of “Moderate Buy” for CRWV stock. The mean target price of $135.35 indicates an upside potential of 20% from current levels. Out of 33 analysts covering the stock, 19 have a “Strong Buy” rating, one has a “Moderate Buy," 12 have a “Hold," and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)